Why Market Beting Against Tencent Q2 Earning?

On August 16th, Hong Kong stocks closed with the announcement of Tencent Holdings' (00700) Q2 2023 financial report.

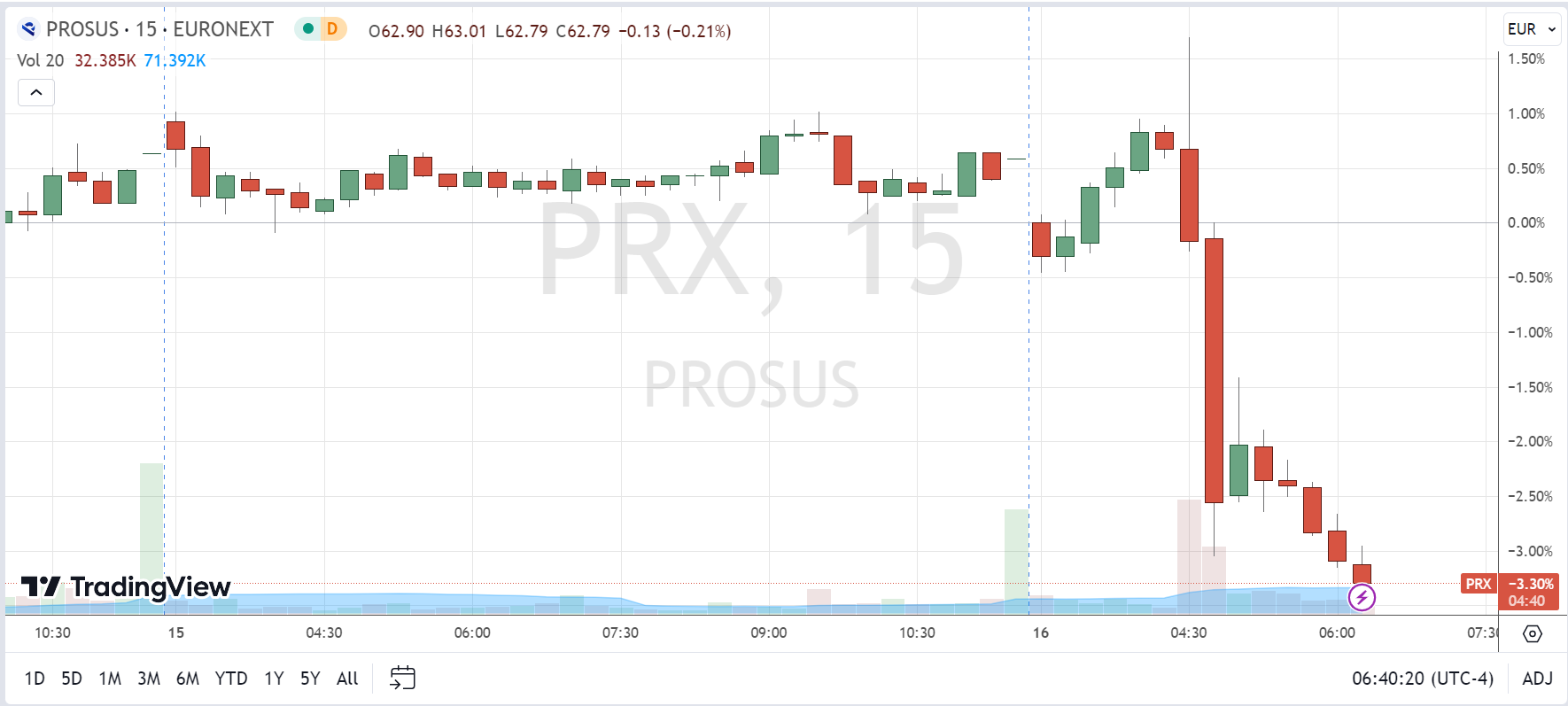

Following the demonstrated strength in the Q1 financial report's rebound and the overall recovery expectations for Q2, market anticipation was actually quite high. As a result, this financial report is a mix of both positive and negative sentiments. The major shareholder, $Naspers Ltd.(NPSNY)$ / $Prosus NV(PROSY)$ , plunged straight 3% in trading after the release, indicating an unfavorable initial impression from the market.

We Believe

Miss is primarily attributed to underperformance in the top-line. The revenue shortfall mainly arises from the gaming business and enterprise services, potentially due to seasonal effects in gaming and decreased optional consumer spending. Changes in the cycles of games outside Tencent's portfolio could also contribute to Tencent's performance, and its revenue ranking has improved July.

