Why TCOM still plunge at surprising earnings?

On Tuesday, September 5th, China's largest online OTA, $Trip.com Group Limited(TCOM)$ announced its 2023 Q2 performance. $TRIP.COM-S(09961)$

It is evident that the post-pandemic travel business has surged, boosting the company's overall performance, surpassing market expectations raised after adjustments. In the short term, the market remains optimistic about the recovery of the tourism sector, but the stock performance is not particularly strong due to the fact that the market had already priced in some of these expectations in the previous quarter.

This has led to a situation where some are "buying the rumor, selling the fact," especially when looking at the performance in the Hong Kong stock market.

Two major factors that consistently constrained Ctrip's valuation are its high debt and goodwill. Although there has been some relief, these concerns still exist, and it is believed that several more quarters will be needed to return to normal levels.

Earnings Review

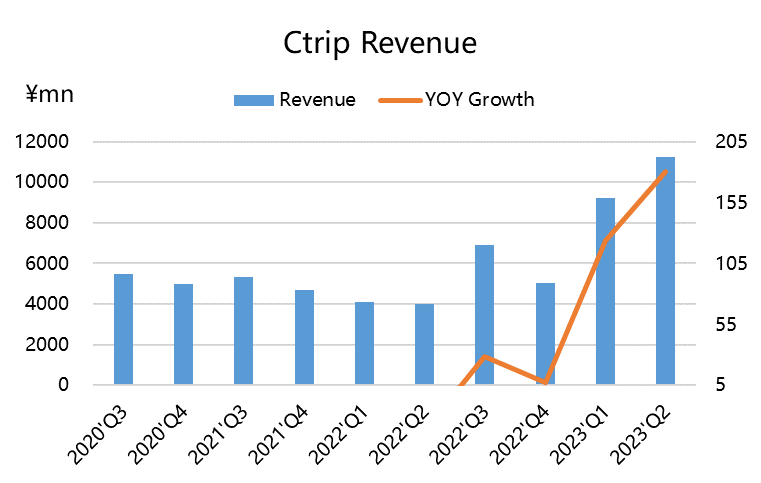

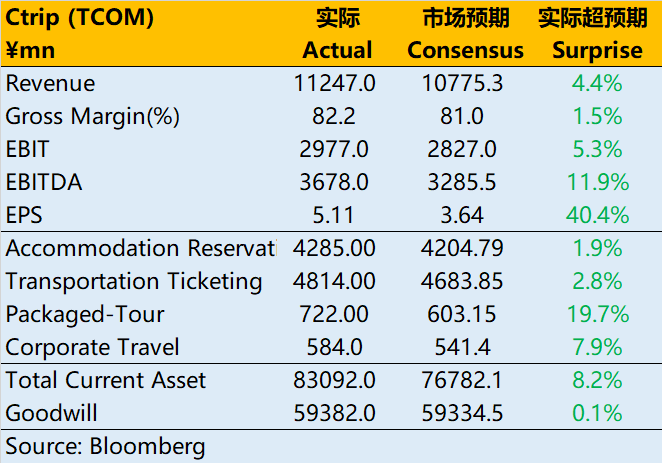

Revenue soared by an astonishing 180% year-on-year to 11.2 billion yuan, surpassing market expectations of 10.78 billion yuan and also exceeding the pre-pandemic 2019 level by 29%.

Among these figures, accommodation booking revenue increased by 216% year-on-year to 4.29 billion yuan, slightly higher than analysts' expectations of 4.2 billion yuan.

Domestic hotel booking volume increased by 170%, growing by over 60% compared to the same period in 2019.

Traffic ticket revenue increased by 173% year-on-year to 4.81 billion yuan, exceeding the market's expected 4.68 billion yuan.

Ctrip stated that outbound hotel and flight booking volumes have recovered to over 60% of the 2019 pre-pandemic levels, while the entire industry's international air passenger volume has only returned to 37% of the 2019 level.

Additionally, flight booking volume on the company's global online travel platform increased by over 120% year-on-year, nearly doubling compared to the same period in 2019.

Furthermore, guided tour revenue reached 722 million yuan, surpassing the market's expected 603.2 million yuan, with a year-on-year growth rate of 492%.

Corporate travel revenue increased by 178% year-on-year to 584 million yuan, exceeding analysts' expectations of 541 million yuan.

In terms of profit, gross profit increased by 203.9% year-on-year to 9.24 billion yuan, surpassing market expectations of 8.72 billion yuan, with a gross profit margin of 82.2%.

Net profit attributable to shareholders was 631 million yuan, compared to 69 million yuan in the same period in 2022, representing an 814.5% year-on-year increase.

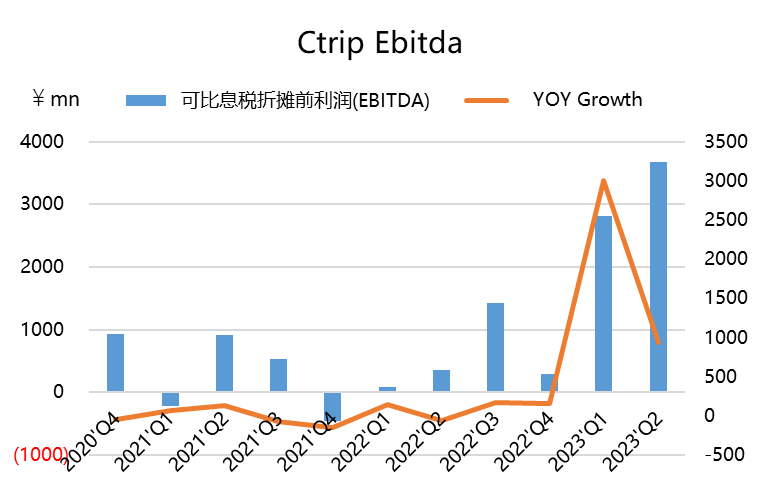

EBITDA was 3.68 billion yuan, exceeding the market's expected 3.29 billion yuan.

