SVB Financial Group faced a perfect storm, but there are plenty of other banks that would face big losses if they were forced to dump securities to raise cash

Silicon Valley Bank has failed following a run on deposits, after its parent company's share price crashed a record 60% on Thursday.

Trading of SVB Financial Group's $(SIVB)$ stock was halted early Friday, after the shares plunged again in premarket trading. Treasury Secretary Janet Yellen said SVB was one of a few banks she was "monitoring very carefully." Reaction poured in from several analysts who discussed the bank's liquidity risk.

California regulators closed Silicon Valley Bank and handed the wreckage over to the Federal Deposit Insurance Administration later on Friday.

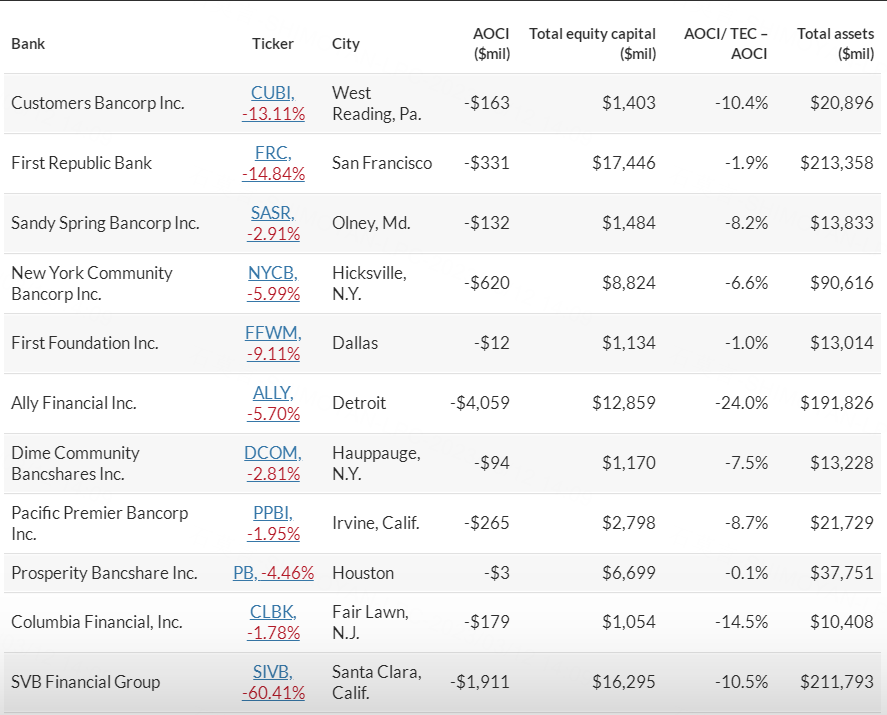

Below is the same list of 10 banks we highlighted on Thursday that showed similar red flags to those shown by SVB Financial through the fourth quarter. This time, we will show how much they reported in unrealized losses on securities -- an item that played an important role in SVB's crisis.

Below that is a screen of U.S. banks with at least $10 billion in total assets, showing those that appeared to have the greatest exposure to unrealized securities losses, as a percentage of total capital, as of Dec. 31.

First, a quick look at SVB

Some media reports have referred to SVB of Santa Clara, Calif., as a small bank, but it had $212 billion in total assets as of Dec. 31, making it the 17th largest bank in the Russell 3000 Index as of Dec. 31. That makes it the largest U.S. bank failure since Washington Mutual in 2008.

One unique aspect of SVB was its decades-long focus on the venture capital industry. The bank's loan growth had been slowing as interest rates rose. Meanwhile, when announcing its $21 billion dollars in securities sales on Thursday, SVB said it had taken the action not only to lower its interest-rate risk, but because "client cash burn has remained elevated and increased further in February, resulting in lower deposits than forecasted."

SVB estimated it would book a $1.8 billion loss on the securities sale and said it would raise $2.25 billion in capital through two offerings of new shares and a convertible bond offering. That offering wasn't completed.

So this appears to be an example of what can go wrong with a bank focused on a particular industry. The combination of a balance sheet heavy with securities and relatively light on loans, in a rising-rate environment in which bond prices have declined and in which depositors specific to that industry are themselves suffering from a decline in cash, led to a liquidity problem.

Unrealized losses on securities

Banks leverage their capital by gathering deposits or borrowing money either to lend the money out or purchase securities. They earn the spread between their average yield on loans and investments and their average cost for funds.

The securities investments are held in two buckets:

In its regulatory Consolidated Financial Statements for Holding Companies--FR Y-9C, filed with the Federal Reserve, SVB Financial, reported a negative $1.911 billion in accumulated other comprehensive income as of Dec. 31. That is line 26.b on Schedule HC of the report, for those keeping score at home. You can look up regulatory reports for any U.S. bank holding company, savings and loan holding company or subsidiary institution at the Federal Financial Institution Examination Council's National Information Center. Be sure to get the name of the company or institution right -- or you may be looking at the wrong entity.

Here's how accumulated other comprehensive income (AOCI) is defined in the report: "Includes, but is not limited to, net unrealized holding gains (losses) on available-for-sale securities, accumulated net gains (losses) on cash flow hedges, cumulative foreign currency translation adjustments, and accumulated defined benefit pension and other postretirement plan adjustments."

In other words, it was mostly unrealized losses on SVB's available-for-sale securities. The bank booked an estimated $1.8 billion loss when selling "substantially all" of these securities on March 8.

