Why Upstart Is Still Uninvestable?

On August 9th, $Upstart Holdings, Inc.(UPST)$ experienced a significant 34% drop in trading due to its Q2 earnings report falling short of expectations and revealing a downturn, along with Q3 guidance below market expectations.

Additionally, as a Fintech-focused company, UPST has ventured into traditional banking and lending after the banking industry crisis, which has raised doubts among investors about its asset quality.

Q2 Earnings Overview

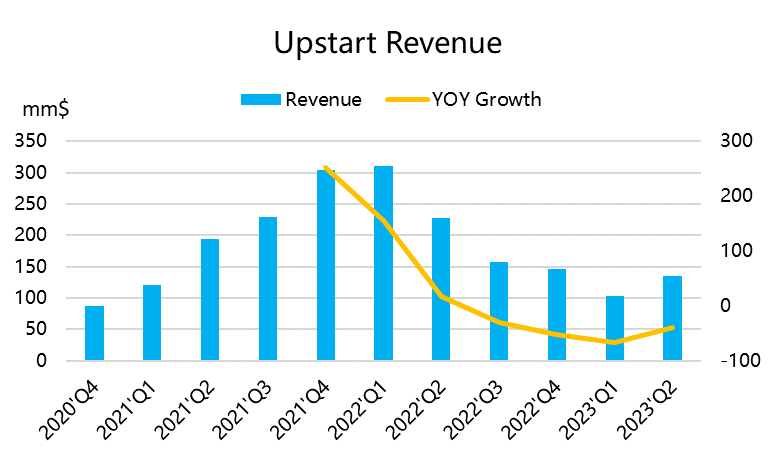

- Quarterly revenue was $135.8 million, a YoY decrease of 40.5%, slightly below the Bloomberg consensus estimate of $135.9 million.

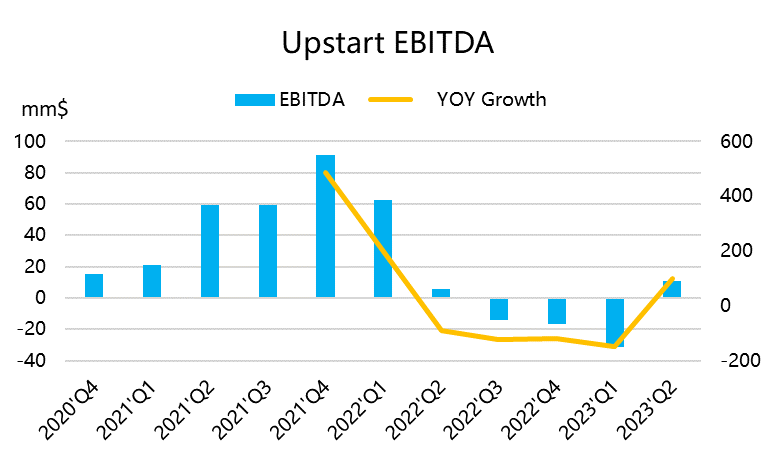

- EBITDA stood at $10.97 million, surpassing the market's expected $0.65 million.

- Adjusted EPS reached $0.06, exceeding the market consensus of $0.07.

- Loan volume was $1.176 billion, a 64% YoY decrease but an 18% increase QoQ; loan count increased by 30%, resulting in a 9% QoQ decrease in individual loan size.

