Here's Why The Best Low Volatility Performer Could Perform Better!

Takeaways

The stock price of Meta Platforms (META) has recovered most of its losses since 2021 and is now only 20% away from its previous high.

In the face of challenges such as iOS privacy changes, TikTok's growth, and regulatory hurdles in multiple jurisdictions, Meta has shown resilience through cost reduction and increased operational efficiency, supporting the company's rebound.

Meta maintains industry leadership in VR devices and has released its latest VR headset ahead of Apple.

Meta is considering building an alternative to Twitter, integrating social media features further into its platform.

Meta's AI model, I-JEPA, can analyze and complete missing image world models more accurately than existing models. The inclusion of AI has also increased user engagement.

The company has a strong cash reserve, which provides an advantage in a high-interest rate environment. Over the next few years, Meta aims to support its valuation through operational efficiency improvements, increased monetization, and share buybacks.

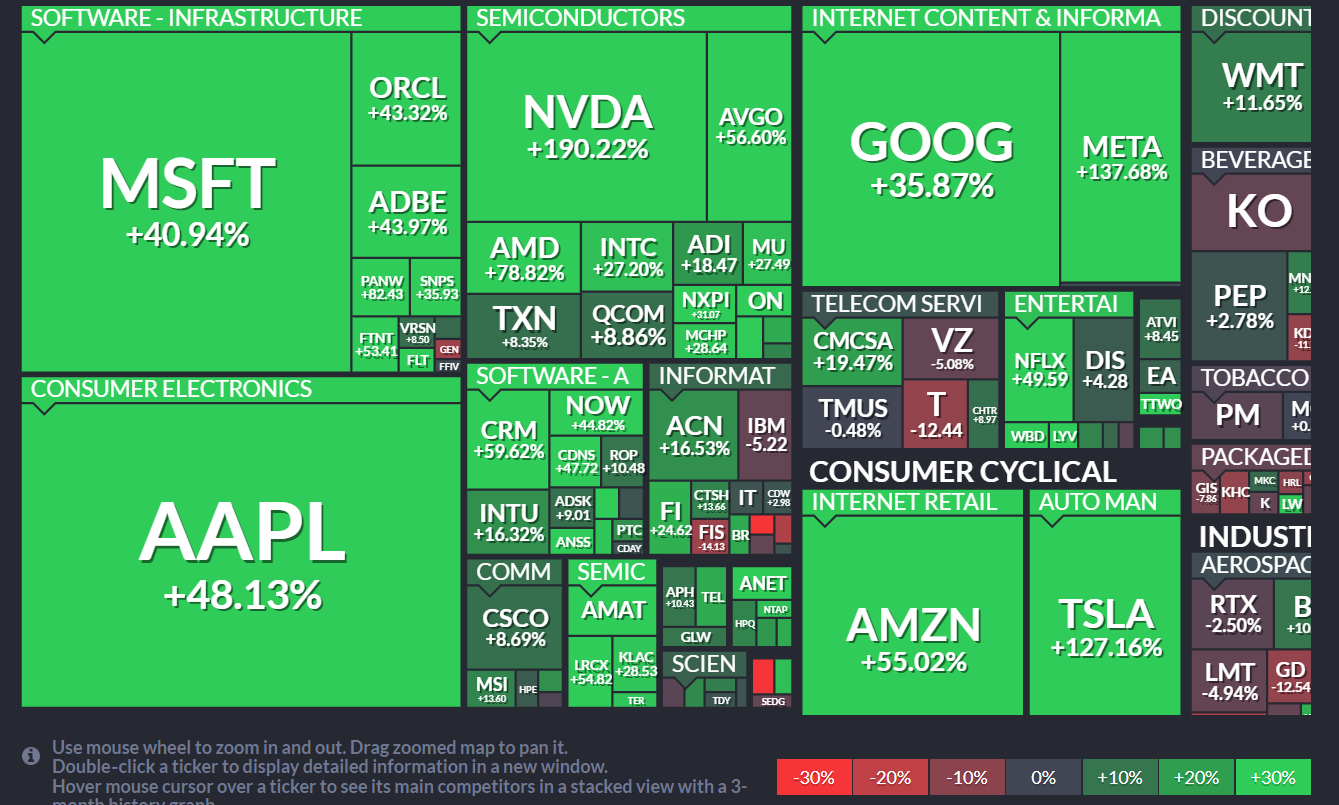

Meta is the second YTD best player in big techs

The rebound in 2023 has been dominated by major tech companies, turning the earlier "recession expectations" into a mid-year bull market.

In fact, Meta is not as well-liked by Americans compared to companies like $Apple(AAPL)$ . Unlike Apple, which is well-received, $Meta Platforms, Inc.(META)$ is controversial and has tense relationships with other major companies and even politicians. Apple's privacy policy posed the biggest challenge, while $Alphabet(GOOG)$ directly competes with Meta in the advertising industry, and $Amazon.com(AMZN)$ e-commerce transition has made Meta's progress difficult. It even had a close encounter with Atlas Energy (ATLS).

