Should we on board Unity with Apple's latest partnership?

With the traditional "Just one more thing" moment of the Jobs era, $Apple(AAPL)$ CEO Tim Cook introduced Apple Vision Pro, a highly anticipated VR eyewear product, at Monday's WWDC.

Although the ultimate size of the market for this product is still unknown, the current price of around $3,500 may discourage many consumers from purchasing it.

However, the technology itself is fascinating. Vision Pro will allow users to see a larger screen through headphones and control it using their eyes, hands, and voice, unlike $Meta Platforms, Inc.(META)$’s Oculus, which relies on external hand controllers.

Currently, the most mature commercial application of virtual reality is gaming. Apple mentioned its collaboration with $Unity Software Inc.(U)$ during the event, causing Unity's stock price to soar on Monday, even triggering a trading halt, and ultimately closing with a 17% increase.

What kind of company is Unity?

Unity is one of the most widely used game engines among global mobile game developers. It was established early on, in 2004, with a focus on real-time 3D interactive content creation and operation, providing the foundation for later building various AR and VR interactive experiences. In addition to Apple's iOS, developers can efficiently and conveniently develop cross-platform applications on Unity, which can be created and deployed on more than 20 platforms, including Windows, Mac, iOS, Android, PlayStation $Sony(SONY)$ , Xbox $Microsoft(MSFT)$ , $Nintendo Co., Ltd.(NTDOY)$ Switch, as well as leading AR and VR platforms.

For example, $TENCENT(00700)$' "Honor of Kings" and $Activision Blizzard(ATVI)$ 's "Hearthstone" client were both developed using Unity3D. These companies have maintained rapid growth in the virtual reality and augmented reality industries, relying on the Unity3D game engine, which has brought opportunities to Unity. VR applications typically have high requirements for the transmission speed of high-definition 3D scene data. With the arrival of the 5G era and the increase in bandwidth throughput, fundamental changes in products become possible.

Unity's business consists of three parts: Operate Solutions, Create Solutions, and Others, with the main focus on the first two parts.

Operate Solutions accounts for over half of the company's revenue, with the majority coming from advertising and cloud services. The cloud business primarily utilizes fundamental tools to process in-game data, while the advertising business adopts precise targeting for revenue generation through profit sharing. The amount of revenue from targeted advertising depends largely on the number of clients and the algorithm's ability to improve the GMV conversion rate.

Create Solutions primarily refers to game engine software, enabling creators to easily develop, edit, and iterate interactive 2D and 3D content in real-time.

In addition, Unity provides customers with tiered subscription plans based on their revenue, offering different-priced solutions ($0-1800) to meet the needs of users at various stages and versions tailored to different industries.

Other business activities include strategic partnerships with hardware/game console/device manufacturers. Despite the current challenging environment in the overall entertainment and leisure industry, Unity's recent acquisitions of Weta and ironSource are expected to bring additional value to the company. It is projected that Weta's tools will become profitable starting in 2023, and the integration with ironSource has yielded benefits for Unity, improving the performance of both networks.

How is Unity's financials?

