Will Apple lose its market value throne in Q4?

$Apple(AAPL)$ may be one of the most important reports determining the market sentiment this quarter. As one of the largest components of the index, despite a continuous year-on-year decline in revenue for four quarters, the company's profits still exceeded expectations, demonstrating resilience in the consumer goods counter-cyclical economic environment for a mature company.

There was some market volatility after the financial report, but it wasn't particularly severe. Because expectations were not high, profit-taking occurred early. The guidance for the next quarter was not particularly optimistic, and long-term investors, including $Berkshire Hathaway(BRK.B)$ may reconsider their positions based on the current valuation and potentially reduce their holdings (observe Q3's 13F).

Investment Highlights

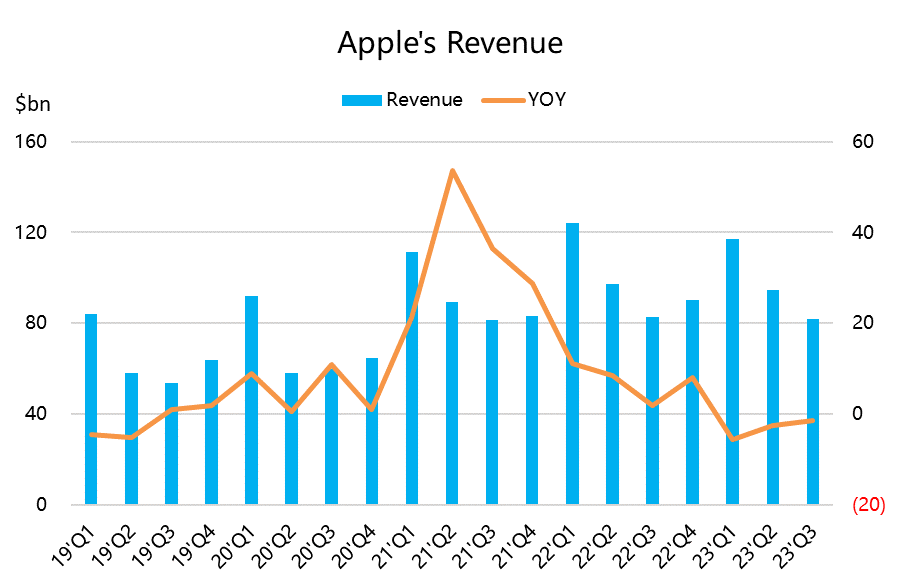

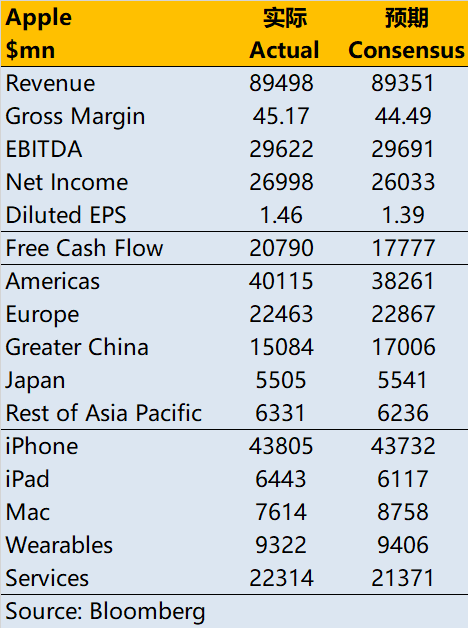

Until the end of September in fiscal year Q4 2023, the revenue was $89.5 billion, slightly better than the market's expected $89.3 billion, but still a year-on-year decline of 0.7%, marking four consecutive quarters of decline. On one hand, there was a year-on-year decline in Europe, Greater China, and Japan, and exchange rate effects were also important factors. On the other hand, the demand for Mac and iPad businesses this year has been insufficient and continuously dragging down performance. Even wearable devices experienced a year-on-year decline, while the same period last year saw an increase due to new product seasonality.

