Palantir’s (NYSE:PLTR) stock-based compensation (“SBC”) has always been a controversial topic among shareholders. On the one hand, SBC helps PLTR achieve positive cash flows. On the other hand, it has contributed to the company’s 18-year no-profit streak.

We know that Palantir’s GAAP earnings have always been negative, but the company usually reports positive adjusted earnings. The question is whether GAAP earnings or adjusted earnings better reflect the company’s operating performance. In this article I argue that it’s the former, and that Palantir is best viewed as an unprofitable company. I rate its stock a hold rather than a sell, though, because it does have enough revenue growth to eventually overcome the effects of SBC.

How Palantir’s SBC Facilitates Positive Cash Flows

SBC is one of the tools Palantir uses to achieve positive cash flows. Many Palantir employees believe in the company, and are willing to accept stock in lieu of extra salary. As a result, Palantir typically delivers positive CFO and negative earnings side by side. The picture is a little more complicated than just saying that “SBC overwhelms Palantir’s cash flows.” In addition to its usually negative GAAP earnings, Palantir also reports adjusted earnings–those have been positive in recent quarters. So, we really need to take a deep look at SBC and whether earnings are positive after accounting for it.

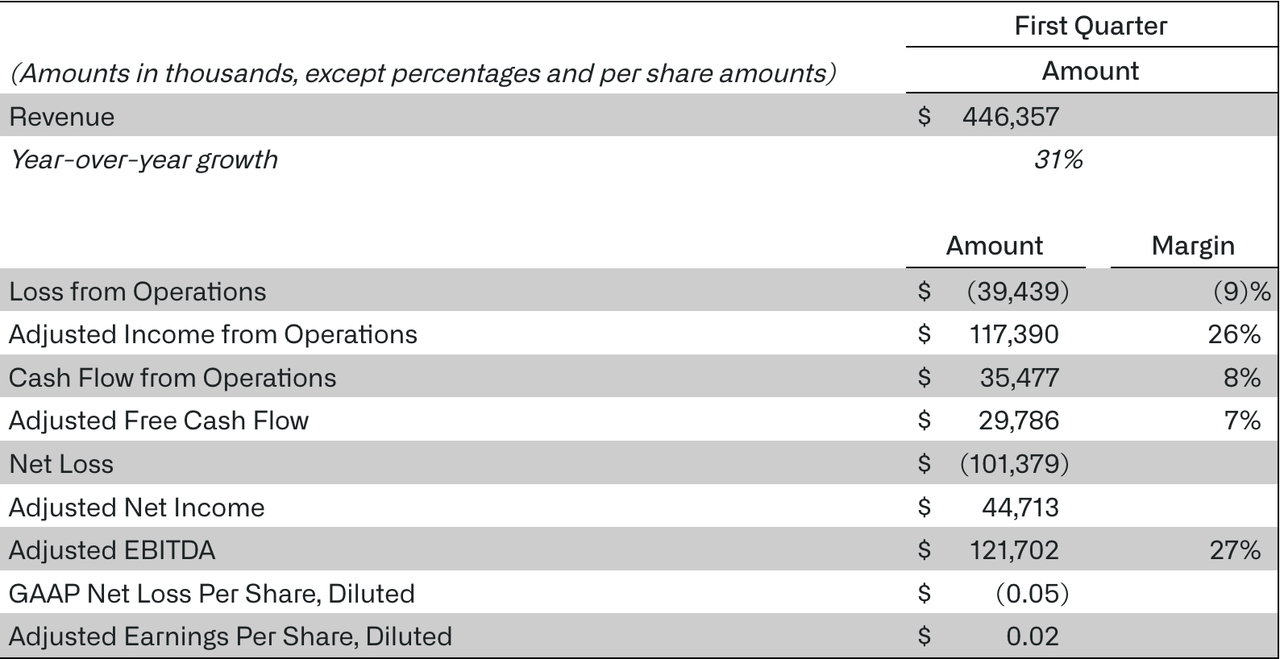

Palantir’s reported net income for Q1 was $-101 million. Add back $149 million in SBC, and you end up with $48 million in profit. So, SBC is definitely keeping GAAP profits at bay. However, we also know that Palantir’s Q1 news release listed $0.02 in positive adjusted earnings, so we have to investigate further. Maybe Palantir’s standards are better than those of the FASB.

Where Palantir’s SBC is Coming From

The first thing you need to know about SBC is that there isn’t just “one kind.” SBC can take a number of different forms:

Immediate stock grants.

Stock options triggered on a certain vesting date.

Stock options triggered when an employee hits certain performance targets (common with upper management).

In Palantir’s case, two types of stock awards are mentioned for the period for the first quarter:

Exercise of stock options - 6.6 million shares.

Issuance of stock after vesting of RSUs - 11.7 million shares

These are listed separately from SBC on PLTR’s statement of changes of equity. It appears that the counts above are for past options exercised in the quarter, while the SBC number is for new shares granted. Nevertheless, these line items do tell us where Palantir’s SBC is coming from: mainly, its stock options, not immediate grants.

We know from an SEC filing that Palantir registered 101.3 million shares at the start of the first quarter. At today’s prices they’d be worth about $850 million. Palantir says that they will be granted over the next three years. It appears, then, that the $149 million in SBC recorded in the second quarter is just the beginning of $283 million worth of SBC per year over the next few years.

Financial Forecast

If Palantir is going to be doing $283 million in annual SBC over the next three years, then GAAP profits will be hard to come by. Alex Karp said on PLTR’s recent earnings call that only $9 million worth of new shares would be issued this year. It may be that only $9 million worth of new shares will be issued, but the projected SBC implies that $850 million or so worth of shares will be given out. Shares don’t have to be issued immediately in order for SBC expenses to be recorded, as SBC cost is recorded when granted, not when shares vest. So, we’ll take $283 million, not $9 million, as our estimate of average SBC over the next three years.

