Maybe Alibaba's Most Important Earnings Ever: Why Should I Invest Here?

$Alibaba(BABA)$ has released its Q1 financial report for the 24th fiscal year, showing progress in open source and a comprehensive recovery in business while further improving profit margins. $Alibaba(09988)$

Summary

China's e-commerce business has achieved double-digit growth after being quiet for five quarters, but profit margins have declined due to industry competition and downward CPI;

International e-commerce achieved its highest growth rate ever at 43.8%, benefiting from cooperation with "One Belt, One Road" countries and the easing competition in Southeast Asian subsidiaries;

The strong e-commerce business also led to Cainiao Logistics turning losses into profits;

Local life and digital entertainment have benefited from the recovery demand after opening up, and strong offline entertainment has helped the historical turnaround of digital entertainment from losses to profits;

The growth rate of cloud intelligence has slowed down, but long-term profit margins have increased, and open of models and more AI application scenarios will become potential increments.

Earnings Rerview

Revenue

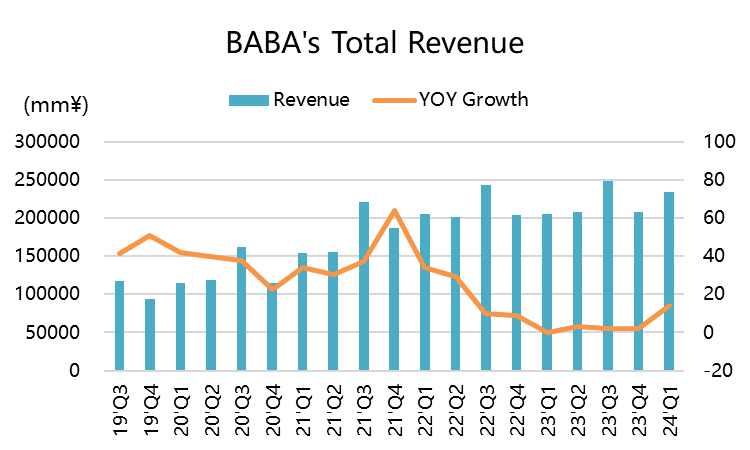

Total revenue was RMB 234.16 billion, a year-on-year increase of 14%, higher than the expected RMB 223.76 billion.

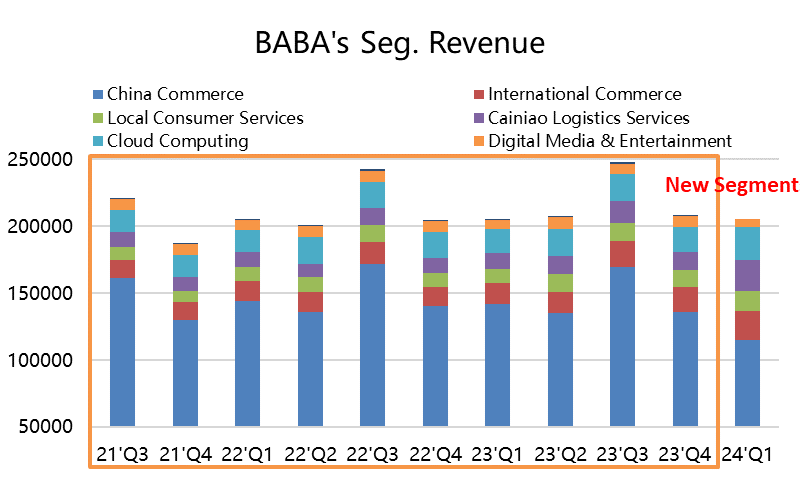

By Segment, including Taotian Group's Chinese commercial revenue of USD 114.95 billion, a year-on-year increase of 12%,

International commercial Sevice revenue RMB 22.12 billion, a year-on-year increase of 41% including Lazada;

Local consumer service revenue was RMB 14.45 billion, a year-on-year increase of 30%;

Cainiao Logistics revenue was RMB 23.16 billion, a year-on-year increase of 34%;

Cloud Computing revenue was RMB 25.12 billion, a year-on-year increase of 4%;

Digital entertainment revenue was RMB 5.38 billion, a year-on-year increase of 36%;

Profit

Gross margin 39.21%, a year-on-year increase of 229bps, higher than the consensus of 37.54%.