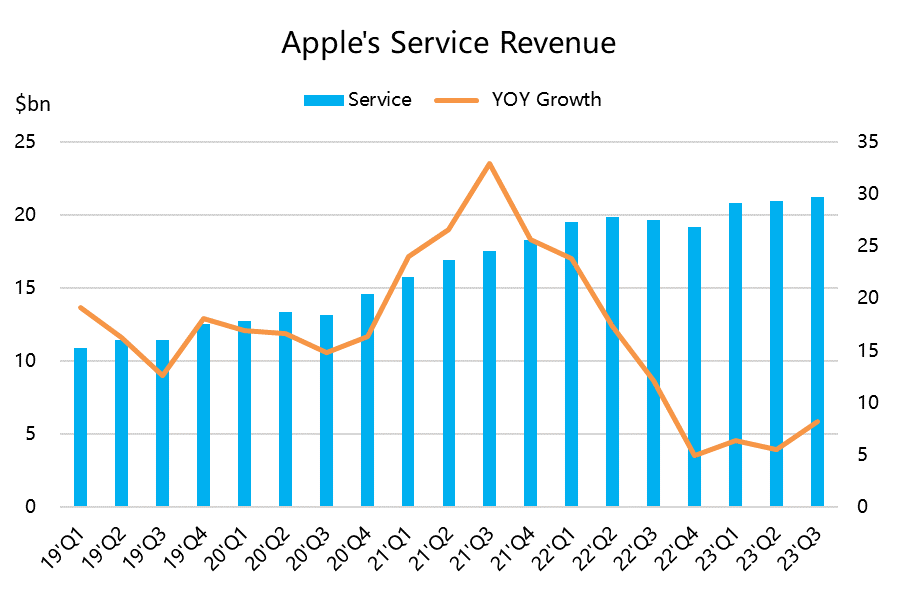

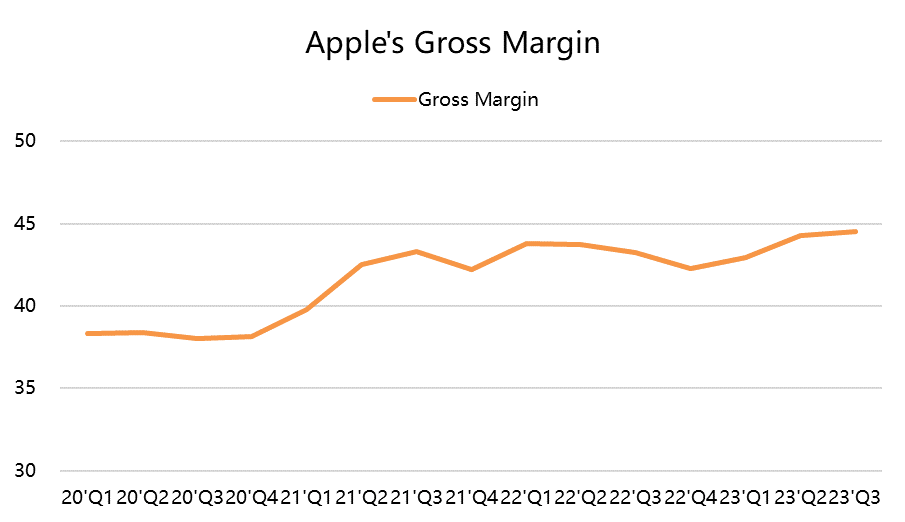

Gross margin increased to 45.2%, a year-on-year increase of 2.9 percentage points, higher than the market's expected 44.5%. This was mainly driven by the growth of the higher-profit service business. The gross margin of the software business has remained above 70% for nine consecutive quarters.

