Divergence in ADP and NFP jobs data? How will the market perform?

Last week, there was a certain degree of discrepancy in the two employment data released by the United States.

Thursday, the ADP Non-Farm Employment Change data greatly exceeded expectations. After seasonal adjustment, private sector employment increased by 497,000 in June, more than twice the market's expectation of 225,000 and far surpassing the previous value of 278,000. It marked the largest monthly increase since July 2022 and significantly heightened market anticipation for the non-farm employment report to be released on Friday.

However, the non-farm data did not turn out as strong as anticipated. The newly added non-farm employment in the report released on Friday unexpectedly declined to 209,000, reaching a two-year low. Nevertheless, the unemployment rate slightly decreased as expected to 3.4%.

Overall, although the growth has slowed down, it remains robust, and the pressure for wage increases is significant. It has provided almost no reason for the Federal Reserve to continue pausing interest rate hikes in July. The rate hikes are expected to resume this month.

Such discrepancies between these two data sets, despite having similar trends, are not uncommon.

The ADP employment report mainly focuses on the employment levels in the private sector and is based on wage data from over 400,000 American companies. The primary method of data collection relies on the wage data provided by payroll processing service companies.

Non-Farm Payrolls (NFP) report is generated and published monthly by the Bureau of Labor Statistics (BLS), offering an overview of employment situations, including the unemployment rate, average hourly wages, and the number of jobs added or lost on a monthly basis. The data collection method primarily relies on the Current Employment Statistics program and the Current Population Survey (also known as the Household Survey).

The June non-farm report, released this time, indicated a decline in employment in non-durable goods, wholesale and retail trade, transportation and warehousing, and temporary support services sectors.

Employment growth mainly stemmed from industries with relatively smaller cyclical fluctuations, such as education, healthcare, and government sectors. However, in the ADP employment report, the leisure and hospitality industry added 232,000 jobs, the construction industry added 97,000 jobs, and the trade, transportation, and utilities industry added 90,000 jobs. Conversely, the manufacturing, information technology, and financial industries experienced declines.

From an industry perspective, seasonal employment positions may be a significant contributing factor.

An interest rate hike in July, what comes next?

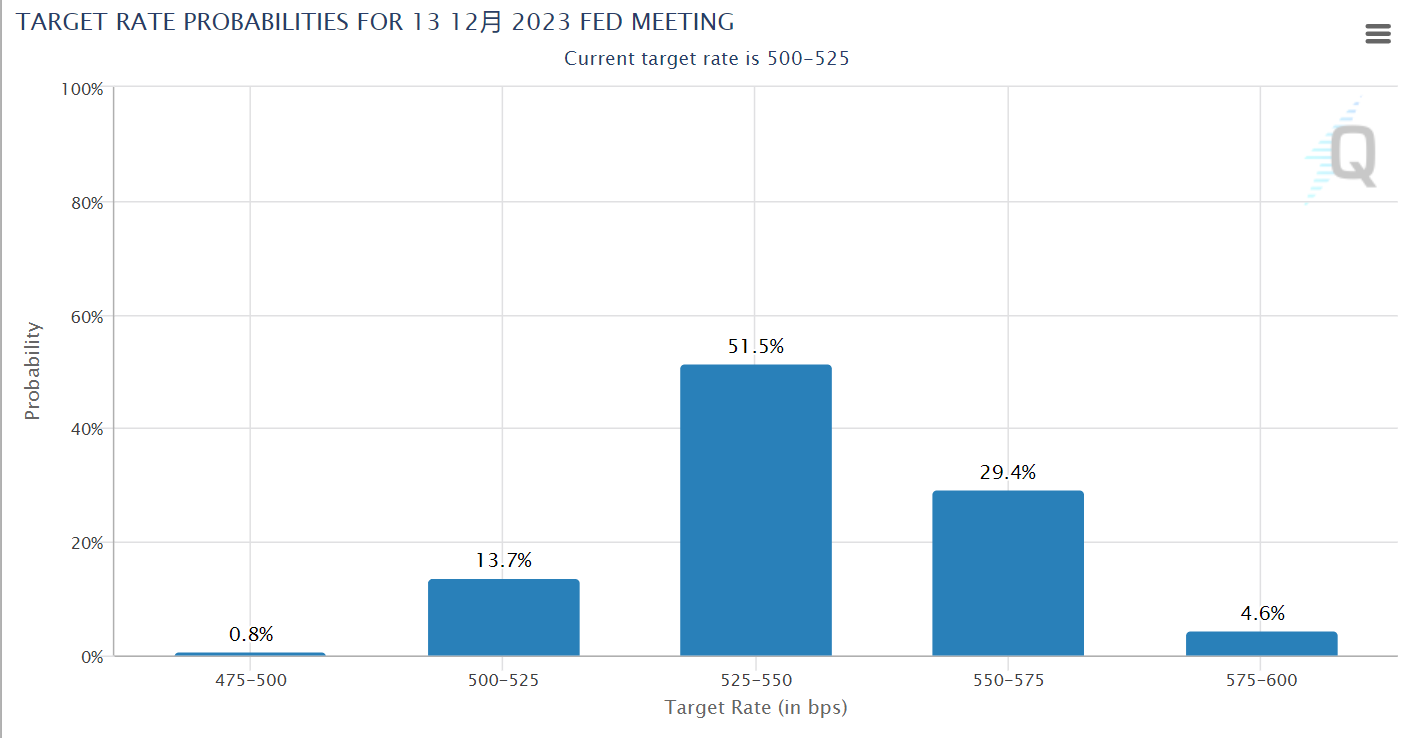

Due to recent U.S. economic data consistently exceeding expectations and various hawkish statements from Federal Reserve officials, market expectations for an interest rate hike in July have surged to over 90%.

