Why Grab's Still Losing Three Years?

GRAB has performed well, but its valuation remains high.

Following the release of its financial report on Wednesday, $Grab Holdings(GRAB)$ saw an increase of over 10% in its stock price. It has also been one of the stocks that has shown resilience this year, but struggled to make significant gains. Since the beginning of the year, its returns have lagged behind the S&P 500 (.SPX), with higher volatility.

However, since March 2022, Grab's stock price has been fluctuating between $2 and $4, and regardless of its performance, it has been unable to break free from this range, let alone surpass the $10 mark it had during its SPAC issuance. The primary reason for this seems to be the persistently high valuation of the company.

Q2 performance reveals a gradually optimistic outlook

The total Gross Merchandise Volume (GMV) reached $5.24 billion, surpassing Q1's $4.96 billion, showing a 3.72% increase and exceeding the market's expected $5.12 billion.

The number of monthly paying users increased to 34.9 million, higher than the 32.6 million in the same period last year and the 33.3 million in Q1, also surpassing the market's expected 33.6 million.

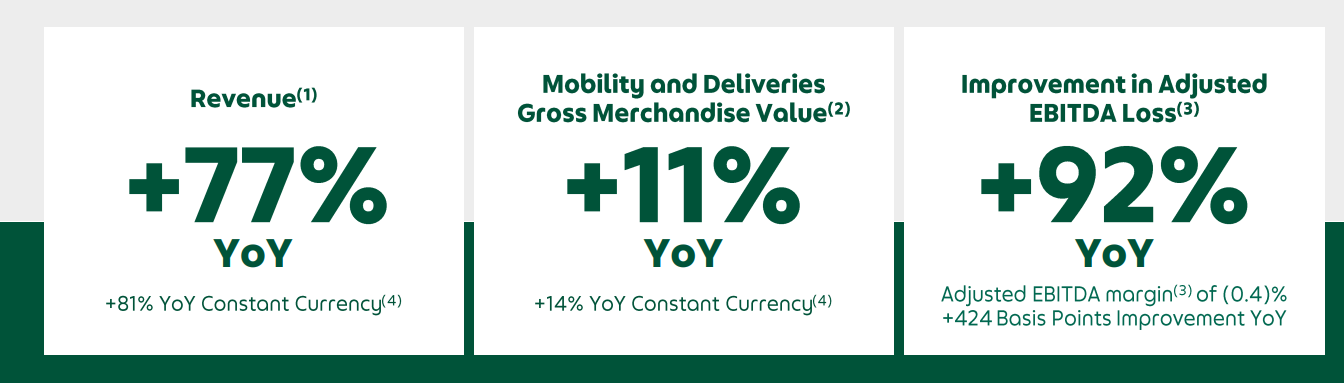

The revenue reached $567 million, a staggering 76.6% increase compared to the previous year, surpassing the expected $546 million and Q1's $525 million.

Adjusted EBITDA improved from -$66 million in Q1 to -$20 million, significantly better than the -$233 million in the same period last year and far beyond the expected -$64.58 million by the market.

Additionally, the company stated its intention to achieve EBITDA breakeven on an adjusted basis a quarter ahead of the initial plan, implying EBITDA profitability in Q3.

