What if Kuaishou is trading at 11x EV/EBITDA?

$KUAISHOU-W(01024)$ released 2023 Q2 earningreport.

Following the comprehensive profitability achieved in the Q1Kuaishou's Q2 results further bolstered overall recovery expectations and achieved a historically high profit margin.

Due to the previously disclosed earnings expectations and the market's partial pricing of these, it is anticipated that the long-term profit margin has yet to peak, leaving room for valuation to rise.

We believe,

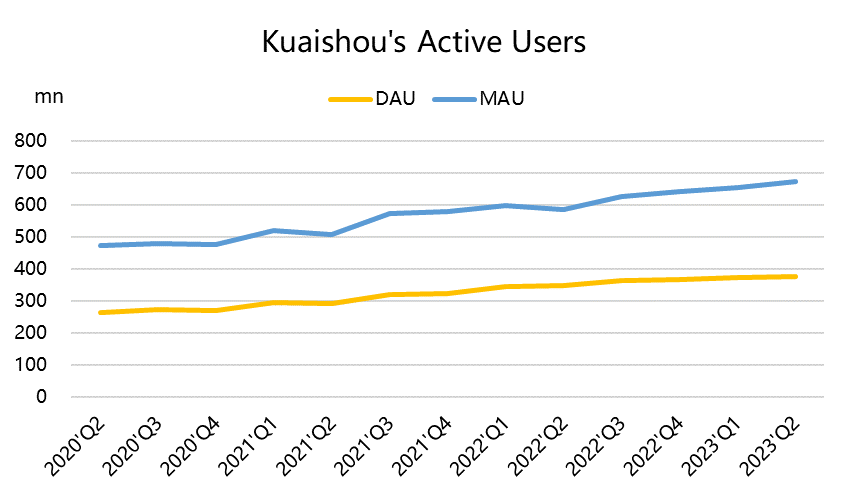

The sustained growth of active users is more pleasantly surprising than the income-profit aspect. Based on this trend, it is projected that MAUs could reach 700 million by the end of this year, with DAUs potentially hitting 400 million. This growth trajectory contributes significantly to the three major business segments.

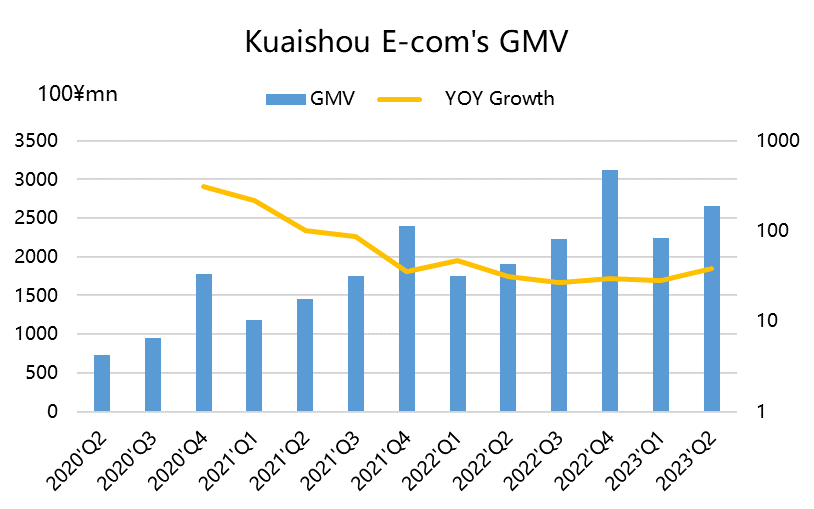

The GMV of live-streaming e-commerce maintains a notable growth rate and remains one of the few companies in the industry to disclose GMV figures. Other revenue sources, including e-commerce, are the primary drivers of growth for the upcoming quarters.

A substantial portion of the advertising business relies on internal flows from e-commerce and short videos. Consequently, this quarter witnessed an uptick in GMV growth to 39%, alongside an advertising revenue recovery to 28%. Unlike the previous quarter, the rebound of the offline economy also brought about additional advertising volume outside the ecosystem.