Investment Highlights

Clearly, the Q2 travel business has rebounded significantly. Driven by pent-up travel demand that remains robust, travel bookings continue to rise, leading to a significant recovery in the company's performance. Despite limited aviation capacity recovery in Q2, travel activities continue to rebound strongly.

At the same time, expectations for Q3 can be more optimistic, as outbound tourism, although affected by exchange rates, can still bring incremental growth in overseas markets.

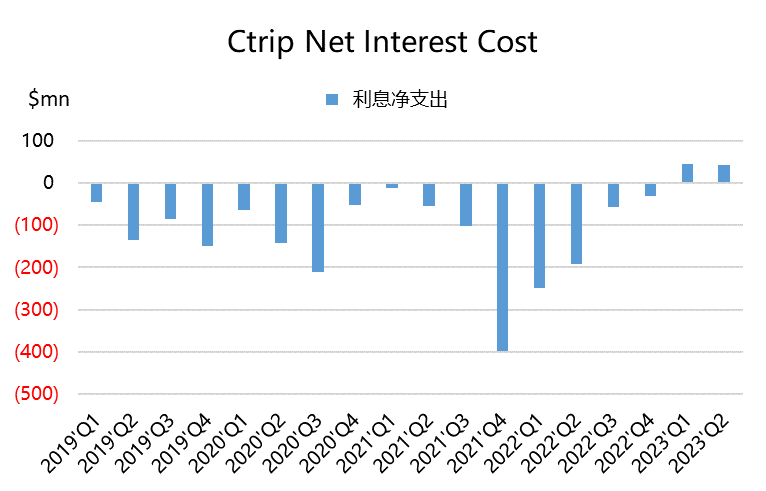

This quarter's net interest expenses have also reached the highest level since the pandemic began, due to higher interest rates overseas compared to lower domestic interest rates, which has had a certain negative impact on the company's profits.

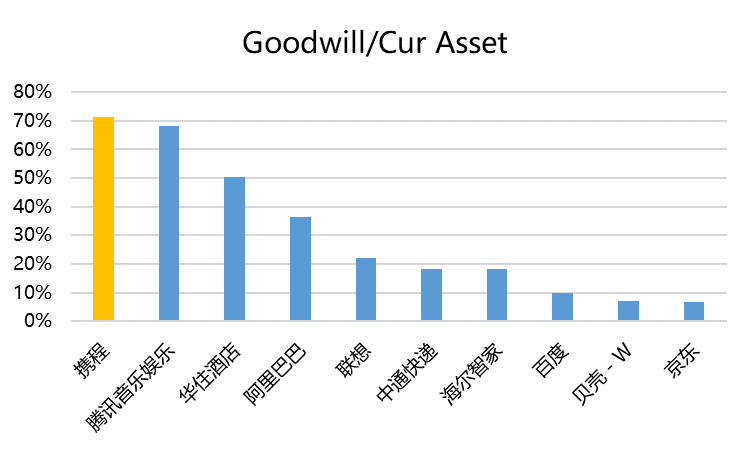

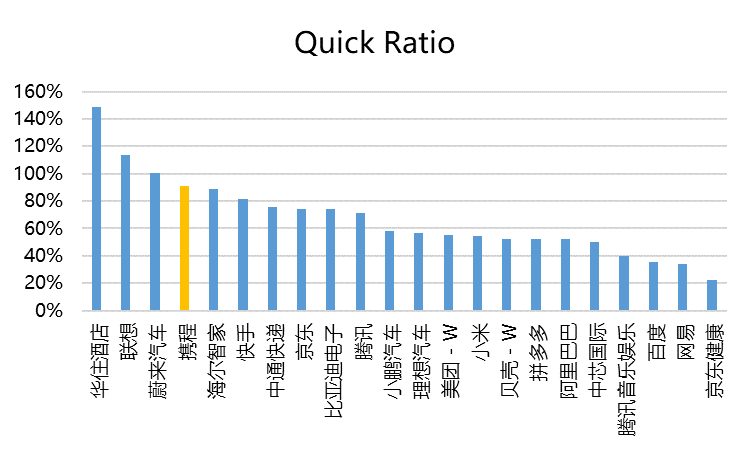

The main factors affecting Ctrip's valuation are its relatively high debt ratio and the substantial goodwill brought about by previous acquisition activities. The ratio of current liabilities to current assets is the highest among components of the $NASDAQ Golden Dragon China Index(HXC)$ and the $HSTECH(HSTECH)$ , and its goodwill-to-current assets ratio is also among the highest, which to some extent lowers its asset quality.

We believe that in the short term, OTA companies will continue to benefit from strong travel demand and maintain excellent performance, to some extent addressing the shortcomings from before. However, in the long term, as shareholders, we still need to see a transformation in the company's asset quality to have a greater valuation potential.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

There’s so many gaps that have to be filled to the downside. I’m a buyer if we get to the low $20’s. Not a penny higher. Would love to retest the lows as well. Way overbought. I do think this company is a money making machine, but we need to fill the downward channel before setting new highs.

$26 or lower before 12/21/23. Sell into the pop tomorrow and secure your gains .

Amazing earnings in every facet. Now let's see if price does what it legitimately should do on wonderful earnings figures ?

beating earnings with a solid number and it drops with 5%? I'm never putting another dollar into this sketchy company!

TCOM had great financial reporting. Any reason why the drop?