The list of 10 banks with unfavorable interest margin trends

On the regulatory call reports, AOCI is added to regulatory capital. Since SVB's AOCI was negative (because of its unrealized losses on AFS securities) as of Dec. 31, it lowered the company's total equity capital. So a fair way to gauge the negative AOCI to the bank's total equity capital would be to divide the negative AOCI by total equity capital less AOCI -- effectively adding the unrealized losses back to total equity capital for the calculation.

Getting back to our list of 10 banks that raised similar red margin flags to those of SVB, here's the same group, in the same order, showing negative AOCI as a percentage of total equity capital as of Dec. 31. We have added SVB to the bottom of the list. The data was provided by FactSet:

Ally Financial Inc. (ALLY) -- the third largest bank on the list by Dec. 31 total assets -- stands out as having the largest percentage of negative accumulated comprehensive income relative to total equity capital as of Dec. 31.

To be sure, these numbers don't mean that a bank is in trouble, or that it will be forced to sell securities for big losses. But SVB had both a troubling pattern for its interest margins and what appeared to be a relatively high percentage of securities losses relative to capital as of Dec. 31.

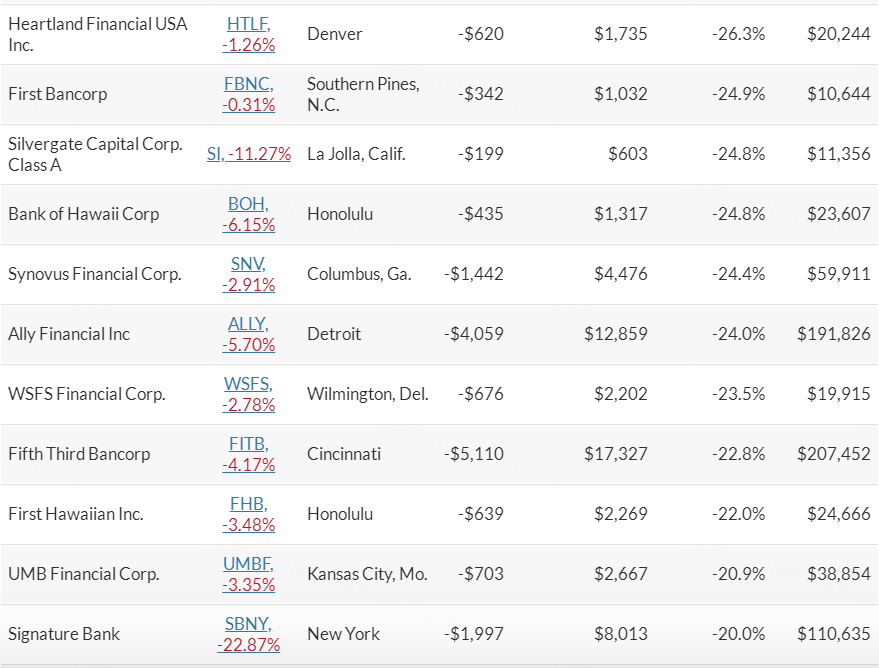

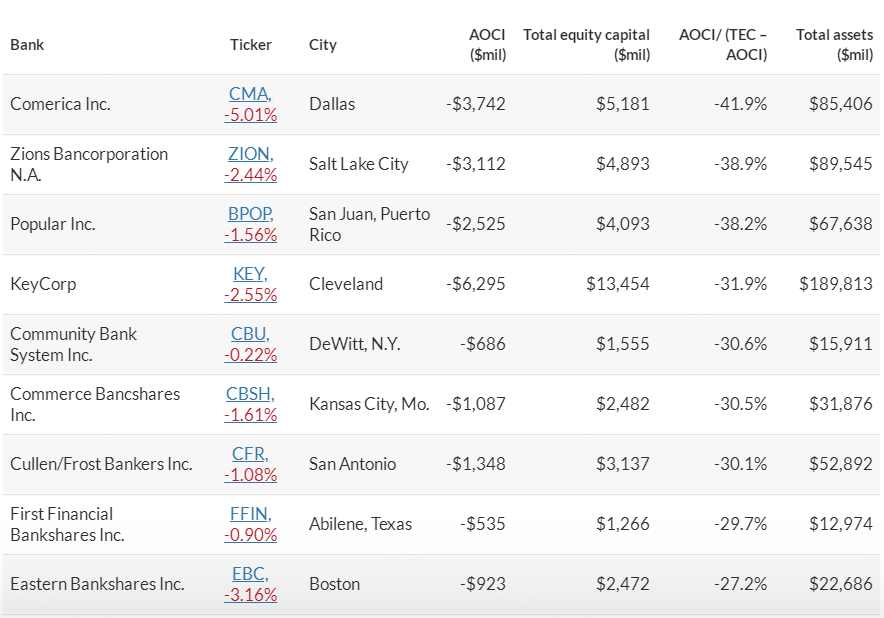

Banks with the highest percentage of negative AOCI to capital

There are 108 banks in the Russell 3000 Index that had total assets of at least $10.0 billion as of Dec. 31. FactSet provided AOCI and total equity capital data for 105 of them. Here are the 20 which had the highest ratios of negative AOCI to total equity capital less AOCI (as explained above) as of Dec. 31:

But it is interesting to note that Silvergate Capital Corp., which focused on serving clients in the virtual currency industry, made the list. It is shuttering its bank subsidiary voluntarily.

Another bank on the list facing concern among depositors is Signature Bank of New York, which has a diverse business model, but has also faced a backlash related to the services it provides to the virtual currency industry. The bank’s shares fell 12% on Thursday and were down another 24% in afternoon trading on Friday.

Signature Bank said in a statement that it was in a “strong, well-diversified financial position.”