Tencent's efforts have yielded highly positive feedback. The advertising business has exceeded expectations significantly, with enhanced monetization of video accounts and increased e-commerce market share. These successes are the result of the company's active expansion of the WeChat ecosystem.

Although efficiency running efforts have likely reached an end, profit generation remains substantial, and contributions from joint ventures are expected to rise.

The reduction in holdings by major shareholders hasn't mitigated their own discount; after Tencent's financial report, stock repurchases can resume, potentially attracting some capital inflow. The company currently remains significantly undervalued.

Q2 Earnings Review

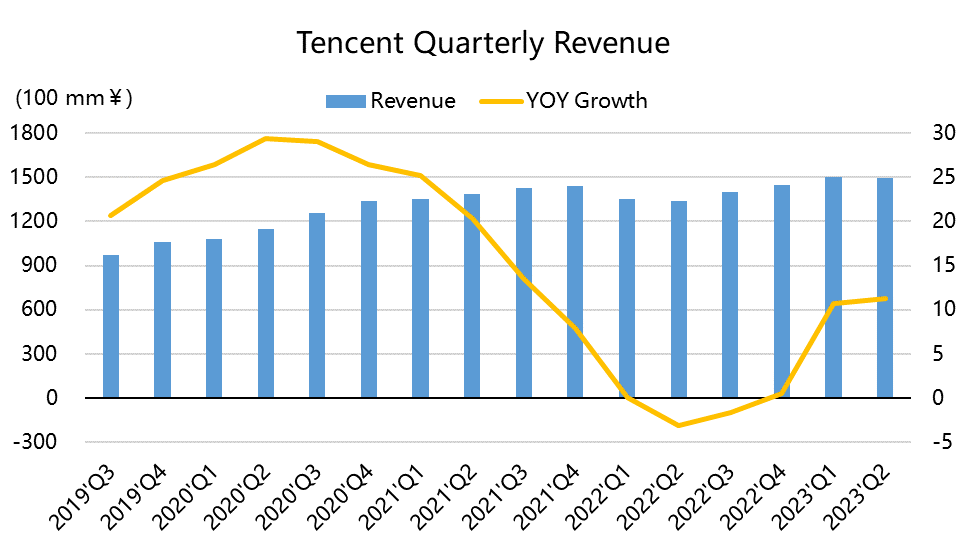

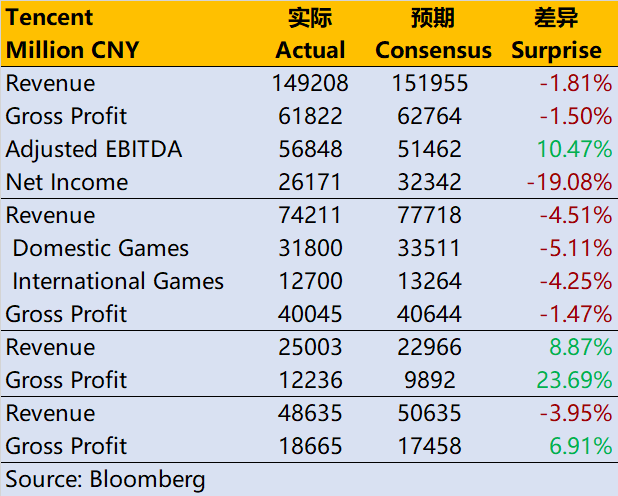

Revenue amounted to 149.2 billion yuan, a year-on-year growth of 11%, falling short of the market's anticipated 152.0 billion yuan. The year-on-year growth rate is on par with the previous quarter;

