Why Temu becomes Sooooo Important to PDD?

$Pinduoduo Inc.(PDD)$ released its Q2 earningl report before opening August 29th. Following the resurgence seen in its Q1 , Pinduoduo continues to ride this wave of recovery, surpassing expectations once again on both revenue and profit fronts, re-entering a phase of high-speed growth.

As we've previously highlighted multiple times, being one of the only two components of the $NASDAQ 100(NDX)$ (the other being $JD.com(JD)$ , Pinduoduo's performance in the secondary market has not only captured the attention of domestic investors but also mirrors the overall sentiment of international investors towards Chinese concept stocks. The previous underselling, the subsequent resurgence, and the double-digit pre-market surge all paint a vivid picture.

In the wake of Alibaba and JD.com's better-than-expected financial reports for the Q2 reporting season, Pinduoduo once again asserts to investors that the online consumer environment isn't as bleak as perceived. Its robust growth further enhances its valuation, bolstering future expectations. However, uncertainties still linger on the path to realization.

We believe

Both advertising and commission revenue have surpassed expectations, showcasing the strength of the platform's ecosystem. This is undoubtedly a reflection of heightened engagement among online merchants and intense competition. It signifies that the overall consumer landscape is not as pessimistic as previously thought.

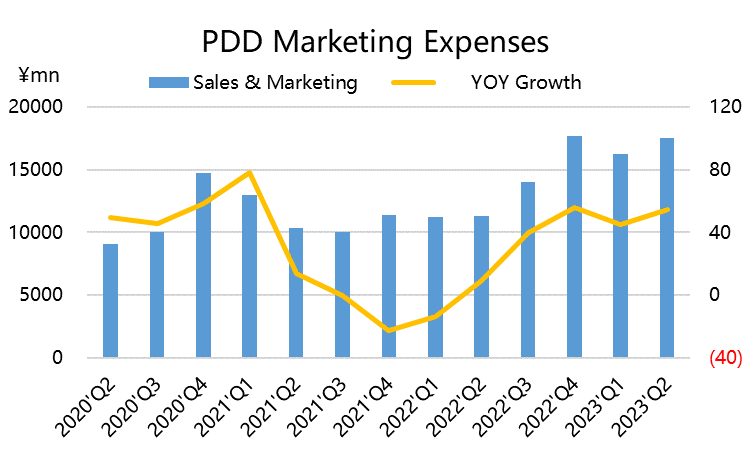

Marketing expenditures continue to rise, with a decrease in gross profit margin. This indicates that Temu, the overseas growth engine, has begun to gain traction, but it also comes with increased marketing costs. This might impact profit margins in the coming quarters.

Profit margins have improved through cost reduction and efficiency enhancement. The company's operational efficiency has further improved. Yet, the competition among e-commerce platforms remains fierce. While there's no imminent significant threat, ongoing efforts are required.

In terms of valuation, the company's long-term profit margin is expected to remain above 30%. However, the maturity of Temu's overseas operations is pivotal, whether it can replicate the China business becomes crucial for profit margins and valuation stability.

Considering this growth trajectory, based on the profit multiple in 2025, the current valuation is still not considered overvalued.