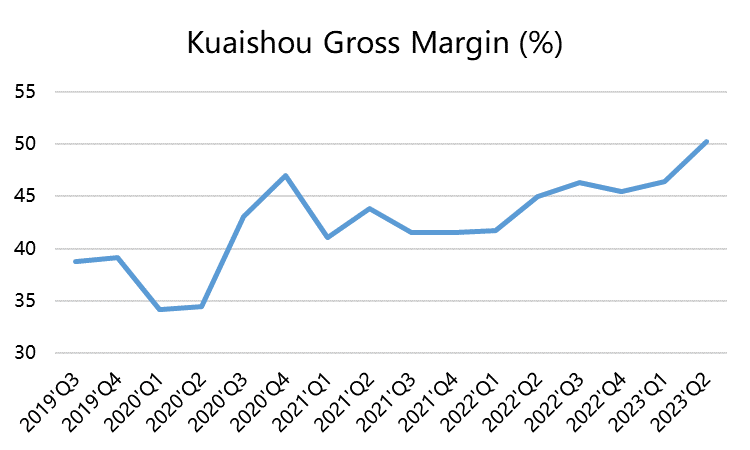

The expansion of the high-profit-margin advertising segment also elevated the company's gross profit margin to a historic high. Simultaneously, ongoing cost reduction efforts contributed to achieving historic highs in operating profit and adjusted EBITDA. It is estimated that there is still potential for long-term growth in operating profits.

However, the current stock price is influenced by a crucial factor.

Performance Review

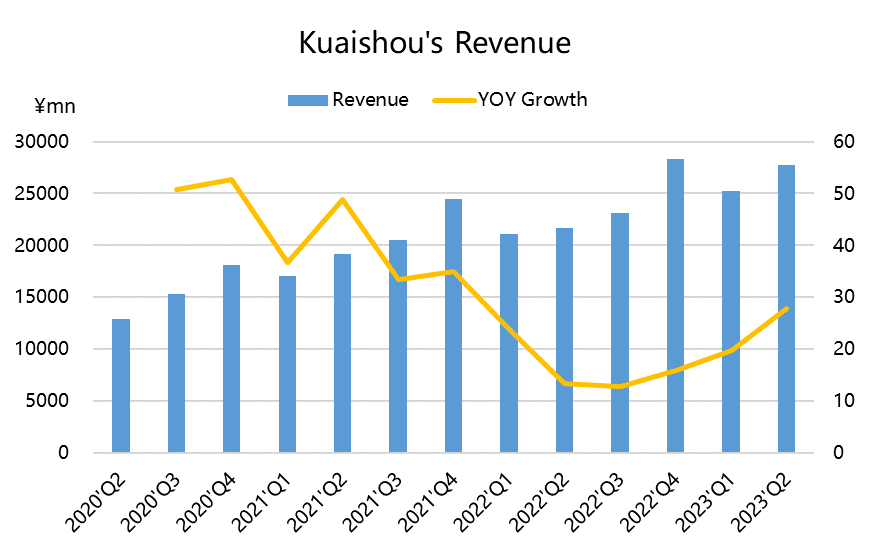

Revenue

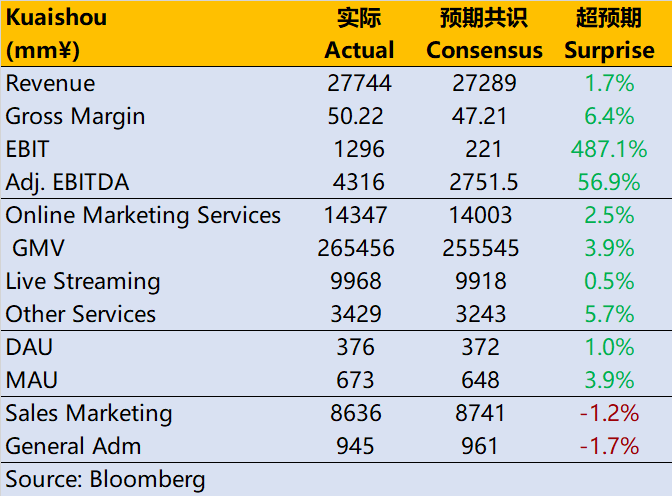

Overall revenue reached 27.74 billion yuan, surpassing market expectations of 27.29 billion yuan, with a year-on-year growth of 28%, maintaining an upward trajectory in growth rate.