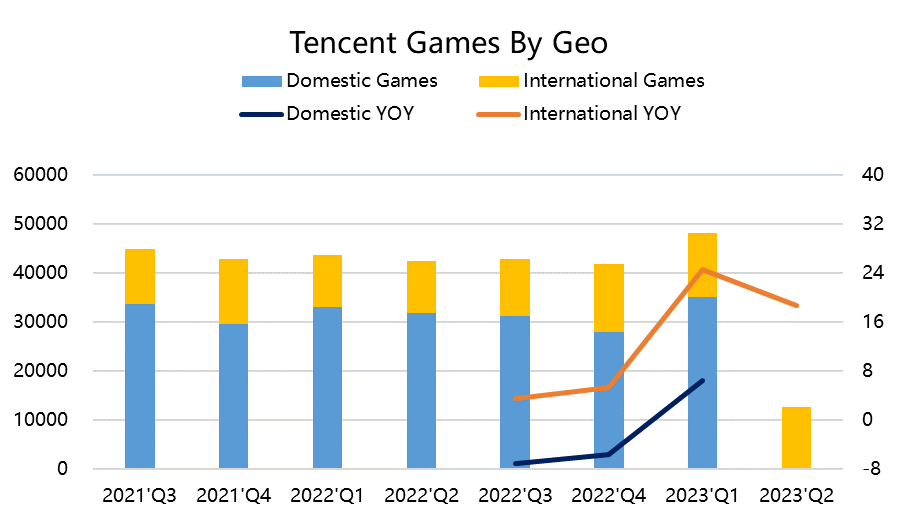

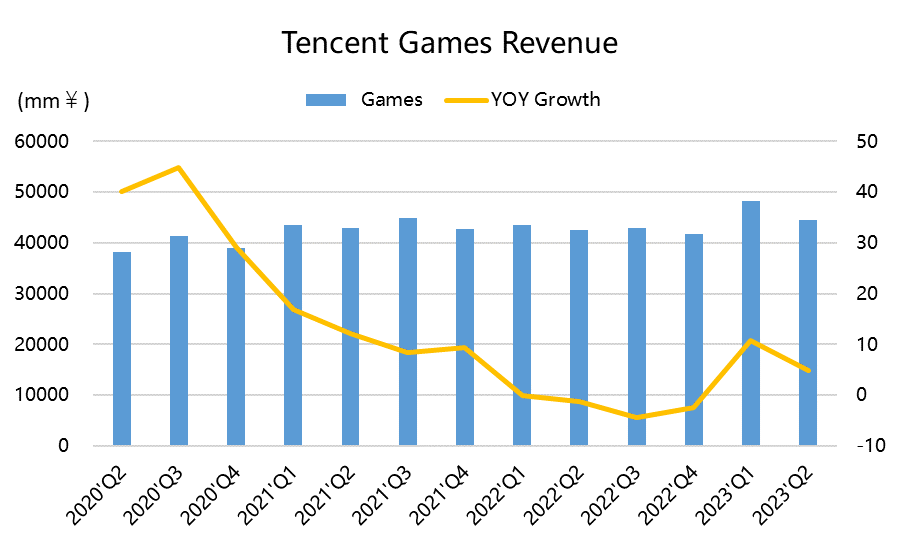

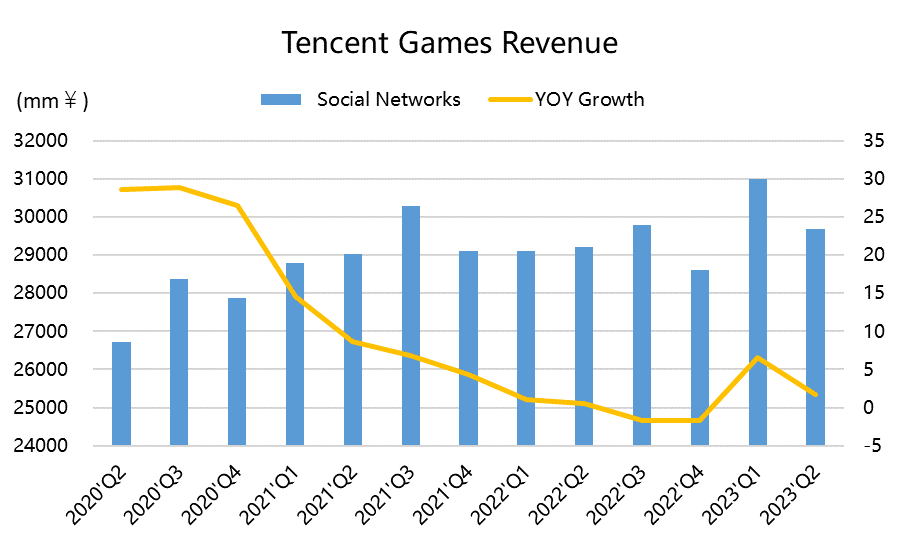

Among them, value-added business revenue reached 74.2 billion yuan, falling below the market's expected 77.7 billion yuan; local game revenue reached 31.8 billion yuan, maintaining a year-on-year stability, but not meeting the expected 33.5 billion yuan. Overseas game revenue reached 12.7 billion yuan, a year-on-year growth of 19% at neutral exchange rates; social network revenue reached 29.7 billion yuan, a 2% increase year-on-year;

