A soaring LULU is still cheaper than Nike?

$lululemon athletica(LULU)$ announced its performance for Q1 of the fiscal year 2023. Unlike the overall slump in the clothing retail sector and the recent sell-offs of luxury brands, LULU's strong Q1 performance and Q2 guidance led to a 13% surge in its stock price after hours.

Performance Overview

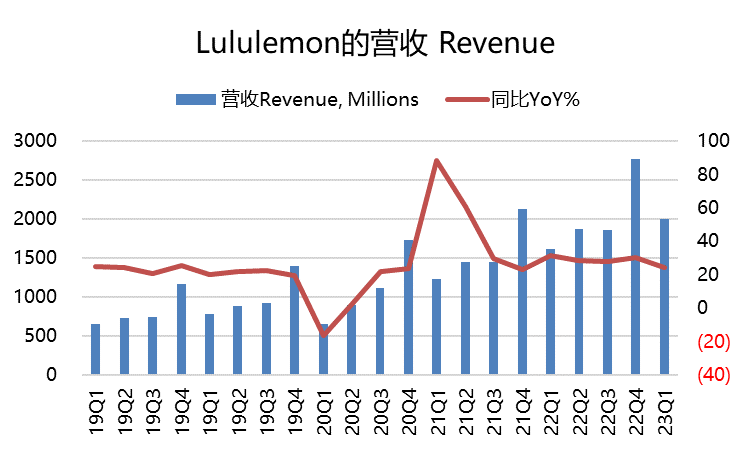

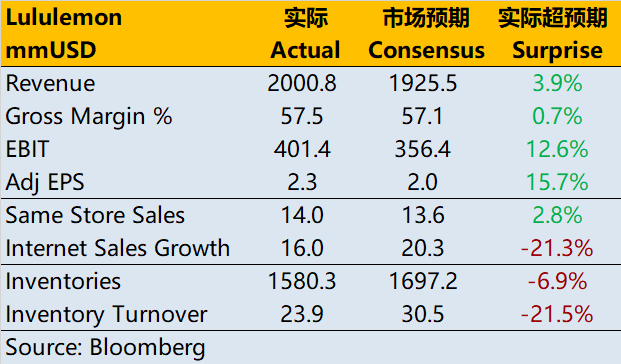

- Total revenue reached $2 billion, a year-on-year increase of 24%, or 27% growth on a fixed exchange rate basis.

- International market growth was 60%, while North America grew by 17%.

- Comparable store sales increased by 14% year-on-year or 17% on a fixed currency basis.

- Direct-to-consumer revenue grew by 16% or 18% on a fixed exchange rate basis, accounting for 42% of total sales.

- Gross margin reached $1.2 billion, with a gross profit margin of 57.5%, a 360 basis point increase from a year ago.

- Operating profit increased by 54% to reach $401.4 million, and the adjusted operating profit margin increased by 400 basis points this quarter, reaching 20.1%.

- Diluted earnings per share were $2.28, compared to $1.48 in the first quarter of 2022.

- Inventory levels stood at $1.58 billion, a 24% year-on-year increase, which was lower than the market expectation of $1.70 billion.

- LULU opened 7 new self-operated stores, bringing the total store count to 662.

Company executives stated that the strong Q1 performance and positive response across global markets, particularly the significant acceleration of sales in China, contributed to the momentum. Additionally, the reduction in air freight costs played a positive role. They expressed satisfaction with the momentum for the upcoming second quarter and the entire fiscal year.

Guidance-wise, LULU expects revenue for 2023 to be between $9.44 billion and $9.51 billion, surpassing the consensus of $9.36 billion. The projected earnings per share for the full year range from $11.74 to $11.94, exceeding the market expectation of $11.60.

Investment Highlights

After exceeding expectations last quarter, LULU's stock price has already climbed a step. As we previously mentioned, the company has taken a middle-to-high-end sports route, mainly relying on the sustained impact of its brand influence.

While the growth of comparable store sales remains higher than market expectations, the growth rate of the DTC business is even faster. One notable difference in Q1 is that the company started promoting discounts and offered certain product incentives. As a result, the inventory consumption in this quarter performed better than anticipated, and the growth rate has decreased to the level seen at the beginning of 2022. However, the current inventory remains at a relatively high level, suggesting that promotional activities may continue.

The biggest setback is the acquisition of Mirror. In June 2020, the company acquired the home fitness business, Mirror, for $500 million, with the intention of expanding its customer base for home workouts. However, as the pandemic control measures eased, this segment has had a negative impact on LULU's performance. Currently, LULU is seeking to sell Mirror.

In addition to yoga apparel and women's products, the company's two future growth focuses are the men's market and footwear. Furthermore, the incremental growth in the Chinese market is crucial for the performance of the coming quarters.

Valuation

Due to the company's increased revenue guidance for the 2023 fiscal year, supported by operational leverage, the company's profits are expected to further increase.

Therefore, although the company's P/E ratio is currently high at 31 times, it is anticipated that with the realization of higher growth rates, the company's valuation level will decrease. The forward P/E ratio for the 2023 performance expectation is expected to decrease to 28 times, which is lower than that of top companies like Nike.

On the other hand, the company is also engaging in a certain degree of share buyback. In Q1, it repurchased 300,000 ordinary shares at an average price of $336.37 per share.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Amazing earnings call. Everything was extremely positive. They said sales increased through the quarter by month. No slowdown whatsoever. This stock is going to explode to new highs.

Between lulu and aritzia, I think aritzia is a better buy, both are debt free, have the same growth and profitability but aritzia is at a forward pe of 15 vs lulu which is at 30. Lulu makes like 8m a store in revenue but aritzia makes 20m per store

Lulu will have raise prices to cover stolen merchandise