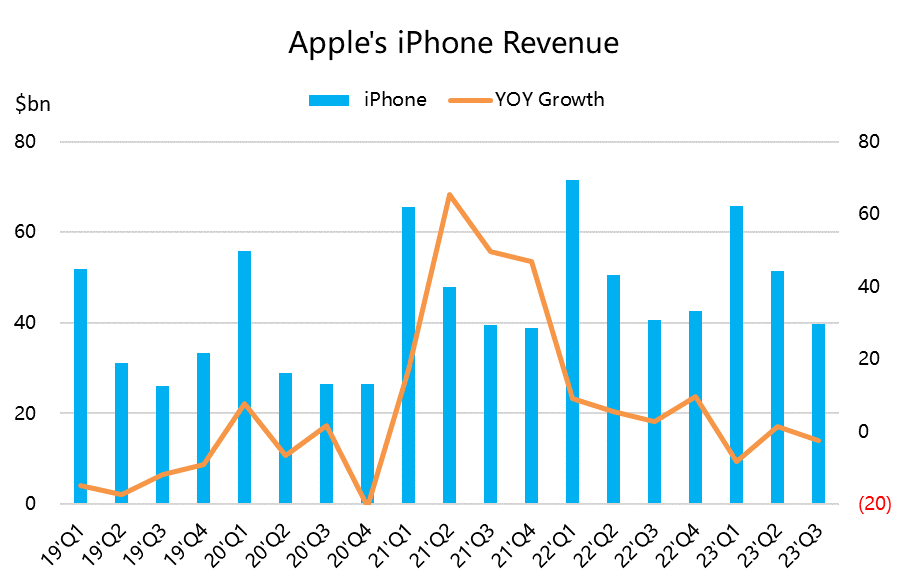

iPhone business, which accounts for more than half of total revenue and is of most concern to the market, achieved revenue of $43.81 billion in the quarter, a year-on-year increase of 2.8%, in line with expectations. During the conference call, executives also mentioned encountering significant challenges in the Chinese market with intensified competition. It is conceivable that Android and Huawei's products have indeed posed challenges to Apple's iPhone series. However, CEO Tim Cook remains optimistic and expects growth to continue in the next quarter. However, it is likely that Apple will bid farewell to the previous "double-digit growth" despite achieving growth.

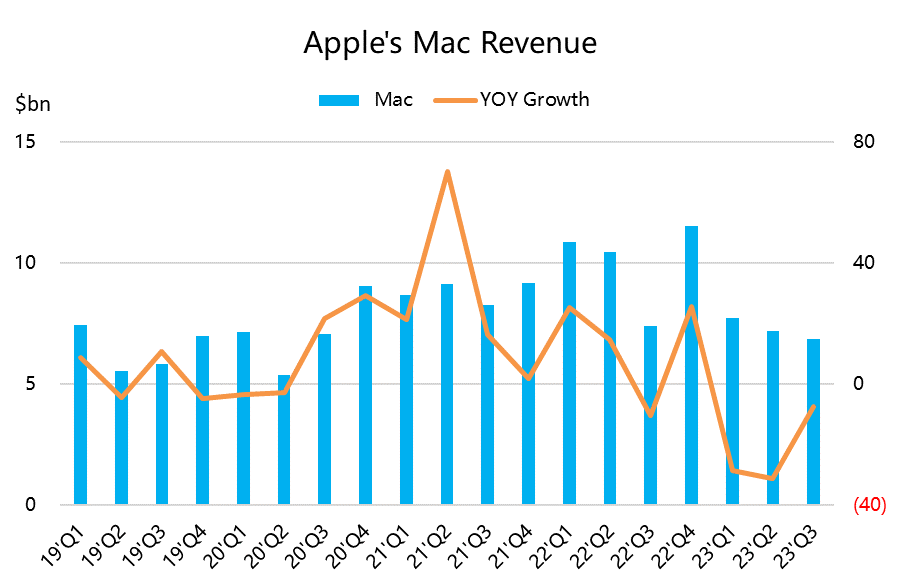

As for other hardware products, except for the newly released M3 chip Mac which may regain some ground in the next quarter (but it may only be temporary), executives predict that iPad and wearable devices may experience a "significant decline" in the December quarter, which is also seen as a negative signal by the market. In fact, Mac's performance in the past few quarters has been poor, indicating that the new M2 chip product did not receive a warm welcome from the market.