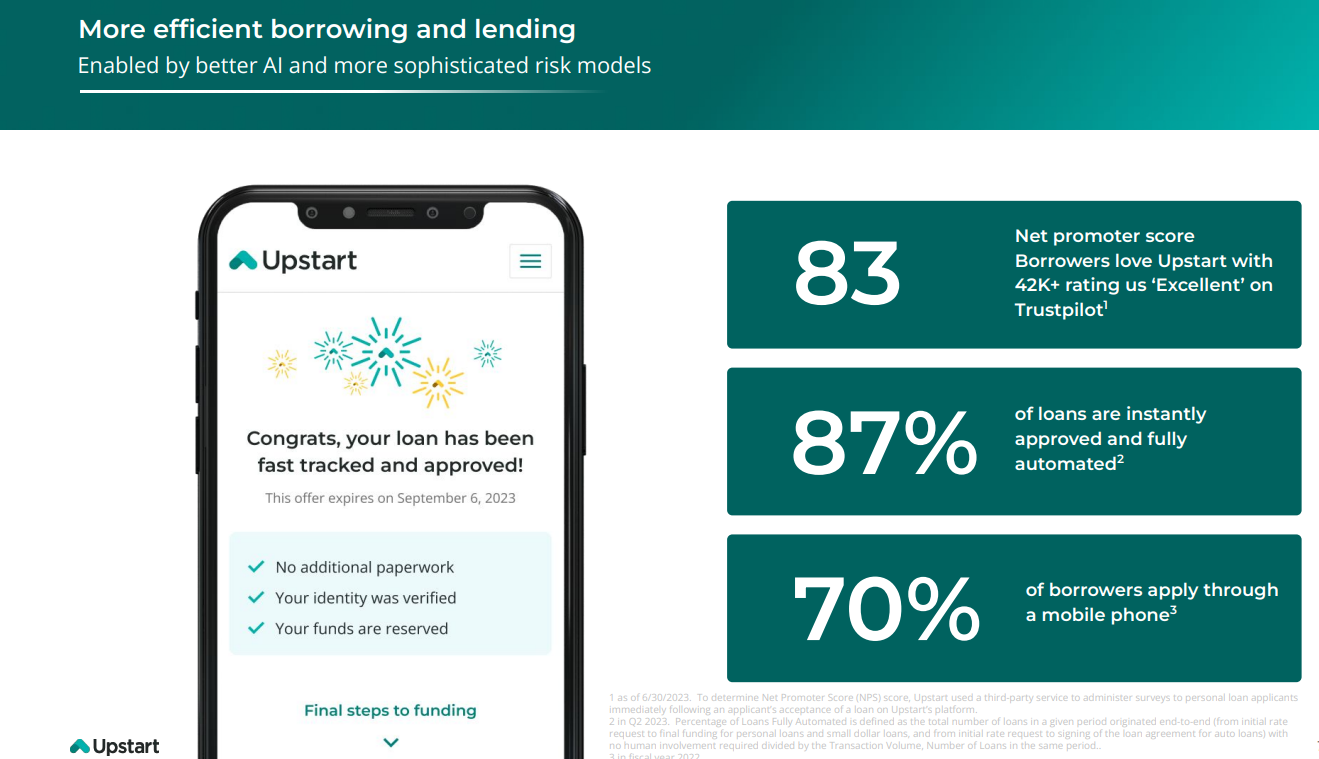

- The proportion of automated underwritten loans rose to 87%, and the company introduced a home equity loan tailored to the real estate market, enabling loan approval within 10 minutes and fund disbursement within 5 days.

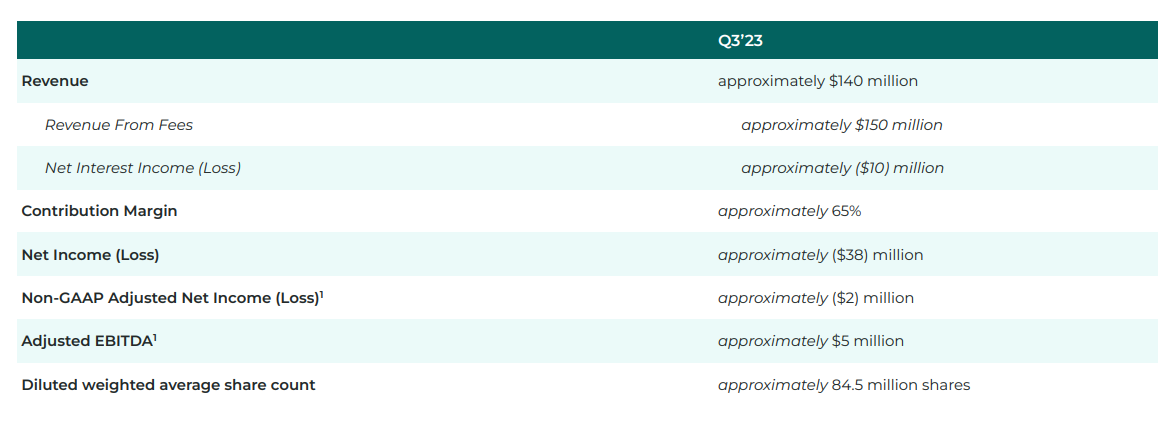

Guidance-wise, due to a lack of committed capital, the company's outlook for Q3 is less optimistic, with revenue projected at only $140 million, falling short of the market's $150 million expectation. Adjusted EBITDA for Q3 is anticipated to be only $5 million, almost half of Q2's $11 million.