Earnings Review

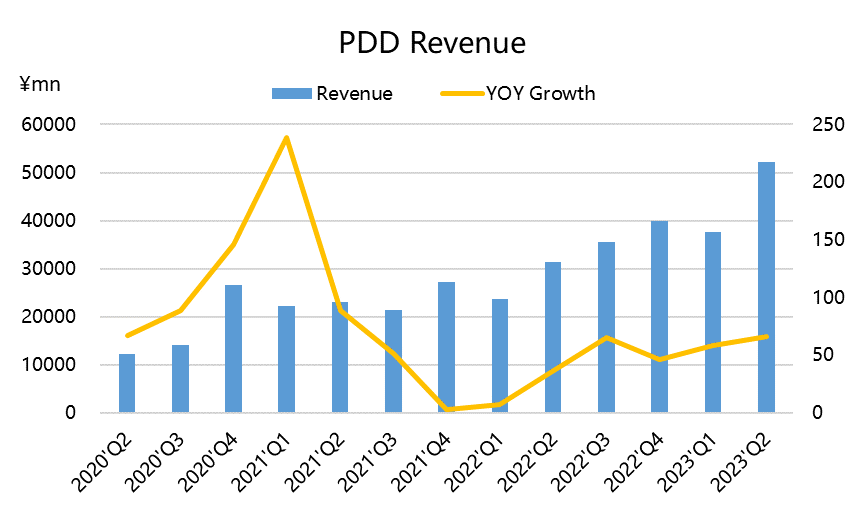

Revenue

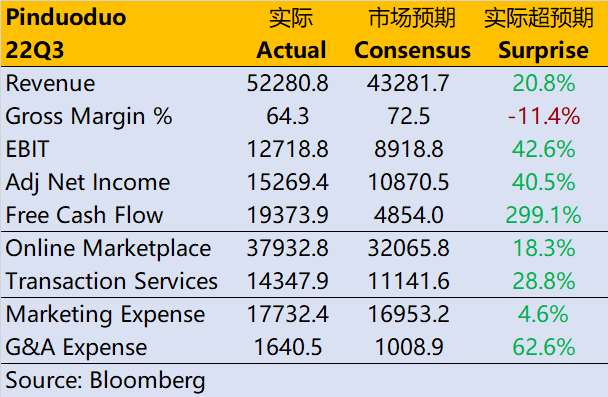

Total revenue reached 52.28 billion yuan, marking a year-on-year growth of 66.3%, surpassing market expectations by over 20% compared to the anticipated 43.3 billion yuan;

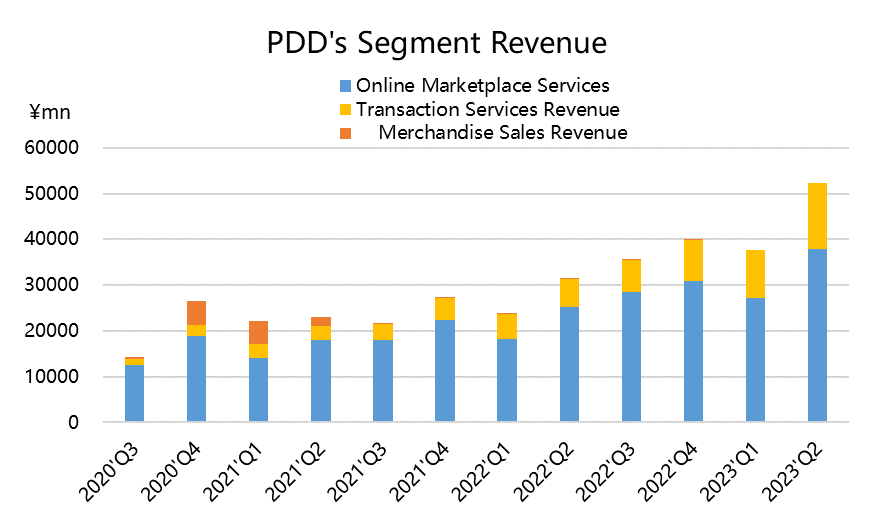

Among them, online marketing service revenue amounted to 37.93 billion yuan, showing a year-on-year growth of 50%, exceeding the consensus forecast of 32.1 billion yuan, and also surpassing the previous quarter's YoY growth rate of 38%;

Transaction service revenue reached 14.35 billion yuan, experiencing a year-on-year growth of 131%, exceeding market expectations of 8.31 billion yuan, as well as the previous quarter's growth rate of 86%;

Profit

COGS reached 18.7 billion yuan, demonstrating a year-on-year growth of 37%, exceeding the market's expected 11.7 billion yuan;

Marketing expenses were 17.5 billion yuan, reflecting a year-on-year growth of 55%, surpassing the market's projected 16.3 billion yuan;

