C3.AI tumbles in difficulties of profit

$C3.ai, Inc.(AI)$ dropped more than 9% in after-hours trading. This came after the company released its current financial report, which slightly exceeded expectations but provided a less optimistic outlook.

While many companies in the true AI sector have been raising their expectations significantly, C3.ai decided to lower theirs and postpone their profitability timeline, raising doubts in the market once again about the company's true potential.

Despite the speculative frenzy that drove the stock up over 181.1% amid this year's AI boom, it's important to note that, as we've mentioned before, despite having the best name in the market (AI), it is one of the least AI-focused companies in the industry.

The company's business model resembles a giant sales operation where they leverage others' technology and sell it to customers. Their performance largely depends on continually providing users with more integrated services and incorporating advanced models into C3 AI's enterprise AI products, with unit sales (Pilot) being a crucial factor in future performance growth.

Q1 Performance Review:

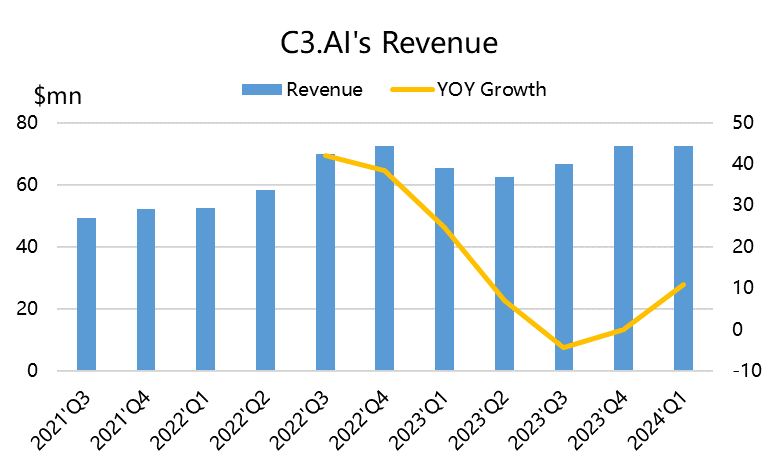

- Revenue reached $72.36 million, a year-over-year growth of 10.8%, surpassing market expectations by $7.6 million.

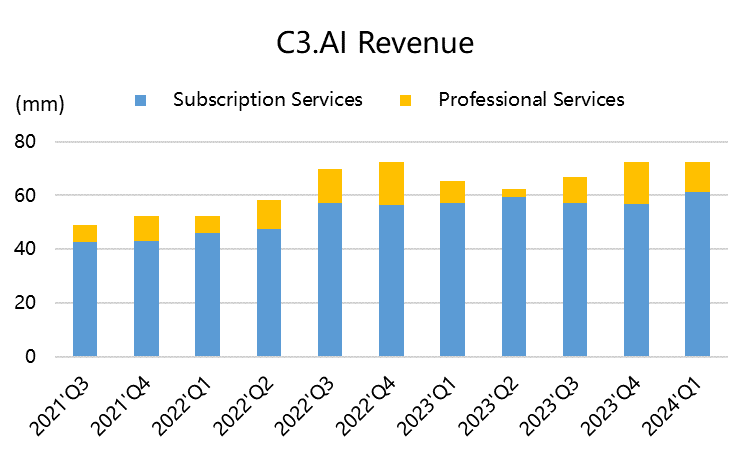

- Subscription revenue accounted for $61.40 million, representing 85% of total revenue.

- Remaining Performance Obligation (RPO) stood at $334.6 million.

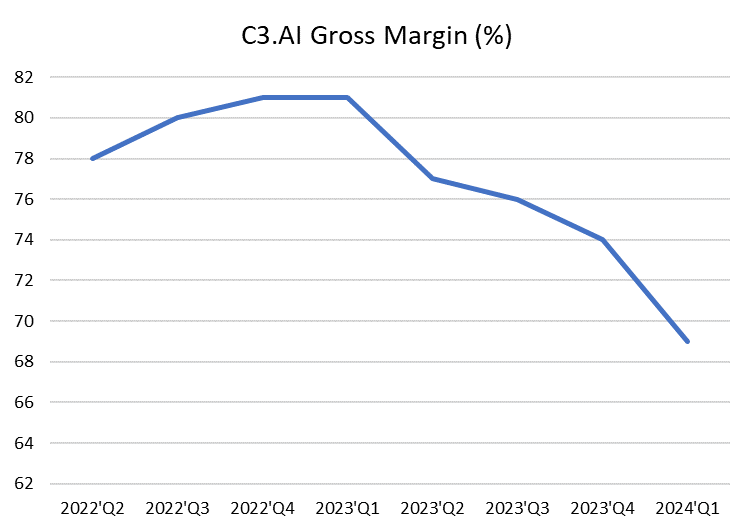

- Non-GAAP gross profit was $49.60 million, with a gross margin of 69%, which continues to decline.

- Current RPO is $170.6 million.

Q2 Outlook:

- Total revenue is expected to range from $72 million to $76.5 million.

- Non-GAAP operating loss is projected to be between ($270 million) and ($400 million).

2024 Fiscal Year Outlook:

- Total revenue is forecasted to be between $295 million and $320 million.

- Non-GAAP operating loss is expected to increase from the previous $50 million to $75 million range to $70 million to $100 million.

- The company anticipates not achieving profitability until the 2024 fiscal year but expects to achieve positive cash flow during that period and in 2025.

The company also announced the launch of a new C3 Generative AI Suite, which includes 28 new domain-specific generative AI solutions tailored for various industries, business processes, and enterprise systems.

The 2024 performance suggests that sales may have reached a plateau, with revenue staying flat at $72.36 million but still growing 10.8% year-over-year. Additionally, the company reported an adjusted loss of $0.09 per share. Analysts had anticipated a loss of $0.17 per share and revenue of $71.6 million.

In terms of investment, AI is an attribute of meme stocks, and it's a game of existing funds. In the first half of this year, C3.AI was shorted by research institutions because its valuation was not low. Due to its ongoing long-term losses, the current Price-to-Sales ratio (PS) is as high as 16 times, far above the industry average of 6 times. At the same time, the revenue forecast for the next fiscal year results in a forward EV/Sales ratio of 10 times, which is higher than the industry average of 5 times.

The extreme volatility is also due to the influx of too many short sellers and the impact of the bearish market environment. The game between retail investors is quite exciting.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

I have zero worries about the long term investment I have in AI. AI has great potential. And all the -talk about it going to $10 is false; I’d buy it again below my cost basis of $24.

AI has been around for decades. Nothing but a bunch of hype. Sure, faster chipsets make it a little faster, but it is still nothing more than machine learning with human input.

I couldn't be more optimistic about the future of AI after reading the conference call transcripts.

This stock is still not proven winner. Usually they skyrocket and come down heavily until proven.

Opened short positions on nividia. AI party is over in the short term