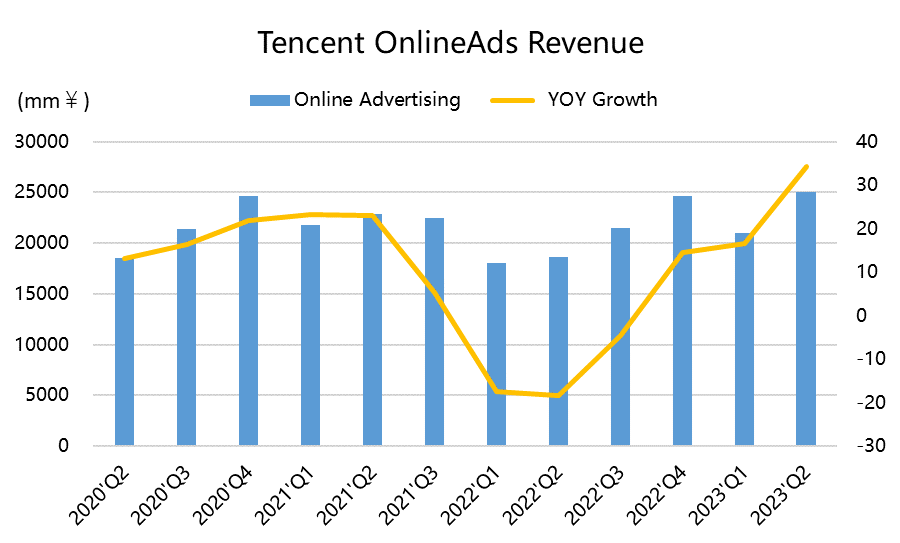

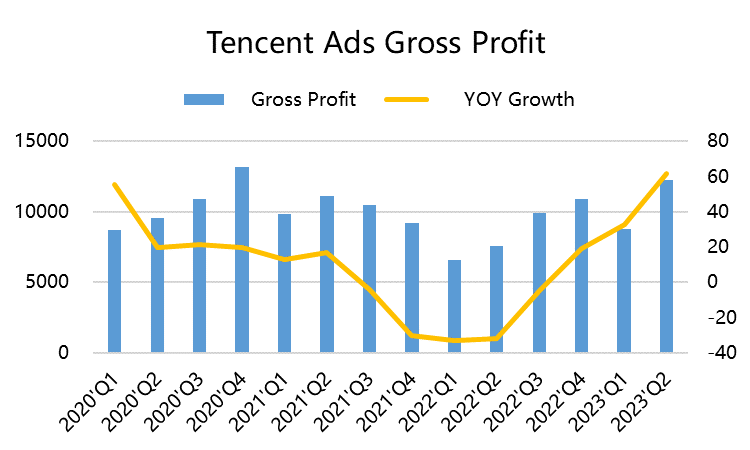

Network advertising business achieved 25.0 billion yuan, a 34% year-on-year growth, significantly surpassing the market's anticipated 23.0 billion yuan;

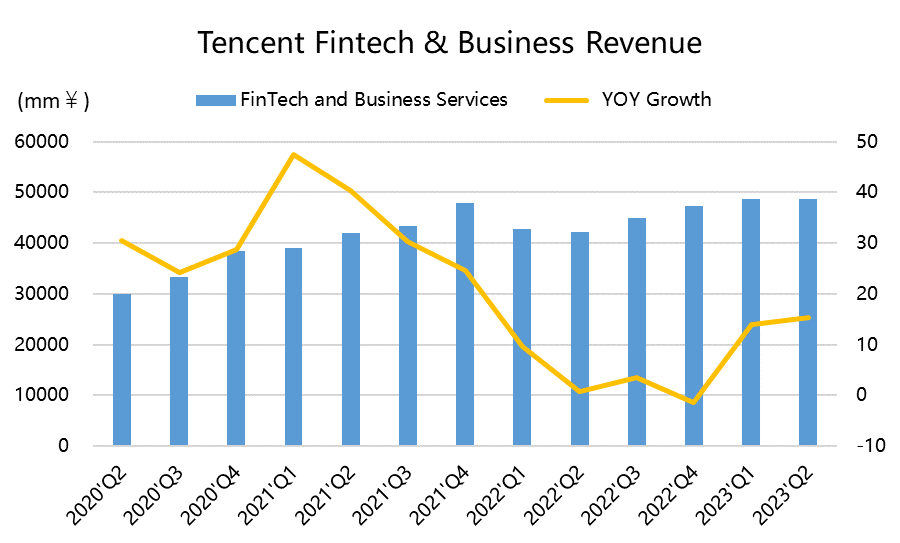

The revenue from financial technology and corporate services businesses was 48.6 billion yuan, marking a 15% year-on-year growth, which was below the market's anticipated 50.6 billion yuan.

