Meituan Q1 Earnings: Earning Huge Beat, with Recovery and Competition

$Meituan(03690)$ released its Q1 2023 earning after May25.

Once again, double beat on revenue and profit, with profits significantly surpassing predictions as part of the expected post-pandemic recovery. As Meituan's performance often exceeds expectations, we are paying attention to two core areas: the recovery of offline-to-online and travel businesses and the reduction in losses for new businesses. The significant increase in profits this quarter is largely due to improvements in these two areas - core business has improved through a revival of high-profit margin operations while new business has improved by reducing costs and increasing efficiency. These factors have positively impacted long-term valuation levels. In terms of secondary markets, Tencent's dividend impact is nearing its end; therefore, Meituan is highly likely to become a leading stock driving economic recovery.

Earnings Review

Revenue

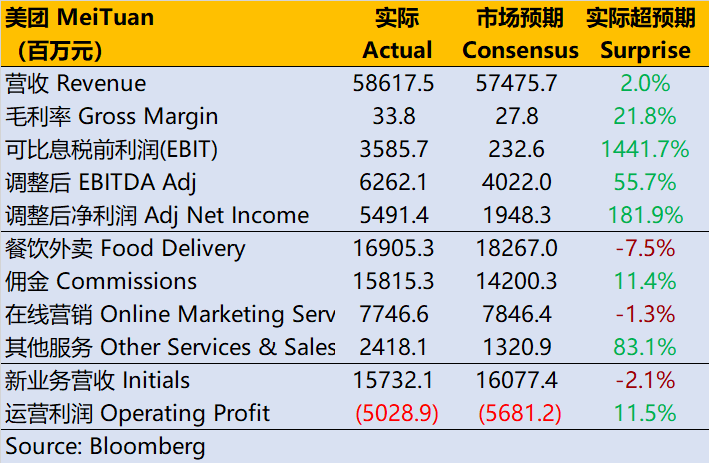

Total revenue was CNY 58.617 billion yuan, an increase of 26.7% YoY - one of few internet companies maintaining double-digit growth rates - exceeding market expectations at CNY 57.48 billion yuan.

By Segment: Overall local commerce revenue was CNY 42.89 billion yuan (+25.5% YoY), higher than expected at CNY41 .63 billion yuan; New business revenues were CNY15 .73 billion yuan (+30.l %YoY), lower than expected atC NY16 .08billionyuan.

By Nature: Delivery service income was CNY16 .91billionyuan(+18 .7%YoY); Commission income wasC NY1624billionyua n(+32.l %Yo Y); Online marketing services wereC NY77.Sb illion yu an(+10.g% Yo Y); Other services and sales wereC NY1768bill ionyu an(+39.% Yo Y).

Operating Data: Active merchants increased by 30% YoY; Instant delivery transactions were 4.267 billion, an increase of 14.9% YoY.

Costs

Total COGS were CNY38.8 billion yuan, better than market expectations at CNY41 .47 billion yuan.

Sales expenses wereC NY10A3b illion yu an, higher than expected at CNY89.Sbillionyuan with a sales expense ratio of17.g%, lower than last quarter's17 .9%, and significantly down from last year's19 .7%.

Administrative expenses wereC NY1g.billionyu an, accounting for only3.4% compared to5.O% in the same period last year.

Research and development expenditures reached CNY5O.A billion yuan with a research and development cost rate of8.g%, lower than the same period last year's10.s%.

Profit

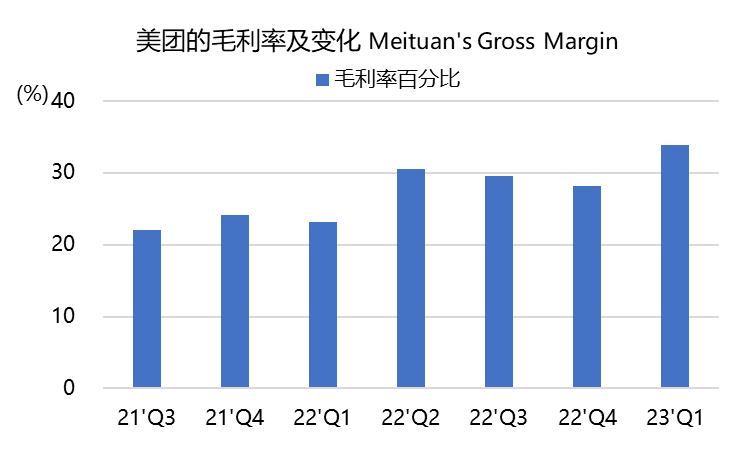

Gross profit margin was 33.81%, higher than market expectations at27 .77%; this leaves room for overall profit margins to grow.

Adjusted pre-tax profits reached CNY35.5billion yuan - better than the previous year (-CNY50 million) and exceeding market expectations (+CNY230 million). Adjusted EBITDA was62.G billion yuan - surpassing market expectations (+40.ZBillion Yuan); adjusted net profit was CNY33.S Billion Yuan while the market had predicted losses.