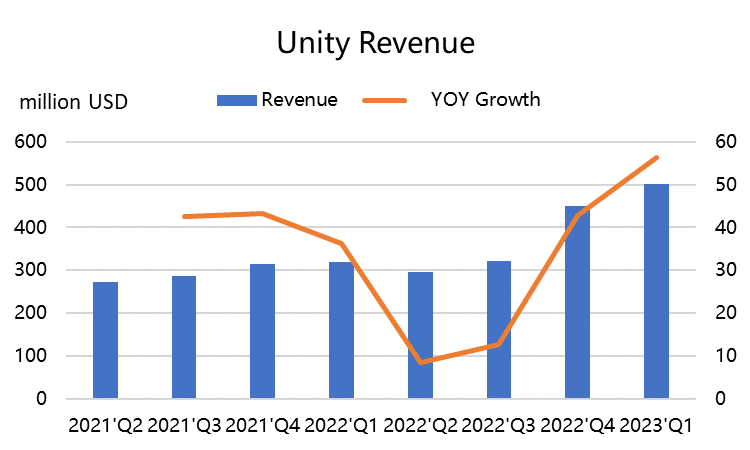

In Q1 2023, Unity's revenue reached $500 million, representing a year-on-year growth of 56%. However, excluding the acquisition portion and calculating based on comparable benchmarks, the revenue actually declined by 2% instead of experiencing growth. Furthermore, it is anticipated that the Q2 revenue will grow by 72-75% compared to the previous year, resulting in a 6-8% growth when considering comparable benchmarks. It is important to note that there were currency monetization issues in the second quarter of 2022, so the adjusted revenue may be on par with the previous year.

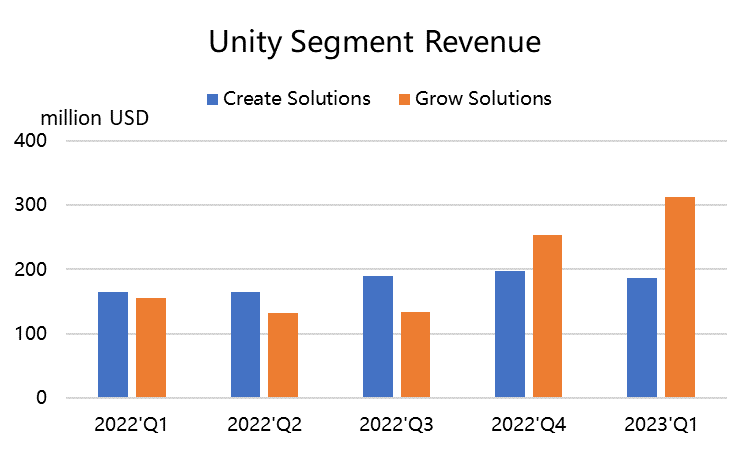

Specifically, the revenue from create solutions saw a 14% year-on-year growth in the first quarter, with a growth rate of 17% when excluding revenue from strategic partnerships. The growth rate has slowed down compared to before, which Unity attributes to the company gradually distancing itself from professional services and increasing reliance on partners for project implementation. Part of the decline in revenue is attributed to the decline in professional services. Unity is reducing the significance of professional services and increasing utilization with partners like Booz Allen and Capgemini. These partnerships assist customers in implementing digital twins, with Booz Allen being more involved in government projects and Capgemini operating in various industries such as energy. Collaborating with these partners helps Unity expand its creative business and continue to benefit from high-profit cloud revenue. However, the company's customer churn rate remains low and has shown improvement over time.

The operational services business still faces resistance in a macroeconomic environment weakened by the overall situation, but growth is expected to accelerate in 2023 with the synergy between Unity and ironSource. For example, ironSource's ad network is shifting towards more advanced Unity ML models, while Unity's ad network adopts ironSource's bidding model.