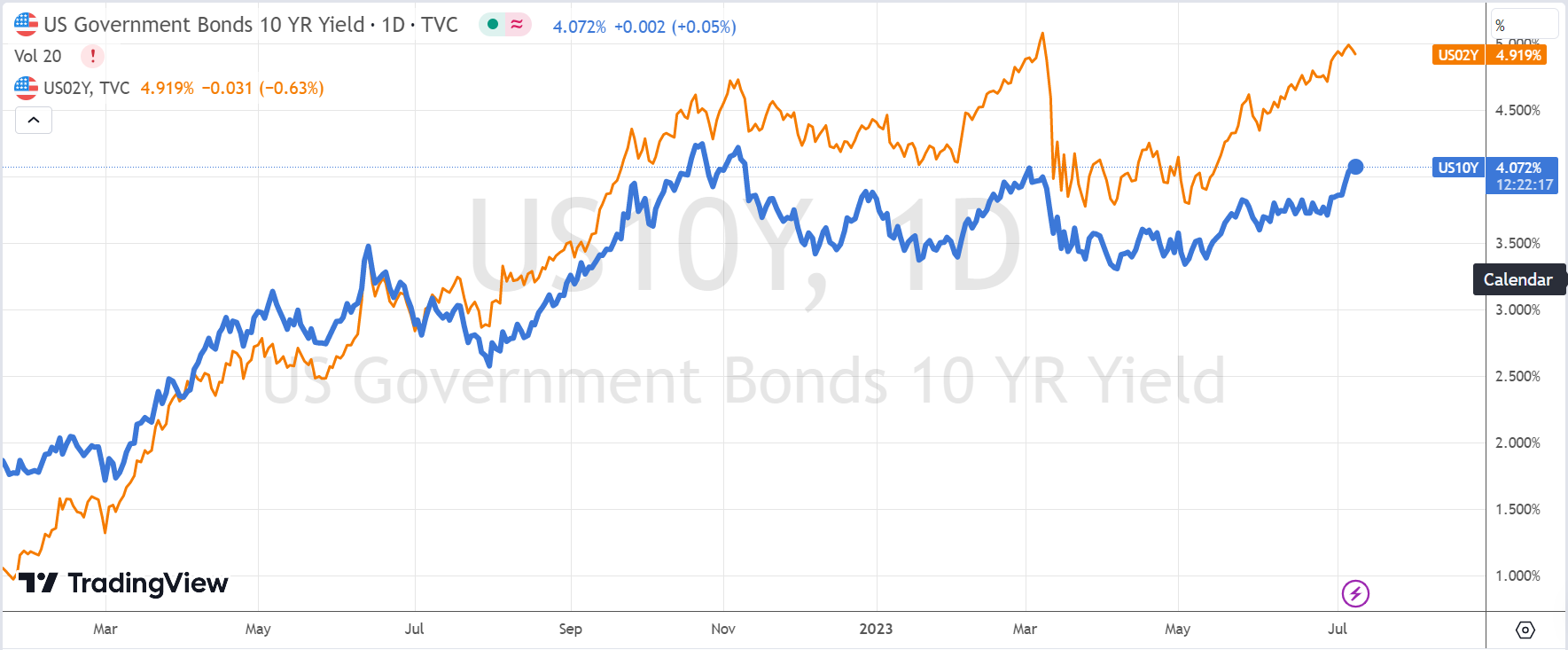

The interest rate hike in July appears imminent. July is also a critical period for policy decisions, with U.S. bond yields reaching new highs. The 2-year Treasury yield has surpassed 5% once again, while the 10-year Treasury yield is approaching 4%. These figures fully account for the interest rate hike in July and also mark a delay in the timing of interest rate cuts.

Last week, U.S. Treasury Secretary Janet Yellen's visit to China also became a global focal point. The U.S. side stated that it is not seeking to "decouple" from China, as such a decoupling between the world's two largest economies would be catastrophic and bring instability to the world. Yellen, who has previously served as the Chair of the Federal Reserve, proactively engaged in this communication at a time when differences in monetary and fiscal policies between China and the United States have been widening. This action holds positive significance and can provide a more stable signal to major economies. As for Jerome Powell, the head of the Federal Reserve, he can obtain more information about China from his former boss, Yellen.

However, the market may not receive clear signals of optimism or pessimism in the short term. Due to the current policy window, the market is likely to continue experiencing a volatile and fluctuating pattern.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Why do I get a gut feeling VIX is about to spike up? All big banks passed the stress test but there was no mention of the hundreds of regional, community small banks. How are they doing, I wonder? Is this banking crisis isolated only in the US? I don't think so.

That figure is just so out of range, one has to wonder if it's creditable. Dig into the detail.

Everyone thinks a tame CPI number will trigger the next leg up. Oh, if only it were that easy.

No chance on God's green earth that figure is even remotely accurate

Lets wait for PMI to know where the market is going