Investment Highlights

On the positive side, the company rationalized its operations, increased automation, enhanced its underwriting model, and seems poised to swiftly enter the market with improved macroeconomic conditions.

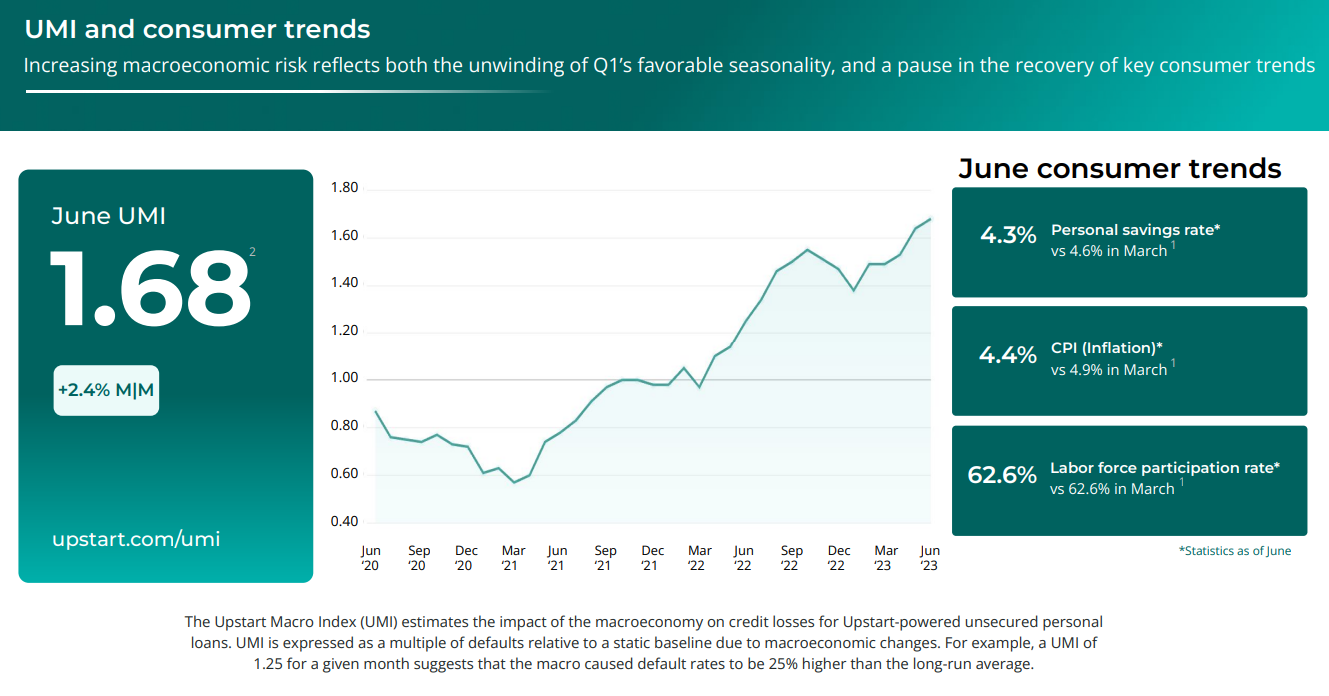

Although liquidity issues have mostly been addressed, market sentiment for lending among small and medium-sized banks has yet to fully recover. Post the banking industry crisis, the funding market remains relatively tight, with sellers continuously supplying loans for liquidity, creating challenging market dynamics. Some banks are also trading ABS at lower prices for liquidity.

A high-interest rate environment might not favor the company. Higher fees/annual rates lead to borrowers accepting fewer loans, gradually weakening credit trends, and often making third-party funding "costly." The company has set a 36% APR annualized interest rate cap, which also restricts its profit potential in a high-interest rate scenario. Moreover, the cautious approach toward Q3 guidance stems from the recovery time of borrower delinquency trends and the overall health of the funding market in the short term.