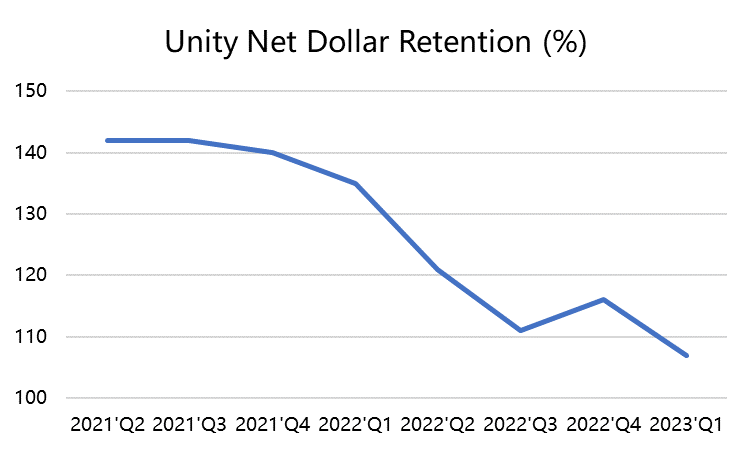

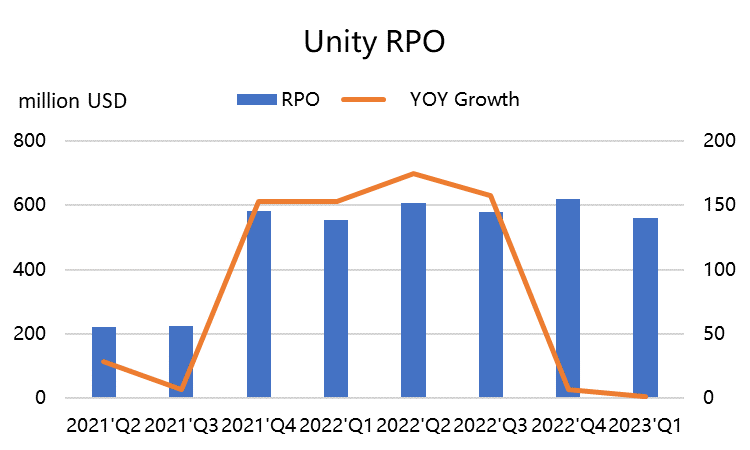

Regarding customers, the number of major clients for Unity has remained stable or declined in recent quarters. Currently, Unity relies on the acquired ironSource to maintain the current situation, which may be more a result of slowed consumer growth rather than customer loss. The remaining performance obligations (RPO) for the company currently stand at $559 million, down from the previous quarter's $620 million. Deferred software revenue has also decreased from around $320 million in the previous quarter to around $300 million.

In terms of profitability, the gross margin has been continuously declining; however, this situation is expected to reverse as the Weta business monetizes more quickly. Additionally, the company is undergoing ongoing workforce reductions, including reducing the number of management levels, partly to absorb the recently acquired companies and achieve cost synergies.

Is Unity worth buying now?

First of all, whether it's VR, AR, or AI, Unity has great opportunities to benefit from them. Generative AI will become a huge boost to the gaming industry, making the construction of 3D experiences simpler and achieving new experiences that are currently impossible.

Unity is developing editor tools and plans to open a generative AI marketplace to profit from the progress of the entire ecosystem. This includes the Unity editor and Unity Runtime.

In addition, Unity has recently increased the prices of some subscription services, but the impact on customer churn is minimal. This demonstrates the company's strong competitive position and indicates that the company has a higher pricing power. In the future, growth is expected to come from usage, as Unity believes there is great potential for increasing assessable revenue over time as developers start using more AI tools and building more advanced worlds.

In terms of valuation, since it has just started positive EBITDA profits, the company is currently more suitable to be compared with peers based on revenue multiples. Of course, some investment banks use post-2024 profit expectations as a benchmark and discount them to calculate the target price.

When comparing the overall revenue multiples with the industry, Unity's revenue multiple (EV/Sales) is 8.7 times, which is higher than the industry average of 6.6 times. However, if the valuation is separated into two parts based on the potential of the developer business with a multiple of 9 and a multiple of 3 for operational services, and using Unity's projected market revenue for 2024, the valuation is $40 per share.

More optimistic investors may value it based on higher revenue expectations.

Therefore, for Unity, the short-term price has already reached a position close to the target valuation, so shorting is definitely not cost-effective. In the future, there is a possibility of greater stock price changes as performance exceeds or falls short of expectations. Considering the current collaboration with Apple, there will be more market funds flowing in, resulting in a certain degree of premium on the stock price.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

It sounds like Unity has a lot of different revenue streams. What are some of the main ways they make money?

Great ariticle, would you like to share it?

Should we board ...?

Great ariticle, would you like to share it?

Great ariticle, would you like to share it?

Great ariticle, would you like to share it?

这篇文章不错,转发给大家看看

这篇文章不错,转发给大家看看

Great ariticle, would you like to share it?

Join 😃😃😃😃

Wow

Sharing