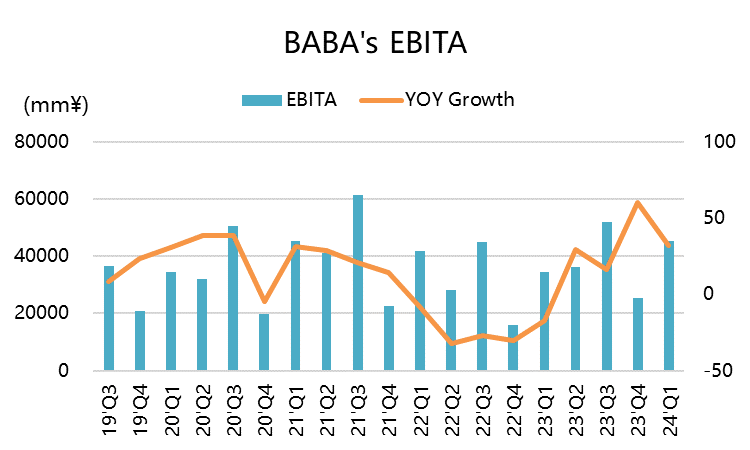

Operating profit was RMB 42.49 billion, a year-on-year increase of 70%;

adjusted EBIT was RMB 45.37 billion, a year-on-year increase of 32%;

Non-GAAP adjusted EPS was RMB 17.37, higher than the expected RMB 14.14;

By Segment, core Chinese retail contributed RMB 49.32 billion, a year-on-year increase of 9%;

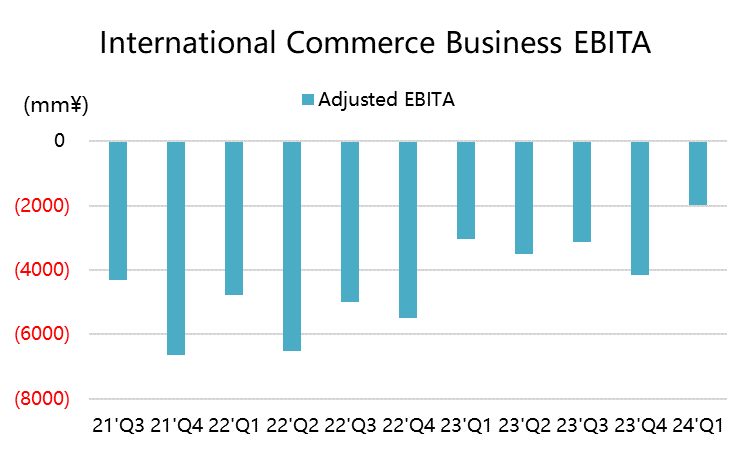

The international commercial department still had a loss of RMB 420 million, but it decreased by 70% year-on-year, higher than the market expectation;

Local services had a loss of RMB 1.98 billion, a year-on-year decrease of 30%;

Cainiao Network had a profit of RMB 880 million, turning losses into profits year-on-year;

Cloud business profit was RMB 390 million, a year-on-year increase of 106%;

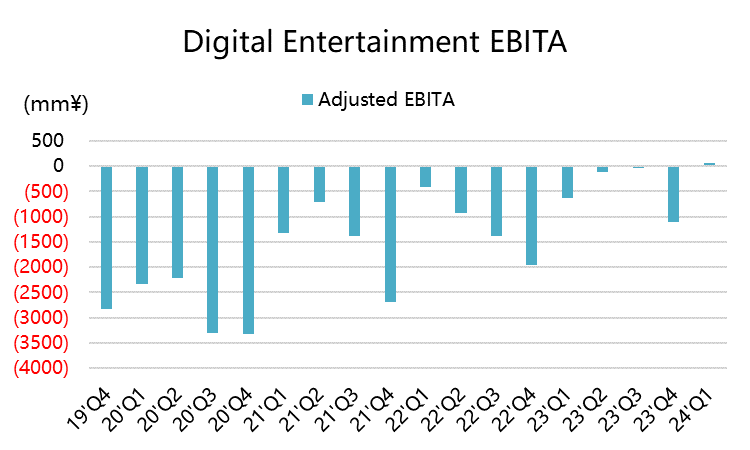

Digital entertainment profit was RMB 60 million, turning losses into profits year-on-year.

From the perspective of pre-tax profits, both Cainiao Network and digital entertainment have turned losses into profits.

