Not only NVDA to bet, Salesforce got another surge on its Q2 earnings!

$Salesforce.com(CRM)$ announced its fiscal Q2 2024 earnings ending on July 31 after close August 30th. Both top line and bottom line beat, leading to a 6% surge in after hours.

In fact, CRM has already surged 60% this year. It stands out as one of the top-performing components of the $S&P 500(.SPX)$ , $NASDAQ(.IXIC)$ and $DJIA(.DJI)$ . This remarkable ascent is attributed to both exceptional performance and the high expectations placed on it in the AI era.

We believe

The continuous strong performance attests that the macroeconomic landscape might not be as pessimistic as previously thought. It also showcases the company's competitive strength within the industry.

The positive impact of price hikes has not been offset by price-sensitive customers; on the contrary, large corporations continue to demonstrate loyalty.

Profit margins have consistently surged since the involvement of fund investor Elliot, highlighting the effectiveness of restructuring efforts in cost reduction and efficiency improvement.

The integration of AI-driven office suites is expected to further enhance the company's product ecosystem and elevate future cash flow levels.

While the current high GAAP PE ratio might not accurately depict the situation, considering EBITDA multiples is more appropriate for valuation. Both the trailing twelve months (TTM) and the 2024 estimated valuations are below industry averages, indicating potential for further growth.

Earnings Review

Review

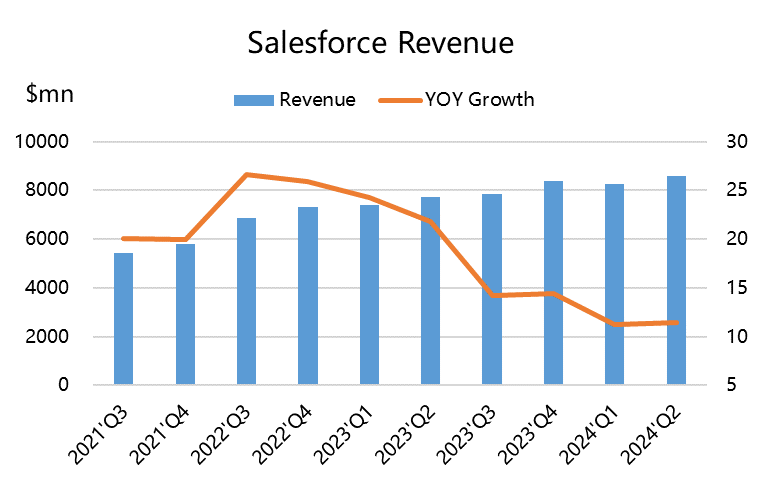

- Revenue reached $8.6 billion, surpassing the expected $8.52 billion, with an 11% YoY growth.

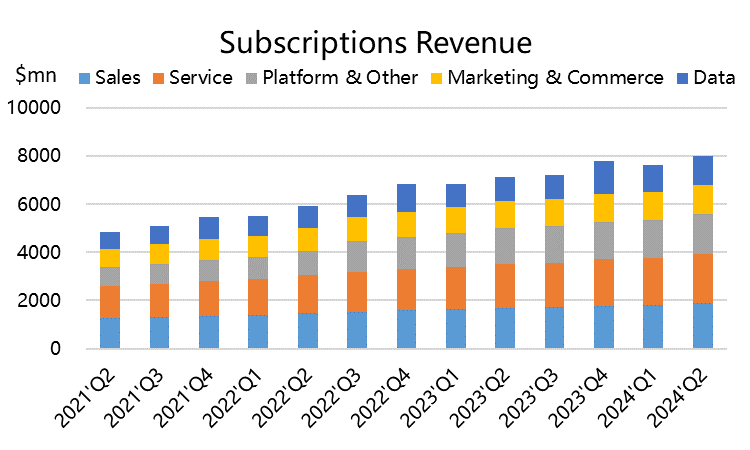

- Subscription and support revenue amounted to $8.01 billion, surpassing the expected $7.91 billion, with a 12% YoY growth.

- Professional services and other revenue totaled $600 million, growing by 3%.

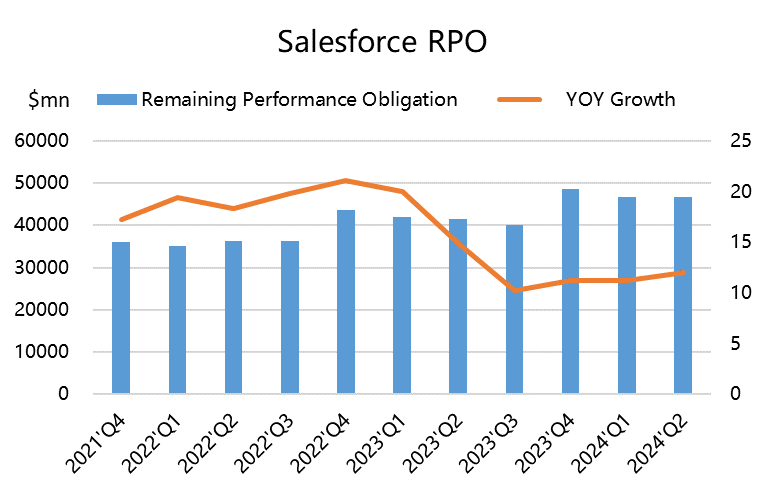

-Remaining performance obligations stood at $46.6 billion, exceeding the expected $46.2 billion. Current remaining performance obligations reached $24.1 billion, higher than the market expectation of $22.1 billion, showing a 12% YoY increase.