If you grow Palantir’s cash from operations (“CFO”) at 31% per year (PLTR’s growth target), you get the following FCF numbers:

This year: $252 million.

Year 1: $330 million.

Year 2: $432 million.

Year 3: $566 million.

That looks like impressive growth. But remember that the real return to shareholders has to account for SBC. With $283 million worth of SBC per year, these numbers all go lower. If $283 million in SBC is taken added back to CFO every single year, then the above CFO forecast is reduced as follows:

This year: $-31 million.

Year 1: $47 million.

Year 2: $149 million.

Year 3: $283 million.

The above is simply how much CFO is reduced by subtracting the forecasted amount of SBC. To get all the way to net income, you need to subtract other non-cash costs as well. According to Seeking Alpha Quant, Palantir had $-498 million in negative net income in the trailing 12-month period. Included in that was $16 million in depreciation, a $10.3 million increase in accounts payable, and $78 million in “other operating activities.” If you throw all of those costs on top of $283 million in annual SBC, then you don’t get to positive net income until year 2 in my forecast above.

That’s potentially a problem. In a recent article, I wrote that PLTR’s fair value was between $5.91 and $13.58. My reasoning was based on a discounted cash flow analysis: the PV of five years’ cash flows for PLTR works out to $5.91 or $13.58 depending on the sustainable growth rate. However, the model I built in that article was quite literally a discounted cash flow model: it was based on FCF. Had I used net income or even just FCF adjusted for SBC, the present value would have been far lower.

Where do Palantir’s Positive Adjusted Earnings Come From?

As we’ve seen, Palantir’s SBC has been preventing it from achieving GAAP profits. That will likely be the case until at least 2024. However, we know that PLTR is reporting positive adjusted earnings–$0.02 worth in the most recent quarter. Before we can really say that Palantir is unprofitable, we should look at what those adjusted earnings consist of. Sometimes companies will take mark-to-market stock losses out of GAAP earnings, and that’s a valid adjustment, because short term stock fluctuations have nothing to do with operating performance. If Palantir has some of these “costs” in the picture, then maybe it’s not as unprofitable as it looks.

Unfortunately, it appears that PLTR’s “positive adjusted earnings” is mostly just a matter of adding SBC back to net income. In the most recent quarter, the company reported $-101 million in GAAP earnings, $149 million in SBC, and $44 million in adjusted earnings. The adjusted figure is almost exactly what you’d get by adding SBC back to net income. Additionally, Palantir said in its recent quarterly report that it adds SBC back to adjusted earnings.

Palantir

This is a problem because SBC is not one of the non-cash charges you can just ignore. Many value investors think that short term stock fluctuations are meaningless, nobody thinks that an ever-growing share count is. The higher the number of shares, the smaller each shareholder’s percentage ownership. That’s a real cost. So, Palantir isn’t “adjusting” for questionable accounting rules. The FASB is right in forcing companies to subtract SBC from net income.

There is perhaps one silver lining here:

Palantir’s shares for the next three years’ worth of SBC have already been issued. As I mentioned earlier, the company registered about 100 million shares in January, mainly for future stock awards. These shares aren’t in the public float yet, but they’re already part of shares outstanding. So, the EPS-reducing effect of the newly issued shares has already occurred. This means that investors won’t have to cope with seeing EPS mysteriously decline as free cash flow rises. Unfortunately, if Palantir’s employees sell their shares when they vest, then that will create extra selling pressure that could send the stock lower. Perhaps, then, the really meaningful dilution (dilution of the public float) is yet to take place.

Risks and Challenges

So far, I have developed a neutral thesis on Palantir. This is a company with pretty obvious strengths and obvious weaknesses, and it’s hard to have a strong opinion on it when each virtue is countered by an equivalent vice.

Indeed, both bulls and bears have many risks and challenges to be mindful of.

Bulls need to be wary of any future deceleration. Palantir’s biggest strength right now is that it still has high revenue growth even amid 2022’s tech slowdown. In their most recent quarters, Meta (FB) and Apple (AAPL) both experienced single-digit revenue growth, PLTR was still all the way up at 31%, just like in the glory days of early 2021. Palantir is one of the few tech stocks that’s still delivering the growth investors want from tech stocks, which is why deceleration is so risky. If Palantir stops growing then SBC and other cost factors become bigger and bigger issues, because they are no longer offset by high revenue growth. So, deceleration is a huge risk to Palantir bulls.

Bears (i.e., shorts) on the other hand need to be wary of Palantir’s resilience. PLTR has a lot of recurring revenue locked in from government contracts that last 3.5 years on average. This is a company with more revenue stability than average, so there is always the potential for upside surprises–particularly if commercial growth accelerates. Palantir gets a stable “base” of revenue from its long-term government contracts, along with growth potential from its rising commercial client base. So, the company could continue delivering on the top line for a long time.

The Bottom Line

Taking everything into account, we can say this about Palantir’s stock-based compensation:

It is a real, material cost. SBC is not something that investors can ignore. It dilutes equity and makes existing shareholders’ ownership stake smaller. So, Palantir’s GAAP earnings are more correct than its adjusted earnings. SBC is not a cost you can write off, so PLTR is, at the end of the day, unprofitable.

Does that mean that the stock is a bad buy?

Not necessarily. Its revenue growth is still strong, and that growth could someday overpower the increases in the share count. That’s one reason for optimism. However, the conclusion is inescapable: Palantir is losing money. And it probably will continue doing so until SBC is brought under control.