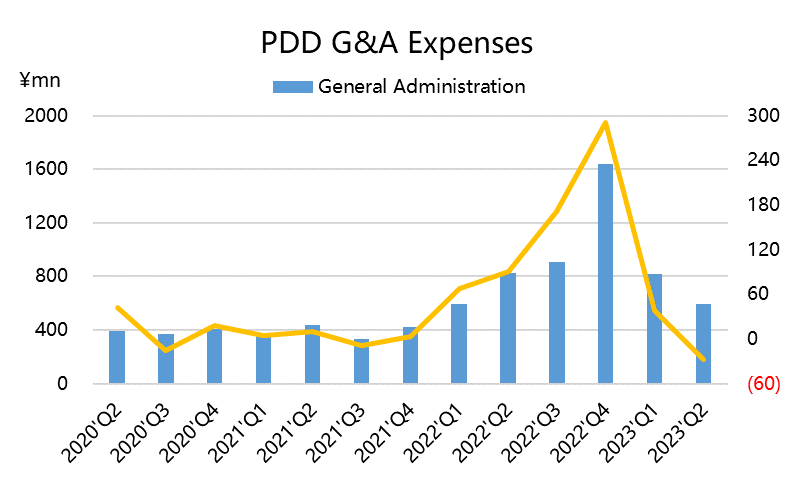

Administrative expenses totaled 600 million yuan, indicating a decrease of 28% year-on-year;

Research and development expenses stood at 2.7 billion yuan, with a year-on-year growth of 5%.

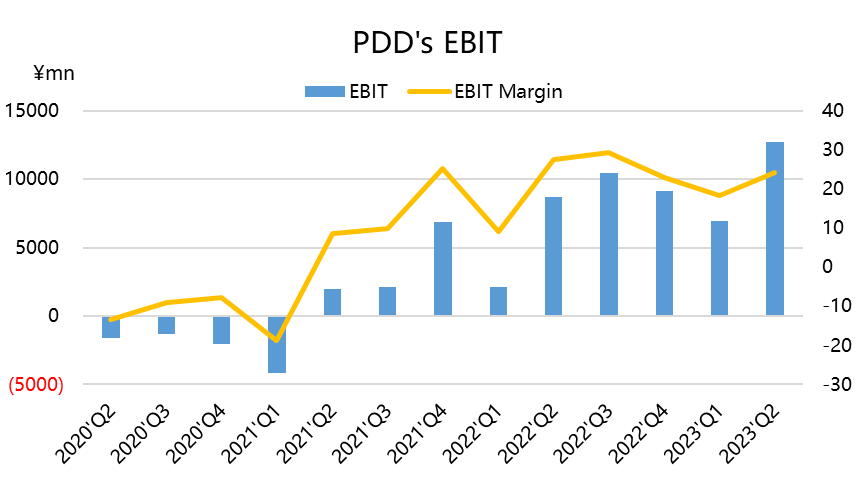

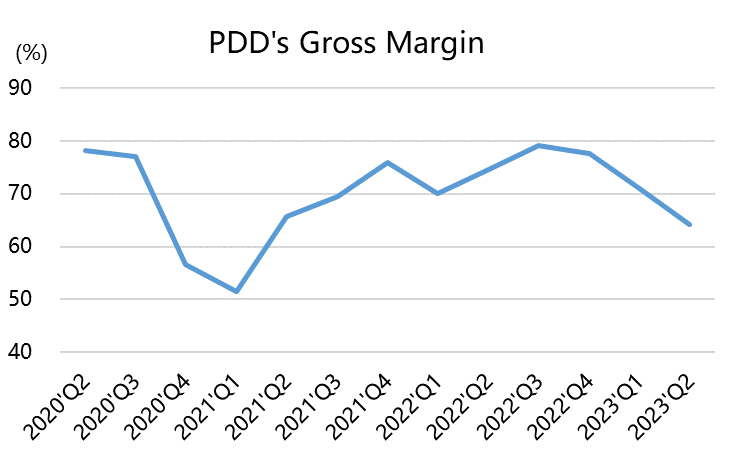

As a result, the gross profit margin decreased to 64.25%, lower than the 74.68% from the same period last year, as well as the anticipated 72.53%;