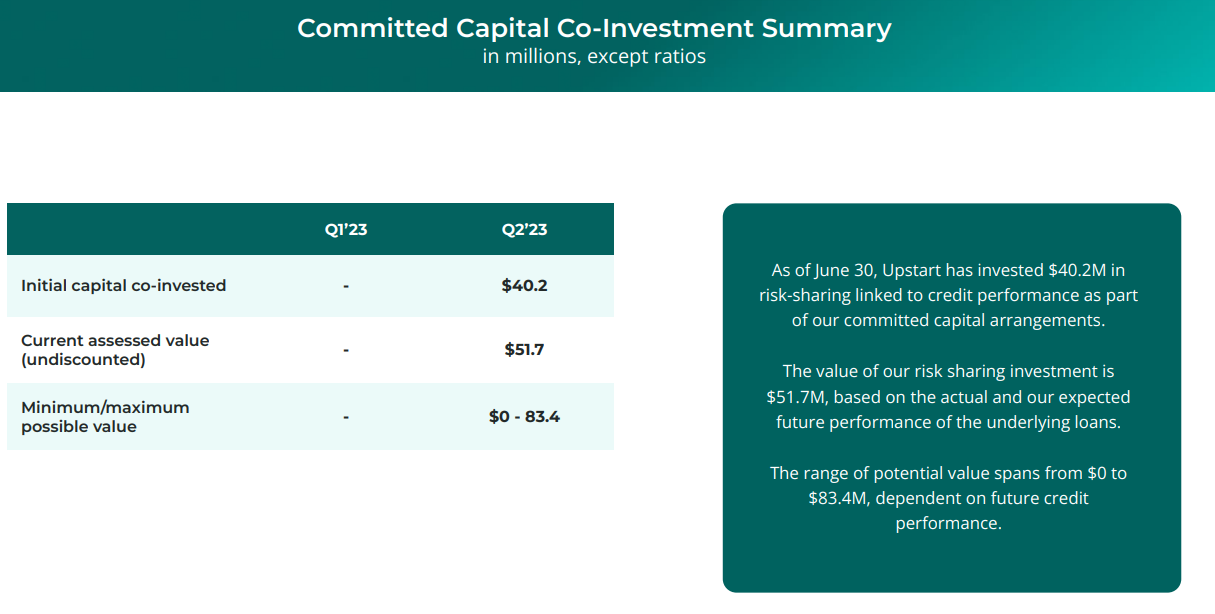

The company is now funding loans with its own capital. Originally assisting ABS transactions, UPST has taken unconventional steps due to the environment by using its assets for trading. Furthermore, the Q1 commitment of $2 billion in new capital from a partner only reached $850 million by Q2's end. The company is also co-operating on this portion of loans with its assets, implying a shared risk. If this portion is subordinate, it might ultimately go to zero during liquidation.

Summary

1. The company's stock price surged significantly after Q1 earnings, rising from $13 to $72. This was driven by factors such as short covering, enthusiasm from meme stock investors, and improved expectations of the company turning profitable.

2. The slowdown in Q2 performance makes it even harder to support the overvaluation. Moreover, current risk factors haven't diminished. The company has also taken on a risky role by becoming a direct loan provider to small and medium-sized banks, which has increased the risk on its balance sheet.

3. In the long run, there is still a trend of funds flowing back from small and medium-sized banks to large banks. An improvement in lending sentiment is only possible after a decrease in interest rates, but the probability of a rate cut by the Federal Reserve this year is extremely low.

Therefore, UPST is still in a situation of poor sentiment and high valuation. Despite being profitable, its performance is not stable, leading to increased volatility in its stock price.

Although the stock price has fallen back to $34, it is still at the level of the end of June. The increase in value since the beginning of the year has been substantial, leaving significant room for a pullback. As the broader market experiences a correction, the likelihood of significant fluctuations in its price remains high.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

If you want to go long my advice is wait till it is at least below the original IPO price. If you want to go short my recommendation is to wait till it is above $70 AND appears to be stalled. Honestly I would never go short something like UPST.

I looked at the fundamentals and I don't know how this stock was ever $70. Based on the fundamentals, it should be about $10 per share.

I looked at the options. I definitely would NOT recommend writing calls are puts at the moment. I usually write options if I do anything with options. But writers over the last week or two are getting wiped out. And the options aren't reflecting the volatility at all. It might be good for those who are speculative to buy them.

This company is raking up losses. I wouldn't even touch it with a ten foot pole.

Fundamentals remain the same, yet the price is falling. It's a fantastic opportunity to buy more shares.