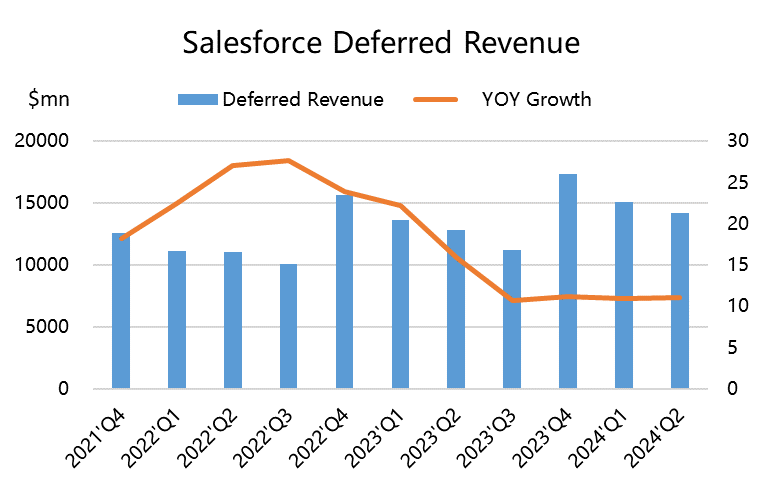

-Deferred revenue was $14.23 billion, growing in parallel with revenue, maintaining an 11% YoY growth, and aligning with the expected $14.47 billion.

Profit

- Gross margin was 79.0%, exceeding the anticipated 78.0%.

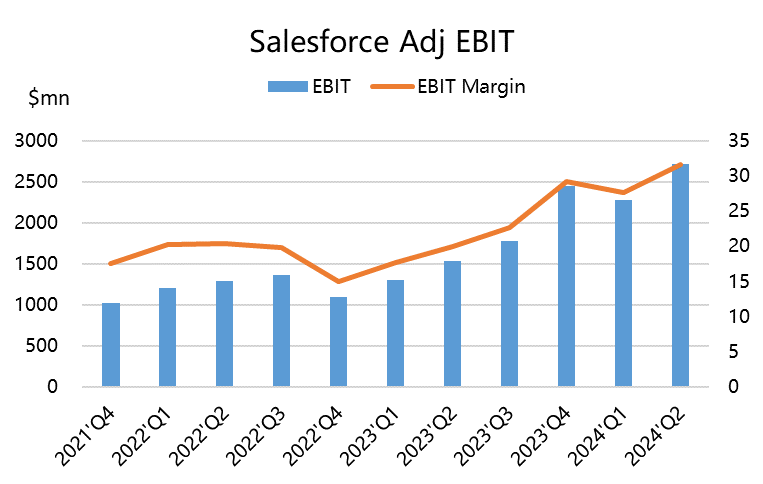

- GAAP operating margin was 17.2%, while non-GAAP operating margin reached 31.6%. Restructuring adversely affected GAAP operating margin by 50 basis points.

- GAAP diluted EPS was $1.28, and non-GAAP diluted EPS was $2.12, both surpassing the market's expected $1.9.

- Additionally, $1.9 billion worth of stock was repurchased in Q2.

Guidance:

- The company anticipates Q3 2024 revenue to range from $8.7 billion to $8.72 billion, exceeding the previous expectation of $8.65 billion, representing around 11% YoY growth.

- FY24 full-year revenue is now projected to be between $34.7 billion and $34.8 billion, with non-GAAP operating margin guidance raised to about 30.0%.

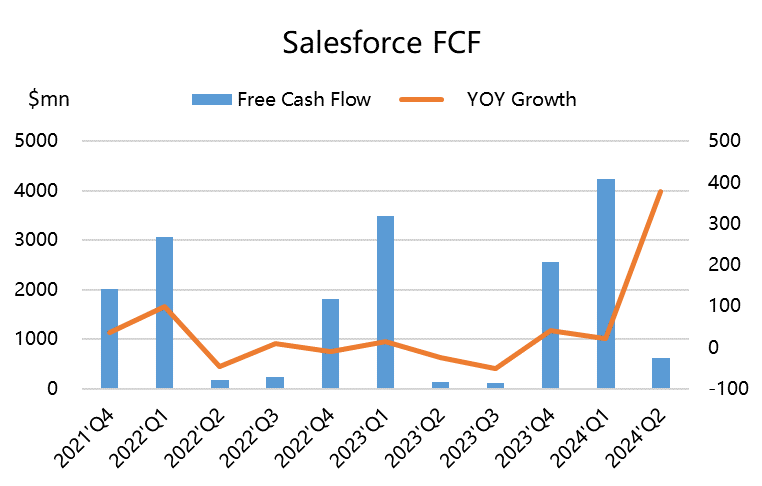

- The growth in operating cash flow guidance has been increased to a 22% to 23% YoY increase.