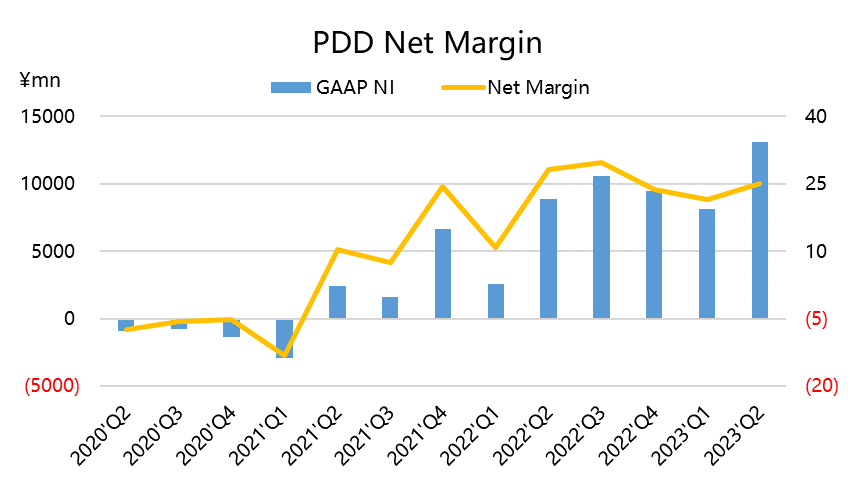

Operating profit reached 12.72 billion yuan, witnessing a year-on-year growth of 46%, significantly surpassing the market's expected 8.9 billion yuan;

Net profit attributable to ordinary shareholders amounted to 13.1 billion yuan, reflecting a year-on-year growth of 47%.

Investment Highlights

Expectations were not modest, yet the results remain pleasantly surprising

Regarding revenue, due to the rebound in performance from the previous quarter, market expectations for Pinduoduo's Q2 performance continued to rise. However, for multiple reasons, this was not fully reflected in the stock price.

The market's projection for Q1 revenue growth at Pinduoduo was a conservative 38%. Comparatively speaking, this growth rate, when compared with JD.com and Alibaba, wasn't overly conservative. Yet, the reality is that the growth rate reached 66%, with revenue leaping from just over 30 billion to over 50 billion yuan. This truly exceeded expectations.

1. The low base from the previous year played a role;

2. Substantial contributions from overseas business "Temu";

3. There are groups both domestically and internationally that are simultaneously "overlooked," encompassing the demand for cost-effectiveness and the potential need for "downgraded" consumption.

Regarding overseas dynamics, the rapid growth can't be dissociated from the prevailing inflationary environment. Part of the middle-class and above has witnessed an increase in wealth along with high interest rates, while the lower-income groups have had to endure higher commodity prices and have even begun engaging in "zero-cost shopping" offline. In this context, online platforms with a low-cost model like Pinduoduo are particularly suited for their needs.

Simultaneously, we can observe the recovery of the advertising sector at a 50% growth rate, and the online competition is gradually intensifying, making it more challenging for merchants to generate profits on Pinduoduo's platform. However, commission income has doubled, which could possibly be an unexpected outcome of the overseas expansion.

Gross margins declines, but net margins gains

Last quarter's gross profit margin fell short of expectations, but it still remained above 70%. However, this quarter, it dropped directly to 64%. Despite the recovery in the advertising sector and the overall stability of the domestic platform, the incremental effect of overseas expansion becomes evident.

Thankfully, the overall strategy continues to focus on cost reduction and efficiency enhancement. Research and development expenses have increased by single-digit percentages, administrative costs have decreased, and even though marketing expenses grew overseas, the 55% growth rate is still lower than the 66% growth rate of income.

As a result, the pre-tax profit margin ultimately maintains at 31%, which is considered quite favorable for an e-commerce business. However, sustaining such profit margins cannot rely solely on cost reduction. It's even more crucial to swiftly enhance the efficiency of the Temu business; otherwise, the profit margin might decrease over the next few quarters.

Valuation

This year, Pinduoduo's stock price has indeed experienced a roller-coaster ride following changes in its performance. The stock price went from over 100 in January to under 60 in May, and hovered around 82 before the financial report.

For e-commerce, the most direct method of valuation is through profit indicators.

We believe that a portion of overseas business, such as Temu, should be calculated separately from the domestic business. However, since the company has not yet differentiated between the two operations, it is currently difficult to ascertain the uncertainty brought about by the overseas business. Additionally, a significant portion is allocated to employee compensation, which could eventually be realized in the secondary market. Therefore, when considering profit multiples, it remains reasonable to calculate based on the current overall profits.

If we consider a target profit margin of 25%, the pre-market price of $92 corresponds to forward price-to-earnings ratios of 21.2x, 15.7x, and 12.8x for the years 2023, 2024, and 2025 respectively.

These ratios are lower than the current industry average and also lower than the anticipated values of Alibaba and JD.com.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Great ariticle, would you like to share it?

Great ariticle, would you like to share it?

Good insights to popular pinduoduo stock.