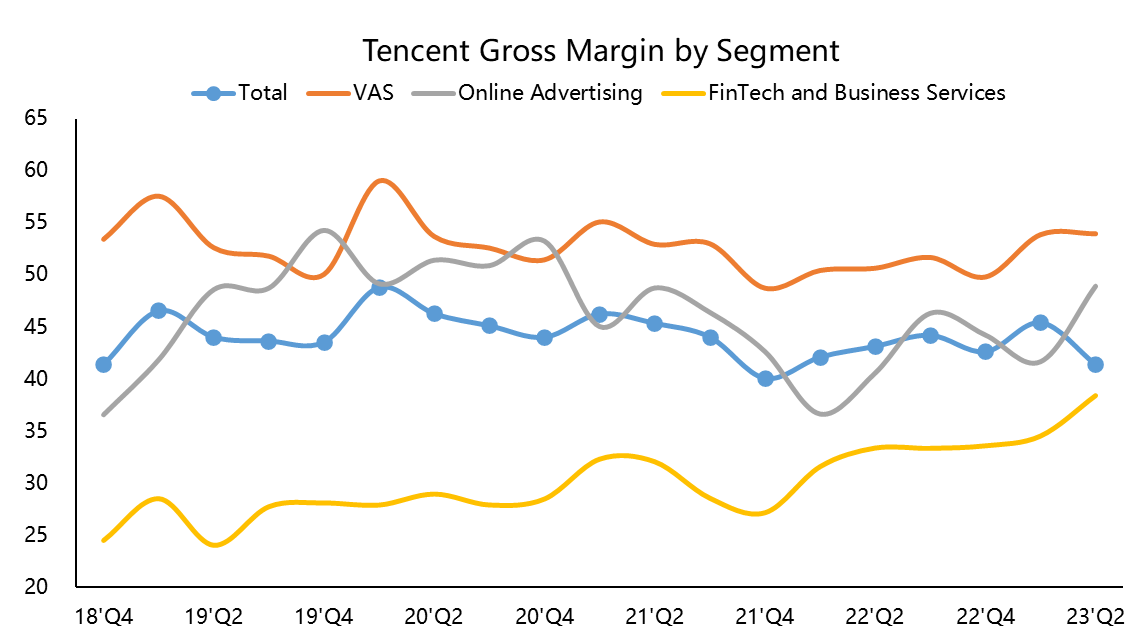

Gross profit margin reached 61.8 billion yuan, with a year-on-year growth that fell short of the anticipated 62.7 billion yuan, although the difference was smaller than the level of revenue increase.

During the period, the earnings reached 27 billion yuan, showing a 41% year-on-year growth. The net profit attributable to shareholders stood at 26.171 billion yuan, lower than the market's expected 32.3 billion yuan, but still exhibiting a 41% year-on-year growth.

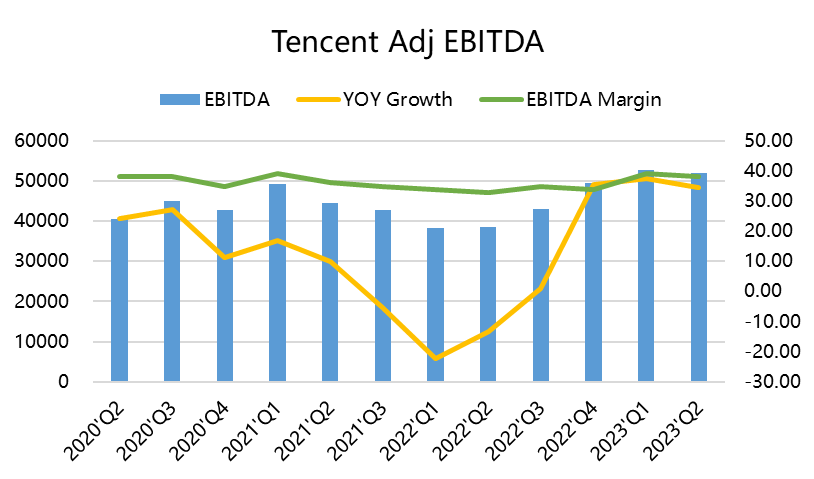

Non-IFRS earnings also reached 37.5 billion yuan, up by 33% compared to the previous year. Adjusted EBITDA surged to 56.8 billion yuan, exceeding the anticipated 51.5 billion yuan, and the profit margin increased from last year's 33% to 38%.