Investment Highlights

China retail business is improving, but "consumption downgrading" and "de-inflation" exist

Alibaba stopped disclosing GMV several quarters ago, so there is a lack of comparative indicators. However, at the end of the 23rd fiscal year in the previous quarter, the retail business in China even declined by 5% year-on-year, which is in line with the overall social retail trend. But in FY24Q1, it grew by 10% year-on-year, with Taobao DAU growing by 6.5% and Xianyu contributing 18% of DAU. It seems that consumption is still active.

When there is the 618 shopping festival in the second quarter, general consumer activities will be stronger. At the same time, compared to last year, which was still constrained by the epidemic, this rebound is still understandable.

However, EBIT margin is declining (revenue increased by 12%, but profit increased by 9%. The company emphasized the increase also includes ads, the sales prices must be declining), which is related to the current competition with $Pinduoduo Inc.(PDD)$ , and Douyin, where products with lower profit margins sell better or some products have actually decreased in selling prices, which is also consistent with the CPI data.

This is also why although Alibaba's financial report reflects strong overall growth data, Taobao's group will actively reduce profits and achieve good results when facing competition from later entrants. However, there is still a risk of consumption downgrading and deflation in the overall consumption environment.

Suprising International Commerce Business

FY24Q1 saw a 25% increase in orders. Looking at cross-border e-commerce transactions, Alibaba has made a lot of efforts to attract more foreign businesses to enter China or to export domestic products. Of course, the main growth areas are not Europe and the United States, but regions with higher resident wealth or population bases such as the Middle East, Central Asia, and Southeast Asia.

Lazada and Trendyol overseas also recorded double-digit growth, which was also due to the improvement of profit situation in Southeast Asian e-commerce by reducing costs and increasing efficiency, such as $Sea Ltd(SE)$. In addition, due to the relatively high US dollar exchange rate, it is more obvious on the profit and loss statement denominated in RMB. The narrowing of losses, in addition to reducing operating costs, also reflects economies of scale.

Local comsuption services benefited from Post-Covid activity.

Revenue reached 14.45 billion yuan. Ele.me, Amap and Fliggy all contributed greatly to growth. The entire local life segment saw a 35% increase in orders and a 30% increase in revenue. This industry-wide recovery will also be reflected in the financial reports of companies such as Meituan, Didi, and Ctrip in the future.

Although it still lost 1.98 billion yuan this quarter, the trend of losses is narrowing. At this rate, it is expected to achieve profitability in the next 4-8 quarters.

Cainiao Became More Independent

Alibaba's logistics subsidiary, Cainiao, has long been considered the business with the fastest potential for independent spinoff and public listing. In this quarter, Cainiao achieved a revenue of RMB 23.16 billion, a year-on-year increase of 34%, with the strength of this business depending heavily on the intensity of e-commerce (especially international e-commerce).

At the same time, this quarter's return to profitability provides a good foundation for the entire fiscal year's profitability and future sustained profitability. Since Cainiao independently disclosed its performance, only Q2 of 23 fiscal years has been profitable.

")

Cloud business has begun to focus on monetization, AI brings new opportunities.

Including Alibaba Cloud's smart cloud business, which includes DingTalk, it grew nearly 4% this quarter (less than the group's consolidated business, adjusted caliber). In fact, Alibaba Cloud has long been anxious about growth and expansion and has turned to monetization efforts.

Its Q1 EBIT profit doubled, similar to the momentum of $Amazon.com(AMZN)$ AWS in its early days of profitability.

This quarter's profitability comes from the recovery of DingTalk usage and the reduction of bandwidth costs, which means long-term profit margins will improve.

What’s interesting is that, From Alibaba Cloud's explanation, we can also see the overall industry trend. The demand for CDN has "returned to normal year-on-year," meaning that commercial activities such as live streaming may be close to the ceiling (companies such as $JOYY Inc.(YY)$ ), while industries such as financial services, education, power, and electric vehicles are in a period of growth ( $XPeng Inc.(XPEV)$ ).

Currently, core technologies such as AI, cloud computing, and big data have become the biggest competition among major cloud service providers. The cloud market has undergone a major reshaping at the beginning of the year, and major companies have begun to embrace challenges and opportunities again.

After organizational restructuring, Zhang Yong took over Alibaba Cloud and immediately open-sourced two universal models with 7 billion parameters called OpenAIText and OpenAILab. Unlike $Meta Platforms, Inc.(META)$ open-source Llama2 targeting the future mature software potential in advertising business and VR, Alibaba itself is a cloud service provider and providing an open platform will directly benefit Alibaba Cloud.

Entertainment business has finally entered an era of prosperity.

