Why did Micron Slip As Beated Q4 Earnings?

Micron Technology (MU) released its FQ4 financial report after the market closed on September 27th. While the quarterly performance exceeded market expectations, the guidance for the next quarter appeared somewhat conservative, casting a shadow on investor sentiment. As a result, the stock fell more than 3% in after-hours trading.

In terms of performance, for Q4 ending on August 31st, Micron reported revenue of $4.01 billion, down 29.6% year-over-year but surpassing the expected $3.93 billion. The adjusted gross margin was -9.1%, higher than Wall Street's expected 10.2%, and the adjusted EPS was -$1.07, while the market expected -$1.18. Operating cash flow was $249 million, lower than the analyst's forecast of $1.17 billion, but the operating cash flow for the same period last year was $3.78 billion, and the previous quarter was $24 million.

As for guidance, Micron expects Q1 revenue to be between $4.2 billion and $4.6 billion, surpassing the market's expected $4.21 billion. The adjusted loss per share is projected to be between $1 and $1.14, worse than the market's expected loss of $0.96 per share. The adjusted gross margin is expected to be between -2% and -6%, below the expected 0.66%.

Additionally, Micron stated that capital expenditures for the fiscal year 2024 are expected to be slightly higher than in 2023, and they anticipate pricing and profitability to gradually improve throughout the year.