Investment Highlights

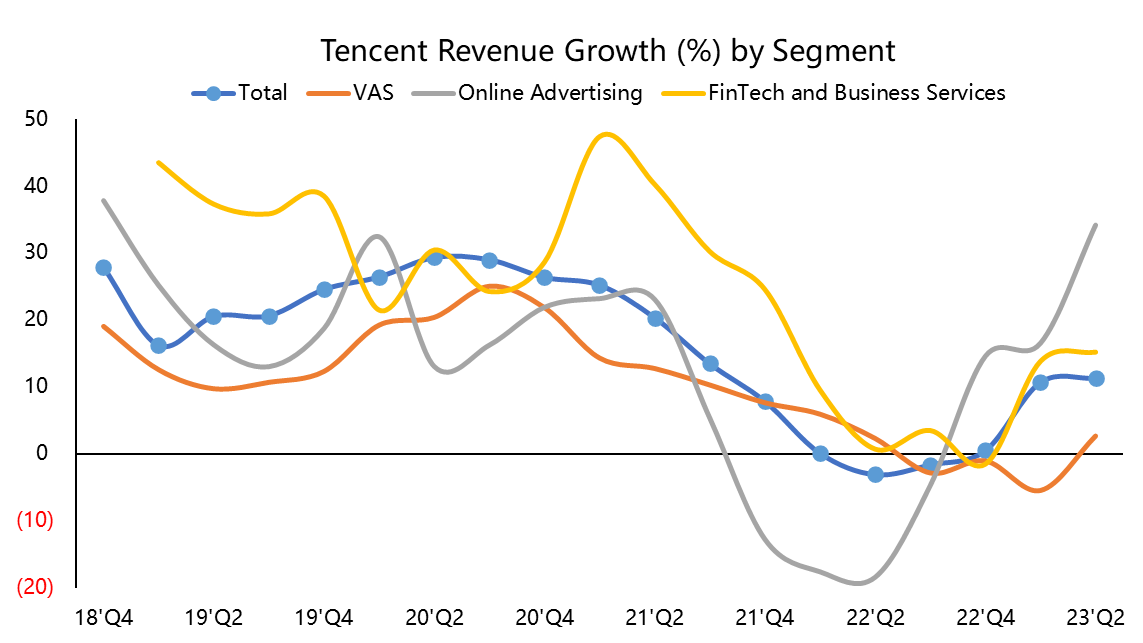

The cyclicality of the gaming business might be the source of market anxiety.

Since Q1, Tencent's gaming business has been growing at a double-digit pace, causing it to surpass expectations. Consequently, this quarter's gaming business saw a 4-5% discrepancy from market expectations, making it the greatest uncertainty in the entire financial report.

The domestic gaming landscape has remained largely unchanged. Tencent mentioned that it actively reduced the commercial content in domestic games. Coupled with the fact that users spent more time at home during the same period last year, the year-on-year performance staying flat is not as bad as it seems.

Of course, we can't deny the strong competitiveness of NetEase's "Justice" and miHoYo's "Genshin Impact." However, if this is the case, it further underscores the cyclic nature of these events.

If you don't trust Tencent, can you trust NetEase?

Overseas games like "Valorant," "Goddess of Victory: Niji" and "Triple Match: 3D" have also performed well, with a double-digit year-on-year growth. However, similar to what was observed in yesterday's Sea performance, the non-essential spending by players in Southeast Asia (a crucial overseas revenue source for Tencent) has decreased, impacting growth.

From an optimistic perspective, the outlook for Q3 is promising. Following July, according to Sensor Tower, Tencent's "Honour of Kings" reclaimed the top spot in terms of revenue. We still view this as a result of the game's "cyclical" nature. Additionally, the domestic version of "Valorant," known as "Unwavering Covenant," garnered significant attention on major game streaming platforms after its launch in July. While its PC gaming revenue may not match that of mobile gaming, it holds the potential to contribute incremental growth in Q3.

Looking at deferred revenue, this quarter has seen the highest levels for Q2. Hence, there's no need for excessive pessimism concerning the year's total gaming revenue.