Despite being a controversial company, Meta achieved a reversal with a growth rate of over 137% in 2023, second only to $NVIDIA Corp(NVDA)$ . Unlike high-volatility stocks like tsla and nvda, Meta achieved this turnaround with exceptionally stable low volatility, making it the "safest happiness" for investors.

Overcoming adversity and challenges

2022 was a challenging year for Meta. Apart from the impact of inflation, the company faced performance decline due to iOS privacy policies. However, after several quarters of operations, Meta overcame significant challenges, and the actual impact of privacy restrictions was smaller than the market's pessimistic expectations.

Two important points to consider:

1. The company has a large and extensive user base, allowing it to provide services more accurately than its competitors based on historical data alone.

2. AI advancements are crucial in providing targeted advertising.

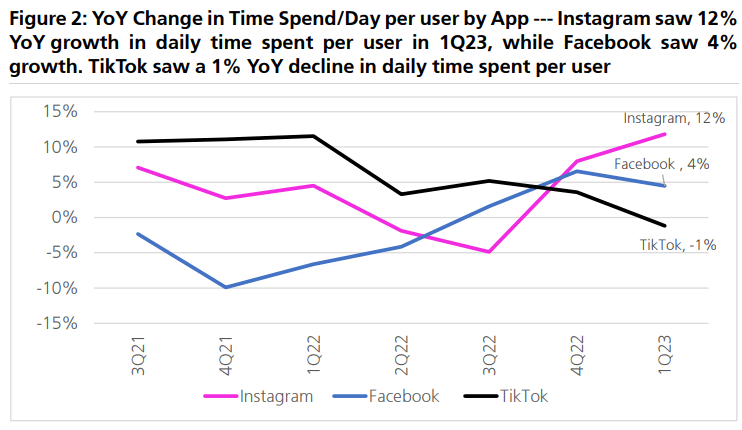

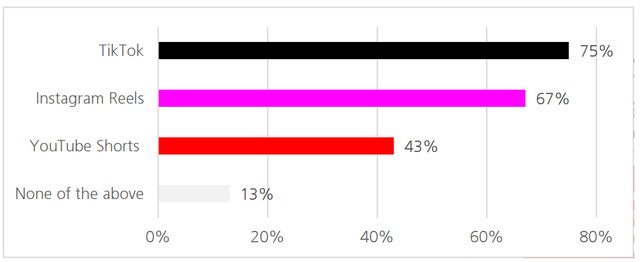

Apart from the challenge posed by Apple, another major challenge for Meta is TikTok. This led Zuckerberg to take off his mask and engage in conflict with China. TikTok's rapid growth became Meta's biggest competitor in the social networking field. Due to restrictions on TikTok in Western markets, Meta's Reels experienced significant growth. If Meta can successfully build a viable alternative to TikTok and make substantial progress, it will be a tremendous advantage for the company's long-term future.

Furthermore, compared to TikTok, Instagram has higher monetization and user engagement.

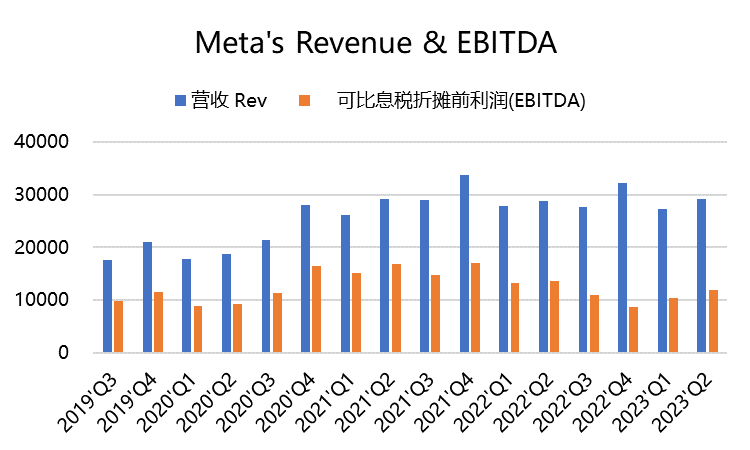

In the third quarter of 2022, Meta announced that Reels generated an annual revenue of $3 billion, with a negative impact of approximately $500 million per quarter, which is expected to be offset by the end of 2023 or early 2024. By the end of 2023, Reels is projected to contribute $5 billion to the company. Additionally, AI recommendations have increased Instagram's usage time by more than 24%, improving engagement metrics and attracting more advertisers.

However, controversies regarding monopolies persist. Meta has faced significant regulatory pressure in recent years. While fines and restrictions still exist in some regions, their overall impact on the company's performance may not be substantial.