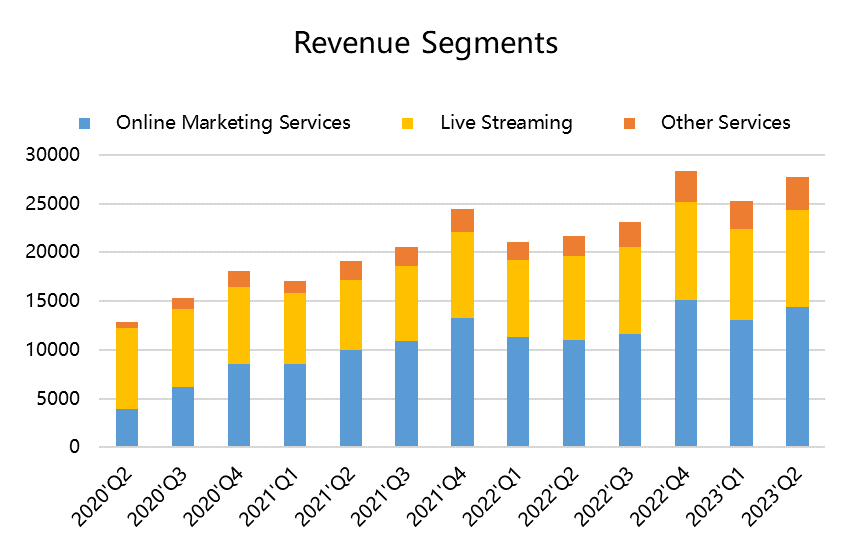

Among these, revenue from network marketing services stood at 14.35 billion yuan, marking a 30% increase compared to the previous year, exceeding market expectations of 14 billion yuan;

Live streaming business revenue reached 9.96 billion yuan, with a year-on-year growth of 16%, surpassing market expectations of 9.92 billion yuan;

Revenue from other business sectors amounted to 3.42 billion yuan, experiencing a year-on-year growth of 61%, exceeding market expectations of 3.24 billion yuan.

From a geographical perspective, domestic business revenue reached 27.3 billion yuan, representing a 26% year-on-year increase, while overseas business revenue amounted to 4.47 billion yuan, soaring by 334% compared to the previous year.

Profit

Gross profit margin achieved 50.22%, surpassing market expectations of 47.21%,

Operating profit reached 1.296 billion yuan, surpassing market expectations of 2.21 billion yuan;

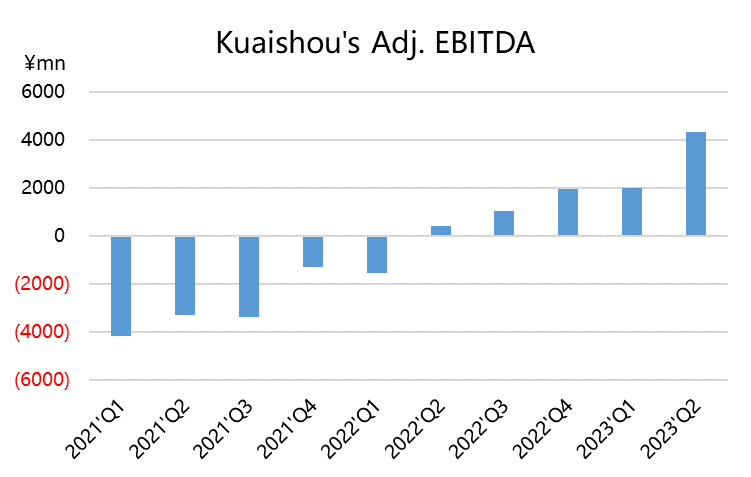

Adjusted EBITDA amounted to 4.32 billion yuan, significantly surpassing the anticipated 2.75 billion yuan.

Investment Highlights

Continued Surge in Active Users, with High Growth Potential

The momentum of user engagement for Kuaishou remains strong, as its traffic continues to expand steadily. The overall monthly active users (MAU), including contributions from overseas operations, surged to 673 million, surpassing the projected 648 million, and daily active users (DAU) also rose to 376 million, exceeding the projected 372 million.

This year, offline activities have gained momentum along with the recovery, and the slightly lower growth rate of DAU compared to MAU is understandable. In general, the DAU/MAU ratio remains at a high level of 55%, ranking among the top apps in terms of user stickiness.

On the whole, whether it's providing support to creators' traffic or establishing its own ecosystem within the realms of local life, advertising, and other lucrative domains, it's often the most effective strategy for drawing in users. Therefore, Kuaishou has been able to steadily expand its user base without significantly increasing costs.

Live-streaming e-commerce serves as the primary catalyst.

Although the consumption environment in Q2 might not have been ideal, trends can be gleaned from the financial reports of Alibaba and JD, indicating that the prosperity of online consumption far surpasses offline.

In Q2, Kuaishou's e-commerce GMV reached 265.6 billion yuan, a year-on-year growth of 39%, marking an even higher growth rate. Aside from the strategy of commission-sharing with fast-selling distributor anchors introduced in Q1, the relatively low base of last year's Q2 also contributed to this growth. The overall revenue growth, including e-commerce, exceeded 60%, serving as the main driving force.

E-commerce has further transformed Kuaishou's revenue structure, shifting from heavily entertainment-focused live-streaming income to a growing emphasis on e-commerce.

Q2 is indeed the peak shopping season, and live-streaming e-commerce remains the most significant trend in online consumption. Therefore, even during periods of intense competition in the e-commerce sector, short video live-streaming e-commerce maintains a competitive advantage in terms of cost-effectiveness and user traffic compared to traditional e-commerce platforms. With the current pace, if Q4's shopping season performs well, Kuaishou has a high chance of achieving its 1.2 trillion yuan GMV target for this year.