Apple's profits can continue to strengthen, with net profit of $22.96 billion exceeding market expectations and earnings per share of $1.46 surpassing the expected $1.39, a year-on-year growth of 13%. However, the revenue bottleneck it faces may continue to be the "biggest stumbling block" in maintaining its current PE valuation of 30.

Currently, Apple's PE ratio is 29 times, and the new VR product that supports its revenue will not be released until next year. There is no timetable for AI to be embedded in existing businesses and form a stable cash flow. More and more investors will think that Apple is "falling behind" in the AI competition and "vote for companies with more promising AI businesses."

$Microsoft(MSFT)$ market value is currently $2.59 trillion, while Apple's is $2.78 trillion. Will the throne of the top market value be handed over again after many years?

Earnings Review

In terms of revenue

Apple's overall revenue was $89.5 billion, a decrease of 0.7% compared to the previous year, which was in line with market expectations of $89.31 billion.

In terms of products, the hardware business decreased by 5.3% year-on-year, while the software business increased by 16.3%. iPhone revenue, which accounted for half of the total revenue, was $43.81 billion, a 2.8% increase compared to the previous year and in line with expectations. Mac revenue was $7.61 billion, lower than the expected $8.63 billion, a decrease of 33.8% year-on-year. iPad revenue was $6.44 billion, better than the expected $6.07 billion, a decrease of 10.2% year-on-year. Wearable device revenue was $9.32 billion, lower than the expected $9.43 billion, a decrease of 3.4% year-on-year.