Online entertainment services (including Youku and Damai大麦) and offline services (Alibaba Pictures) have both achieved historical profitability, with revenue reaching RMB 5.38 billion and EBIT reaching RMB 63 million.

From the intensive rise in performance activities this year to sold-out concerts, the explosive demand for offline entertainment activities will also boost the entire sector and will continue to be reflected in FY24Q2.

As for movies, Hollywood films' box office in China has been lower than expected this year, coupled with a lack of strong content output from important IP providers such as $Walt Disney(DIS)$ (Black Panther, Silver Armor 3 and other films have not achieved Marvel's historical performance), which has greatly increased the market share of domestic films and provided opportunities for Alibaba Pictures and others.

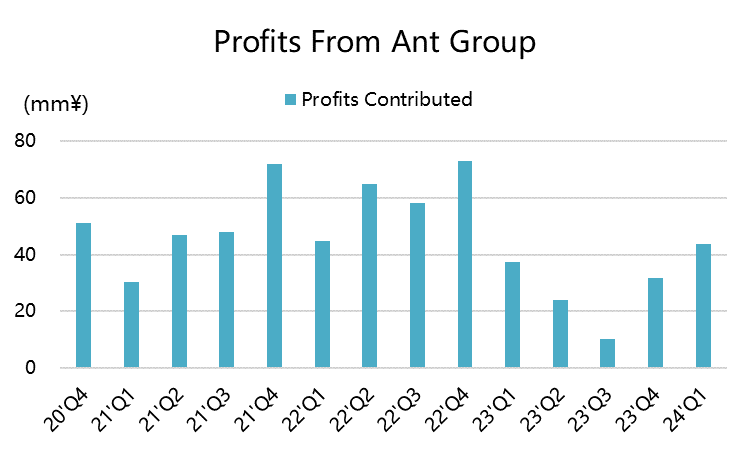

Ant Group's contribution will also increase.

In this quarter, Ant Group contributed a profit of RMB 4.36 billion, or USD 602 million, the highest value since the third quarter of 2021. With the July regulatory fines imposed on Ant Group (RMB 7.07 billion fines will be reflected in next quarter's financial report), the call for Ant Group's relisting is increasing. However, at present, Alibaba has also lowered its valuation of Ant Group and denied the listing rumors.

From a performance perspective, official encouragement of investment has also become another positive factor in the financial services sector, but the next major turning point may be the landing of Ant Financial's license.

Valuation

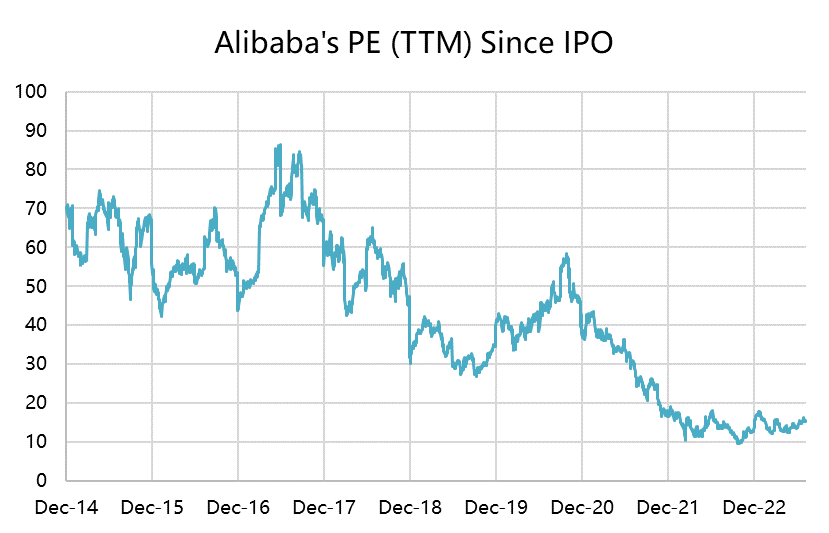

Alibaba's P/E ratio (TTM) has been below 20 times since November 2021, which is obviously not matched with the average P/E ratio of over 30 times for large tech companies in the US stock market.

Investors are also very clear about where the discount comes from and understand the situation, but we believe that in the long run, Alibaba's stock price will eventually return to the mean.

From the current regulatory attitude, the needs of the real economy, and the company's own operations, Alibaba is very likely to continue to achieve a double-click of performance and stock price in the next few quarters.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Great ariticle, would you like to share it?

这篇文章不错,转发给大家看看

Great ariticle, would you like to share it?