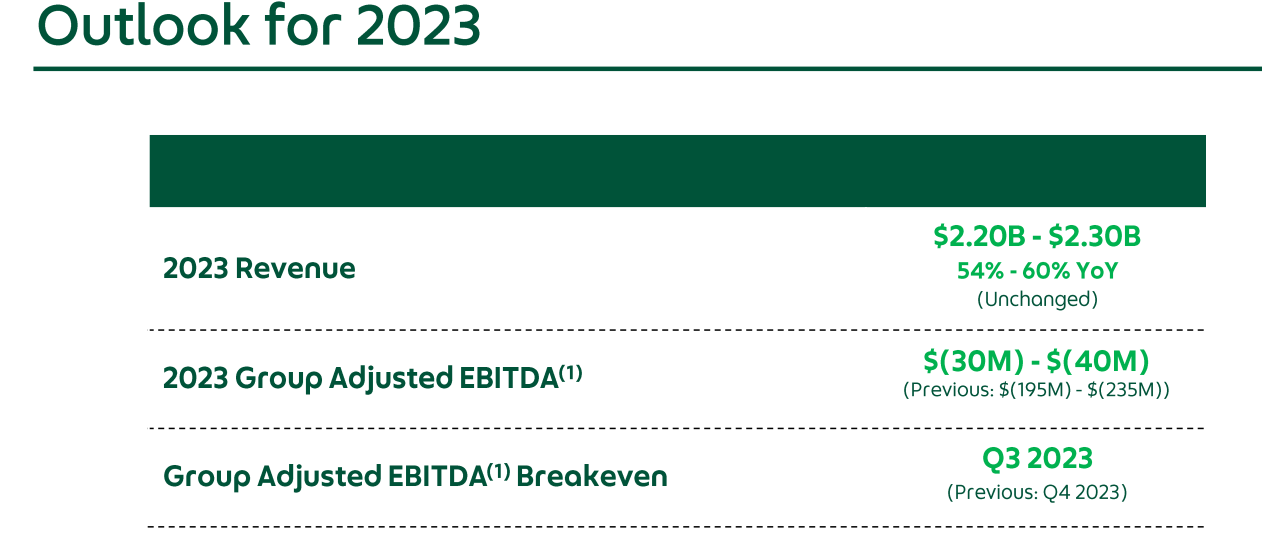

The guidance for the full year 2023 has also been raised. Adjusted EBITDA is projected to be between -$30 million and -$40 million, higher than the previous estimate of -$195 million to -$235 million. Revenue outlook is set at $220 million to $230 million.

In summary, various business segments have demonstrated robust growth, the food delivery business has returned to positive EBITDA, and the optimized incentives have maintained the engagement of existing operators and drivers. Certain changes in delivery product models, such as the expansion of GrabUnlimited subscribers, have yielded favorable results.

Why is the stock price struggling to rise?

Just like Uber, Grab has actually established a significant advantage with economies of scale in its region, and given the current market environment, it's difficult for other players to replicate this without setbacks. Therefore, similar to Uber, Grab's performance has noticeably improved this year.

However, Grab's original sin lies in its SPAC, and the choice of a highly popular and large-scale SPAC that year implies that post-IPO investors might have to endure a "lost valuation."

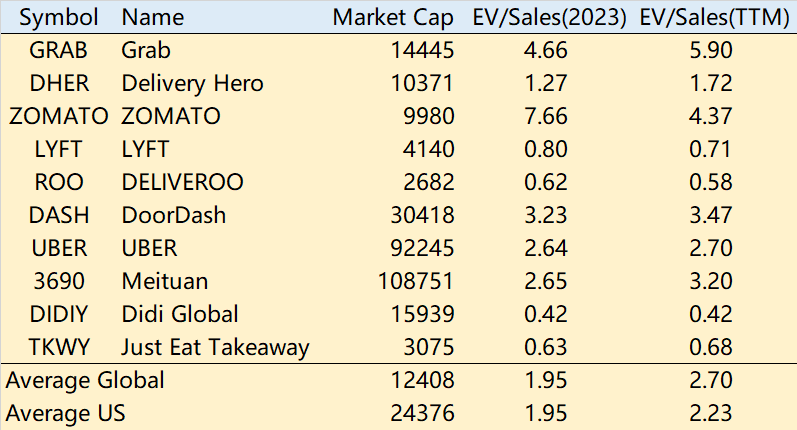

Due to substantial profit deviations, even when comparing based solely on revenue multiples, the industry's current average EV/Sales ratio is 2.6. If only considering U.S. market-listed companies, the average is merely 2.2. In contrast, Grab aims for 5.9.

Even when looking at the full-year expectations, Grab's 5.4 is significantly higher than the average of 1.95. At this pace, Grab must sustain industry-average double growth rates for three consecutive years to possibly match the industry average level three years from now.

It's aptly put that the "lost three years" brought about by the SPAC.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

GRAB traded at $3.755 after earnings, and the Calls went up from $0.45 (when I wrote this article) to $0.80 at the close , for about 80% gain!

Holdings prior to the earnings report this week,

I would consider purchasing the 3usd strike price in the money calls .

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

nice. This is the start of the turnaround. Move guidance of positive earnings to Q3 2023 from Q4 2023. Overall green and will likely ad after Jackson Hole conference.