Entertainment in Trasformation

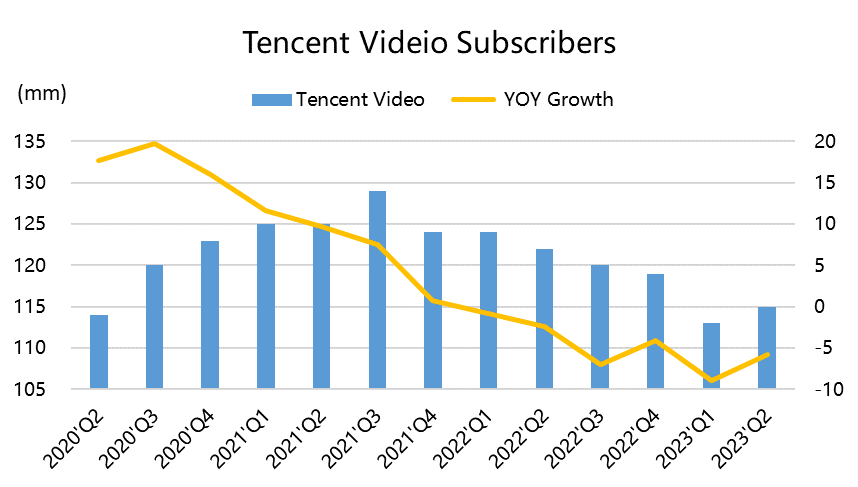

In terms of social media, the decline from a 6% growth in Q1 to 2% today, following Tencent Music's earnings disappointment yesterday, is not surprising. Entertainment streaming inherently faces challenges, and Tencent's social media focus will shift towards music, offline experiences, and casual gaming.

Tencent's video streaming service has experienced a 5% drop in paying subscribers, settling at 115 million. However, this is still an increase from the previous quarter, partly attributed to the success of the hit show "The Long Season."

Simultaneously, in Tencent Music's earnings report from yesterday, a notable decline in live streaming revenue was observed. Nevertheless, there is an accelerating trend in music subscription, and Tencent Music is placing greater emphasis on the role of digital music, shifting away from its previous emphasis on social entertainment. This is particularly significant given the current macroeconomic context, where audiovisual entertainment does not exhibit strong cyclicality.

Advertising Is the Best Performer

In Q2, the advertising business shone with a year-on-year growth of 34% and a quarter-on-quarter growth of 19%. The gross profit margin also rebounded to 48%. This growth rate and operational efficiency are both ahead of the industry average, indicating that Tencent's advertising efficiency has been upgraded and has gained recognition from advertisers.The advertising ecosystem is still in its explosive phase.

In Q2, the advertising business shone with a year-on-year growth of 34% and a quarter-on-quarter growth of 19%. The gross profit margin also rebounded to 48%. This growth rate and operational efficiency are both ahead of the industry average, indicating that Tencent's advertising efficiency has been upgraded and has gained recognition from advertisers.

There may be macroeconomic demand recovery and the booming 618 e-commerce season, but we believe that the structured increment brought by the Video Account ecosystem is more important. This includes the incremental investment from e-commerce customers and the incremental migration of live e-commerce from short video platforms to Video Accounts. The improvement of Video Accounts and product efficiency will jointly promote the continuous optimization of the gross profit margin of the advertising business.

How’s Fintech and Cloud

Commercial payment activities have grown year-on-year since Q1 due to the low base. However, the activity level of offline activities is not as high as expected, as can be seen from macro data released by the National Bureau of Statistics. Therefore, financial technology business maintains growth, but not as expected.

Cloud business competition has also become more apparent in domestic commercialization. Tencent has also increased its monetization efficiency in this area, with a gross profit margin reaching a historical high of 38%, following Alibaba Cloud's emphasis on efficiency in this business.

AI monetization still has some way to go for domestic manufacturers, but Tencent's advantage is in the technical services of Video Accounts and other related businesses. The monetization growth of cloud business will also depend on the group's ecosystem.

Is there still room for profit margin improvement?