Recovery in the advertising market as a whole.

Q2's network marketing revenue grew by 30% year-on-year, doubling the growth rate of Q1, reaching 14.3 billion yuan. The revenue trajectory of Kuaishou's advertising business aligns with that of e-commerce, indicating a strong reliance on the consumer market for advertising revenue.

The incremental growth of Q1 primarily stemmed from internal traffic. Thus, despite a 28% increase in GMV, the advertising business growth rate stood at a mere 15%. However, there was an improvement in this situation in Q2, indicating that incremental growth beyond live streaming e-commerce has begun. Previously, Tencent Holdings (00700) financial reports also highlighted the enhancement of the overall advertising business by the app ecosystem.

Innovation remains essential for the live streaming sector.

Purely entertainment-based live streaming has reached a saturation point, with platforms like Huya and Douyu experiencing multiple consecutive quarters of decline. In addition to absorbing traffic from smaller platforms, Kwai's entertainment-focused live streaming has restructured the industry. Similar to Douyin, it has expanded its scope to industries like recruitment, establishing new categories of live streaming such as "Kwai Recruitment" and "Ideal Home."

The differentiation in traffic also sustains double-digit revenue growth for the company's live streaming segment, with Q2 growth at 19%, an improvement from Q1.

Profit margins still hold potential for growth.

With the recovery of the higher-margin advertising business, an increase in the revenue-sharing ratio from live streaming e-commerce, and the continuation of cost-saving measures, Kwai achieved historically high profit margins in Q2.

Notably, the gross profit margin exceeded 50%, reaching 50.2%, while the adjusted EBITDA reached 4.32 billion yuan, resulting in a profit margin of 15.6%.

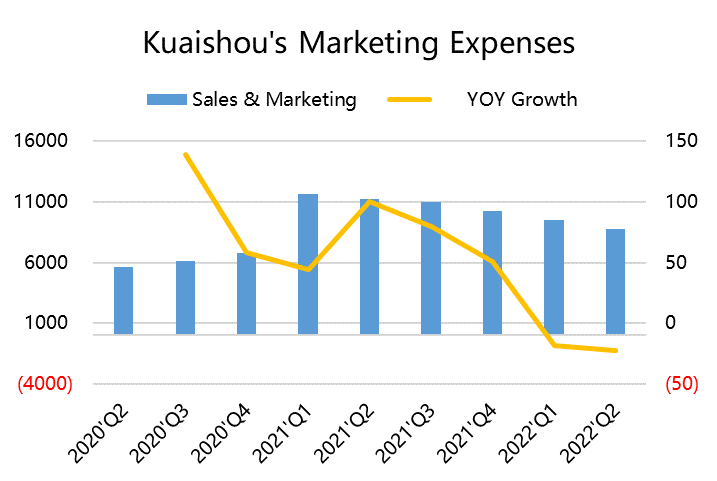

On the front of operational expenses, Q2 witnessed a further 1.1% reduction in administrative costs, a 1.4% decrease in marketing expenses, and a 3.9% decrease in research and development costs. These cost reductions continue, though the pace is also nearing its conclusion.

Valuation and Stock Price

If we estimate the profits for 2024 using the Q2 EBITDA profit margin and maintain the consistent expected 131.2 billion yuan (expected to be revised upward later), with the current EV of 256.8 billion Hong Kong dollars,

EV/EBITDA ratio could stand at 11.5 times.

This valuation level might have caught many off guard in terms of how swiftly it materialized for Kuaishou.

Given the substantial volatility of the $HSTECH(HSTECH)$ as a whole, coupled with various factors influencing capital decisions, and considering that Hong Kong stock pricing leans towards international investors, Kuaishou's current undervaluation is not unexpected.

Of course, Kuaishou's investors might have numerous grievances as well, such as debuting in 2021 during the internet frenzy at a high price of 400 Hong Kong dollars, which trapped a significant number of shareholders.

To instill investor confidence, apart from relying on performance, additional efforts are essential. Certainly, in the case of internet companies with substantial equity incentives, these incentives should either be factored into performance or into stock prices. Therefore, whether including equity incentive expenses in financial reports (reverting to losses) or factoring them into stock prices (lowering the valuation level), neither is currently a significant reason for investors to substantially increase their holdings.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Despite some changes in the environment, it remains one of the most competitive companies in China. Looking at the long term, the outlook is still positive. My strategy remains unchanged – to hold firm during rises and not to sell on declines.

Currently, those with no positions are bearish, while those with positions are bullish. Let's wait and see.

It hasn't reached my target price for adding more positions yet, please don't rise further.

The pullback level has been reached, I'll add some positions first.

Recently, stocks have been falling after the release of financial reports!