Investment Highlights

After surpassing expectations in the first two quarters, the market has indeed raised its performance expectations for Salesforce. This year, due to the lingering "recession expectations," there was a sense of conservatism prevailing for a while.

However, the fact that CRM has exceeded expectations even when expectations were already quite high demonstrates the company's competitive strength in the industry and its exceptional operational capabilities.

Among several leading indicators, cRPO continues to exceed expectations, while deferred revenue remains relatively steady compared to expectations. Both indicators maintain a double-digit year-on-year growth rate of around 11%, indicating that the growth of orders remains relatively stable. However, cRPO will continue to be significantly impacted by the accumulated effects of sales performance over the past five quarters.

Furthermore, despite the price increase implemented this quarter, customer stickiness has not decreased as a result. In reality, most major companies have been able to accept these changes, which will greatly assist the company's profit margins in the coming quarters.

In terms of guidance, the company adopted a more conservative approach in the first half of the year, factoring in certain recession expectations and thereby placing a greater focus on profitability. However, it now appears that the recession might not truly materialize, suggesting that the upward revision of guidance may not have yet reached the company's full potential.

The management's heightened focus on profitability is a new development following the entrance of the proactive investor Elliot. We observe that the company's profit margins and free cash flow for two quarters have significantly exceeded market expectations. The adjusted operating profit margin has reached 31.6%, and the company's operating cash flow has grown by 142% compared to the same period last year, marking the highest level in Q2 history.

All of these factors align well with investors' demands in the current environment.

Additionally, in March of this year, the company introduced Einstein GPT, integrating OpenAI's generative artificial intelligence technology into its own AI products. The company also states that it is "leading customers into a new era of artificial intelligence."

Valuation

Firstly, in August, the company raised the prices of its core cloud products by 9%, marking the first price hike in seven years. We anticipate that this move will undeniably benefit the company's revenue and profits, potentially exceeding the company's own projections.

Regarding the valuation of CRM, the most significant misconception is directly comparing its GAAP profits for a price-to-earnings ratio analysis, which would position it as a high P/E ratio incumbent company, seemingly impeding a feasible entry point.

However, this is a misapprehension.

1. Depreciation and amortization expenses should not be encompassed in Salesforce's valuation, as they are unlikely to substantively impact the fundamental quality of the company's operations.

2. The transient impact of restructuring costs won't affect the long-term profit margin; it might even lead investors to underestimate the long-term profit margin.

By excluding these non-substantive expenses, the intrinsic value derived suggests that the company is severely undervalued.

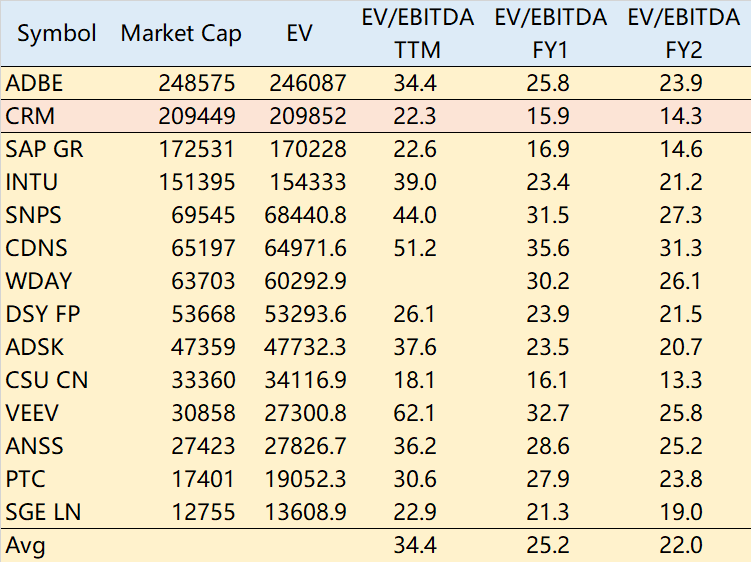

Currently, the average EV/EBITDA (TTM) of the top 10 companies in the industry is 34x. It's projected to be 25x in 2023 and 22x in 2024.

Considering CRM's growth rate, with the expected EBITDA of $14.7 billion by 2024 and discounting at an average WACC of 10.5%, with a 22x EV/EBITDA, the per-share value could reach $297. This is a 30% premium over the post-market price of $227.

Consequently, there is still a 30% upward potential for CRM

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

The ticker did not make a new high, and will most likely start a consolidation phase before the next leg higher ( or lower).

this post lead me to rethink about my previous investment. which deeply is lack of professional and comprehensive consideration

it is time for me to treat this stock strictly. HOLD it is perhaps a very good taste

surpassing expectation is normal thing because people have inclination to be conservative.😁😁😁

I think that CRM has enough power to go higher