Investment Highlights

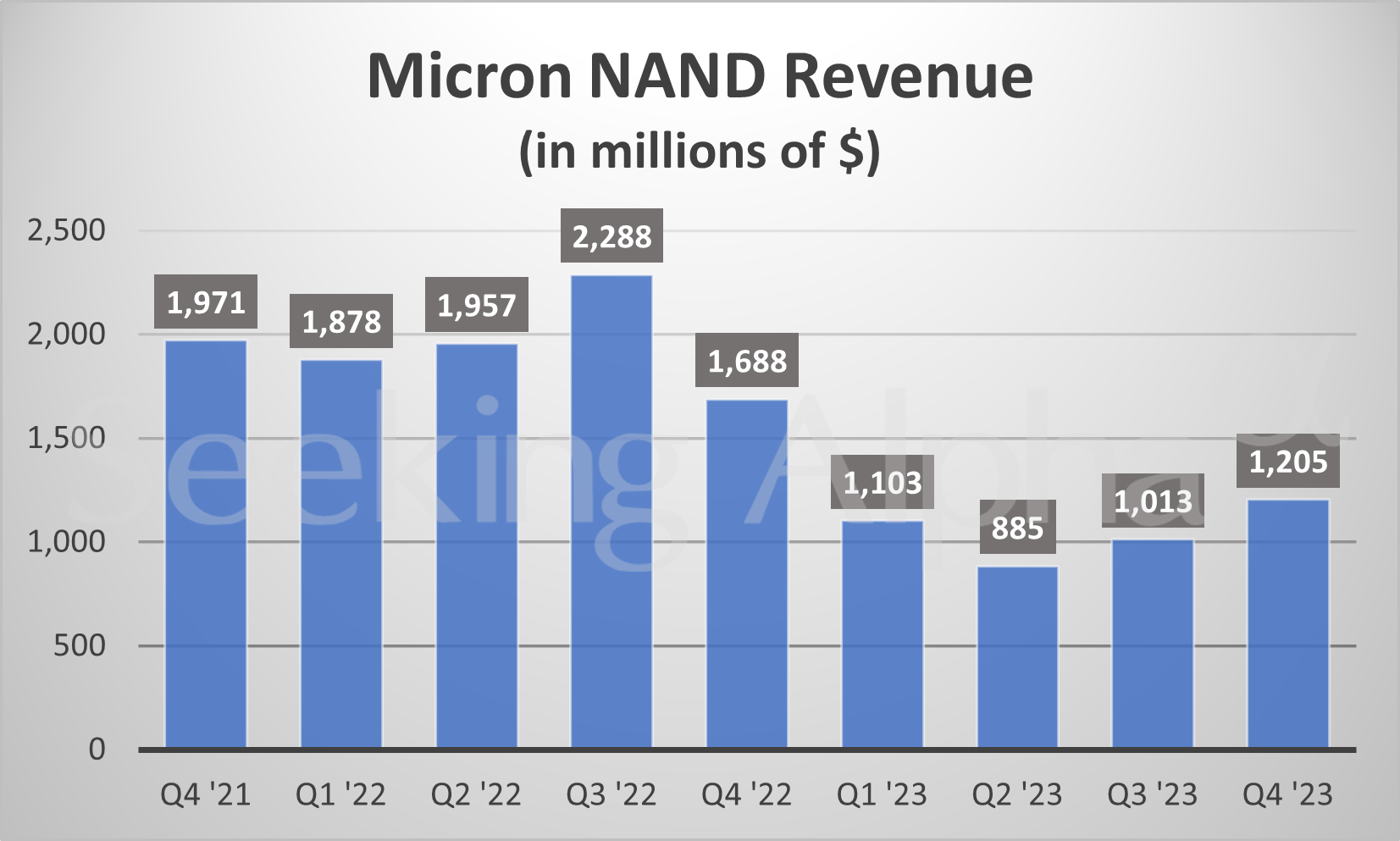

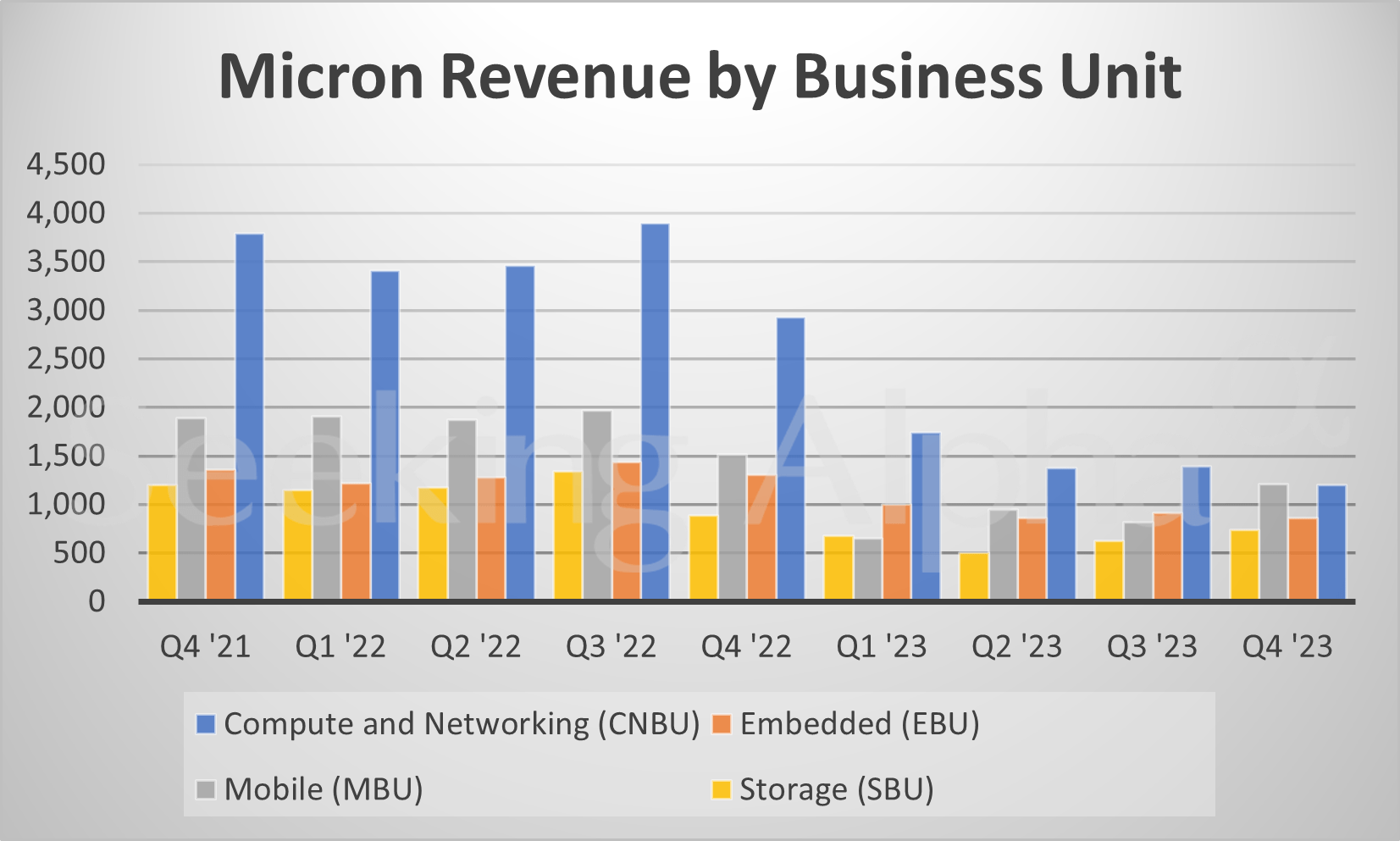

Micron benefiting from seasonal factors in the consumer electronics market this quarter, with significant growth in the mobile phone business, and overall revenue levels meeting expectations. The gross margin has started to improve (-9%), but there hasn't been significant inventory changes. Most PC, mobile phone, and automotive customers' inventories have returned to normal levels, while traditional server business is reducing inventory but related revenue has bottomed out.

Regarding guidance, Micron expects industry growth rates to surpass long-term CAGR data, and storage is entering a year of recovery. Industry supply is expected to fall short of demand, especially for DRAM, with DDR5 shipments surpassing DDR4 in early 2024. They plan to maintain low production levels while investing in advanced process equipment to support higher yields.

Capital expenditures for the next fiscal year may increase slightly, with a significant increase (more than doubling) in advanced packaging Capex for HBM. It is expected that data center growth will begin in Q4, PC sales will increase by 5-10% next year, mobile phone sales will increase by 5%, and industrial control and automotive revenue will reach record levels, with all end terminals maintaining a trend of capacity improvement.

Micron is optimistic about the replacement cycle brought about by AI-enabled terminals (PCs and mobile phones) and expresses a high degree of confidence in HBM.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Micron is losing money because of standard semiconductor problem - inventory at clients and in the channel. Not because of competition. Once the inventory gets exhausted the oligopoly will put the screws on again.

Since the last ER Micron moved their profitability target from FQ4 next year forward to FQ3, that's a 3 month improvement that the market should like (possibly after tomorrow)

Negative free cash flow is not good for this overhyped, overpriced, pumped up stock. The belief that companies will pay endlessly for something that is just a hype.

Will keep the stock in the $60-$70 range for the next decade.

Mu should have been 82 after earnings. So much positive for long term, LONG