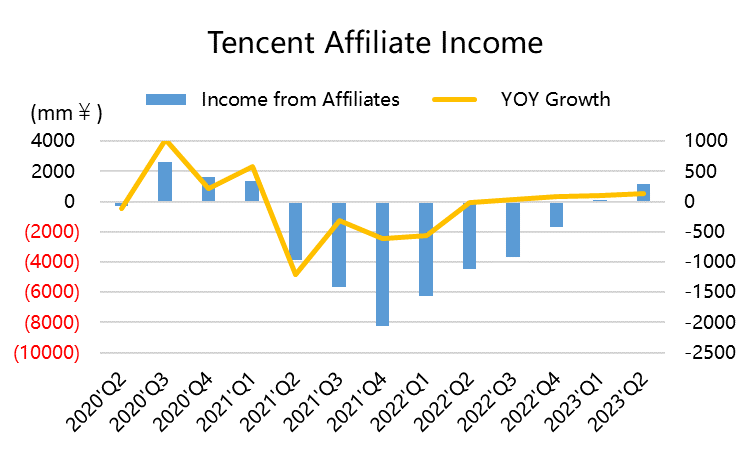

The profit of affiliate companies in Q2 was relatively high, reaching RMB 1.2 billion, compared to a loss of RMB 4.5 billion in the same period last year. This number represents the performance of associated companies in Q1, which is also the first quarter of recovery after the pandemic. Therefore, it seems that there is still room for profit growth for associated companies in the next quarter.

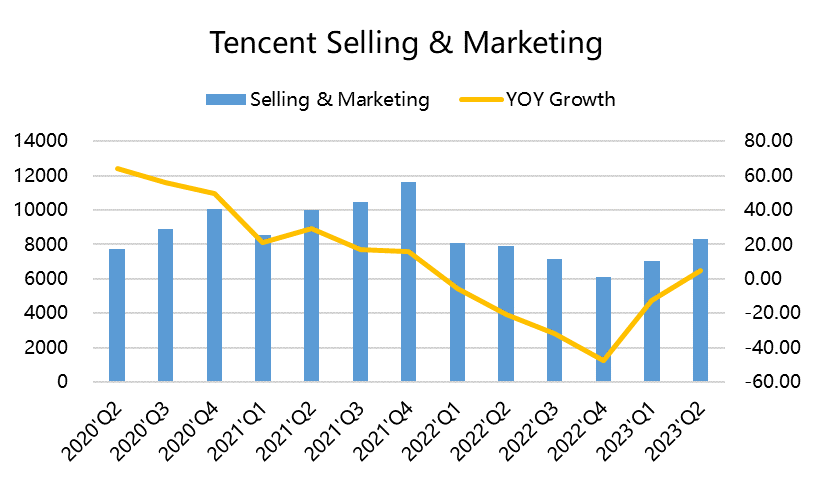

Without considering these external factors and only looking at Tencent's own operational efficiency, administrative expenses continued to decrease by 3% in Q2, but marketing expenses increased by 4.8%, and research and development expenses increased by 6.7%. It can be said that cost reduction and efficiency enhancement have been achieved.

Interest expenses are also critical in the era of high interest rates, so Tencent's interest expenses and interest income have both increased. Q2's net interest was RMB 128 million, which is a reasonable asset allocation.

Adjusted EBITDA was RMB 56.8 billion, far exceeding the expected RMB 51.5 billion, and the profit margin also increased from 33% last year to 38%. Profit growth exceeded revenue growth and can bring stronger cash flow to the company.

Valuation

Currently, Tencent's trailing P/E ratio for the past 12 months is 14.7 times, far below the average level of the past 10 years; EV/EBITDA is even less than 10 times, and it has been said that it is undervalued for a long time. But why doesn't the market give face?

The selling by major shareholders may still be an important reason. Especially during the quiet period, Tencent's share buyback stopped, leaving only determined major shareholders to reduce their holdings, putting great pressure on the market.

The discount between $Prosus NV(PROSY)$ stock price and net assets is about 36%, and it has not narrowed due to share reduction.

Based on the current reaction of foreign capital, Tencent may face an unfavorable Thursday (with a possible correction range of 3-5%), but starting from Friday, it can continue to buy back in the secondary market to offset the impact of selling to some extent. Whether Tencent can make it or not has become synonymous with whether Hang Seng Technology can make it or not.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Tencent is huge - it’s like a venture capital / investment fund. i’m seeing it has some sell pressure as it’s main shareholder has indicated many times they will offload the shares.

Dopo Alibaba sempre utile tenere d'occhio i risultati dell'altro gigante cinese della tecnologia: Tencent.

TCEHY , jd and tencent positive earning outcomes can send this over 95 . Let’s go , rooting for you.

11% revenue growth, profits even better, buyback and dividends what's not to like?

I guess it would be like a Tencent mutual fund. I'm invested in Chinese stocks