Investment Highlight

Q1 is the first quarter after recovery began; however, January still had some degree of impact reflected in active user numbers (which have not been disclosed this quarter but are expected to decline), as well as transaction orders related to medicine rising. Overall profitability exceeded predictions due largely to high-profit-margin businesses such as offline-to-online commerce recovering their share percentage-wise post-recovery.

As Meituan revised its business classification again in Q2 2022, both takeaway and offline-to-online travel businesses were included in the local core commerce category, making individual business segments somewhat of a "mixed bag."

Core businesses continue to perform exceptionally well with order volume increasing by 35% YoY. Commission growth reached 32%, far exceeding market expectations - reflecting an increase in transaction volume and price due to recovery while delivery costs can contribute higher profit margins long-term thanks to improved efficiency.

Meituan also charges both users and merchants for delivery services; Q4 saw a significant reduction in logistics subsidies compared to the pandemic environment of Q2. Similar to JD.com, Meituan has further demonstrated economies of scale through logistics services that exceeded market expectations.

The in-store and travel businesses have grown rapidly, but although they have escaped the impact of the epidemic, the recovery of merchant marketing activities may not catch up with overall growth. The growth rate of online marketing services is only 10%, which is critical compared to the previous quarter's decline, but it cannot match the overall 26% and local core commercial 25%. This reflects two factors: 1. Competition from short video platforms such as Douyin for in-store business; 2. Macroeconomic consumption recovery falls short of expectations, and merchants are more cautious about their investments.

However, overall, the recovery of travel business will greatly bring back lost profit margins in the long term.

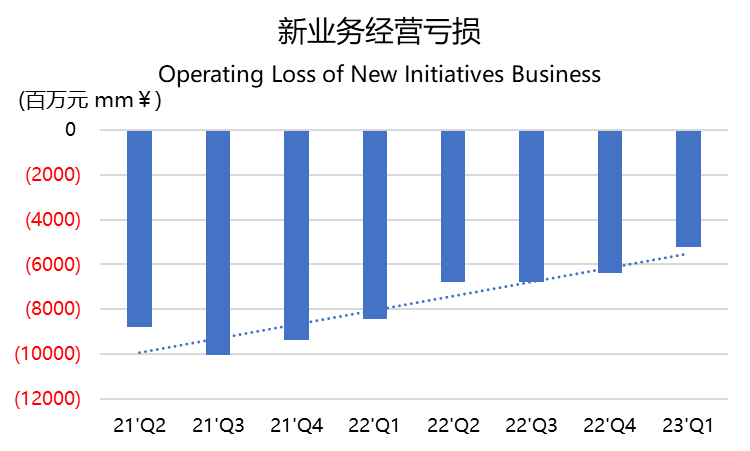

In terms of new businesses, a year-on-year revenue growth rate of 30% may be somewhat lower than expected, but reducing losses in this area is more important. The operating loss rate for Q1 has dropped to 32%. Through offline transaction markets' rebounding trend, grocery shopping and preferred businesses will further reflect economies of scale and are expected to turn losses into profits earlier.

From a profit perspective, gross profit margin is expected to continue at its current level after travel business recovers.

Other expenses including management fees and R&D costs remain relatively stable. However, marketing expenses were not well controlled with spending reaching CNY10.4 billion higher than market expectations' CNY9 billion during this recovery phase. This means that companies spent significant costs on seizing offline businesses while responding to competition due to economic recovery expectations rather than increasing subsidies since food delivery services are already matured.

Overall operating profit margin reached 6.1%, amounting to CNY3.58 billion where wealth management income was an important reason for pushing other income up this quarter highlighting Meituan's ample cash flow situation.Adjusted net profit was CNY5.49 billion including share-based compensation (nearly CNY2 billion non-cash expenses).

Valuation and Expectations

It must be said that the current priority of reducing costs and increasing efficiency will bring investors great confidence in profit margin improvement.

We have previously estimated that if there are no significant changes in macroeconomic environment, Meituan still applies growth company valuation logic among existing internet technology companies. That is, after the expected future few years' profit margins tend to stabilize at a certain level, they can be discounted back to current valuations.

Assuming core business revenue reaches CNY290 billion by 2025 and terminal profit margin stabilizes at around 20%, then profits would approach CNY58 billion. Calculated with a P/E ratio of 25 times, the valuation would reach HKD1.45 trillion. Even with a higher WACC (Bloomberg) discount rate of 22%, each share could reach HKD170 by 2023.

Currently, Tencent's dividend impact has almost come to an end, and changes in buying and selling power require opportunities such as financial reports to ignite them. Of course, overall attractiveness of Chinese assets is currently the biggest influencing factor for investors on these heavyweight stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

How has the pandemic affected Meituan's offline-to-online and travel businesses?

Consumption recovers, and Meituan's core local business is stable and healthy.

Can Meituan sustain their current level of profits in the long term?

What happened to the Hong kong market? It sucks.

chinese stocks are not doing so well at the moment

Sharing