An alternative of AI

Unlike hardware providers like NVDA, Meta's progress in the field of AI isnot direct or fast, but it may be one of the earliest to commercialize and reflect AI advancements in its performance.

In February of this year, Meta released the first version of its open-source large language model (LLM), called Meta AI (LLaMA). This model helps researchers develop cost-effective alternatives to proprietary AI software, creating a significant impact in the field of AI. Insiders reveal that Meta is exploring how to make the next version of its open-source large language model (LLM) commercially available, which could support chatbots like ChatGPT.

Meta's Chief Scientist, LeCun, also introduced the World Model, a "human-like" AI model called I-JEPA, which can analyze and complete missing images more accurately than existing models. I-JEPA performs exceptionally well in various computer vision tasks and is much more computationally efficient than widely used computer vision models.

In fact, Meta's AI-driven applications are more diverse than those of other companies, including its Oculus VR headset. With Microsoft criticizing the current size of the VR and AR market and Google terminating its AR project, Apple's recently released "Vision Pro" headset has become a significant competitor in the field.

Meta previously released the next-generation virtual reality headset, Quest 3, ahead of Apple. This headset features NVIDIA's GPU chip, doubling the processing power compared to Quest 2.

Recently, Meta may collaborate with $Tencent(00700)$ and make them the exclusive distributor for the Meta Quest series of headsets, as well as develop VR games for Quest headsets. However, the extent to which Meta can reduce or eliminate the substantial losses in its Reality Labs division will determine its ability to improve operational efficiency. In Q1, the division incurred a per-share loss of $4 billion.

Takeover Twitter

Meta is actively seeking to build a platform as an alternative to Twitter, leveraging its existing customer base of over 3.5 billion across all its platforms.

Successfully cloning Twitter would not only increase the company's profits but also convey the message to investors that the social media ecosystem is a winner-takes-all system. Within this system, newly built social media functionalities in the coming years can be integrated into Meta's platform.

Is there still potential in valuation?

Meta boasts a strong balance sheet, with a majority of its assets in cash and very low liabilities, allowing the company to generate significant interest income in a high-interest rate environment.

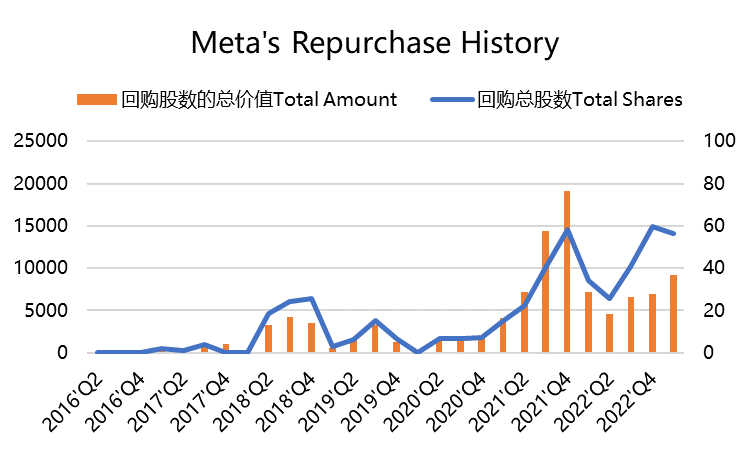

Due to its ample cash reserves, the company has been engaging in share buyback activities, reaching its peak in 2021. Despite a decrease in buybacks as investors returned after 2022, Meta's stock price continued to rise.

In terms of valuation, the company's current Price-to-Earnings (PE) ratio on a trailing twelve-month (TTM) basis is 25.8 times. After implementing cost-cutting measures, consensus estimates have doubled EPS forecasts.

Based on the consistent EPS expectations of $11.9, $14.9, and $17.2 for the fiscal years 2023-2025, the current PE ratios are 24 times, 19 times, and 17 times, which can be considered reasonable. Considering the company's long-term growth potential, this valuation is relatively low.

If Meta can achieve an earnings per share of $20 by 2025, the current price of $286 would still be considered cheap.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Apple is bigger company than Nvidia so if Apple trades at $192 it is cheaper than nvidia at $400 , so I think Apple should go much higher from current price. ( Logic of an apple investor)

Recent developments that include restructuring, layoffs, cutting back on lavish spending on metaverse (that was primarily respopnsible for decline in margins), and redirecting efforts on AI bode well for Meta.

Nvidia is not an AI chip company, but is rather a supercomputer manufacturer. Nvidia will be years ahead of where it is now. Quite honestly, and without hyperbole, Nvidia has the potential to become the most valuable company that ever existed.

All the cloud computing companies know full well how powerful Nvidia is becoming, and are very troubled by it.

Doesn’t seem to be great. Hope the bad things will not happen

Crazy that NVDA is about to surpass AMZN in market cap.

Great ariticle, would you like to share it?