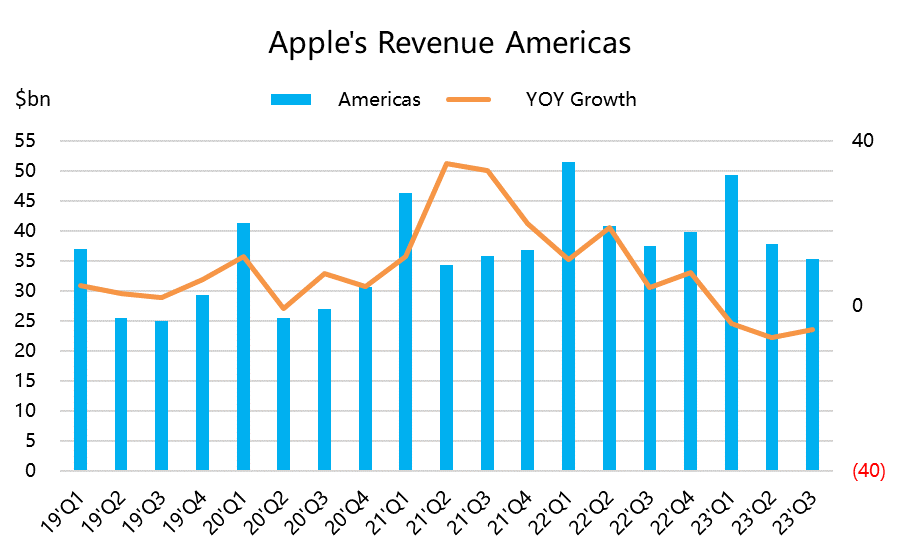

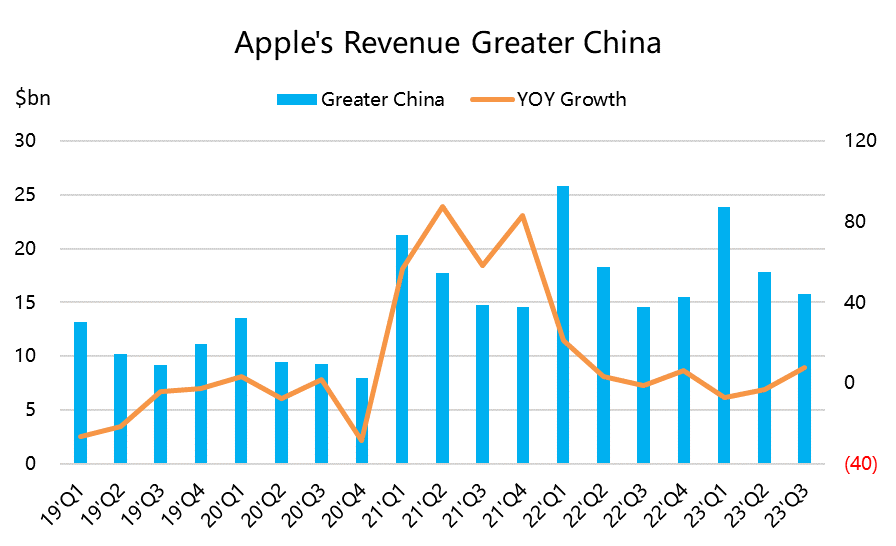

In terms of regions, revenue from the Americas was $40.12 billion, a 0.8% increase compared to the previous year; revenue from Europe was $22.46 billion, a 1.5% decrease; revenue from Greater China was $15.08 billion, lower than the expected $17 billion, a 2.5% decrease; revenue from Japan was $5.5 billion, a 3.4% decrease; and revenue from other Asia Pacific regions was $6.33 billion, a 0.7% decrease.

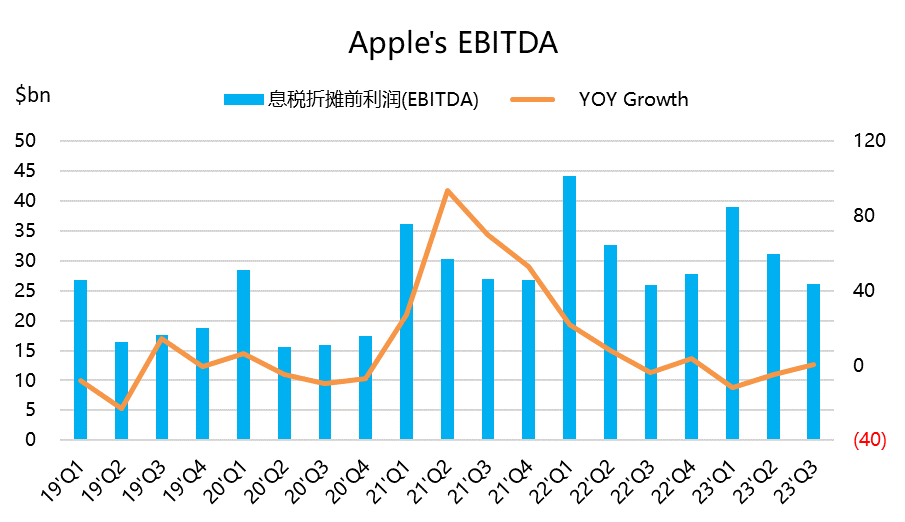

In terms of profitability, the company's gross margin was 45.2%, an increase of 2.9 percentage points compared to the previous year and higher than the expected 44.5%. The hardware gross margin improved to 36.6%, while the software services gross margin was 70.9%. As a result, the company's operating profit increased to $27 billion, an 8.3% increase compared to the previous year, with earnings per share of $1.46, exceeding expectations of $1.39 and a 13% increase compared to the previous year. EBITDA was $29.6 billion, in line with expectations.

In addition, the company spent $25 billion on stock buybacks and dividends, and announced a cash dividend of $0.24 per share.

In terms of guidance, Apple did not provide specific values but only stated during the conference call that it expects total revenue for FY2024Q1 until the end of December to be similar to the same period last year, around $117.2 billion. However, market expectations include total revenue for the three months including the heavyweight holiday shopping period to recover and increase to $122.2 billion year-on-year. This indirectly indicates poor guidance.

In summary

As Apple's valuation is essentially an anchor for the entire market, any changes in Apple also affect investors' overall return on US stocks.

With a valuation of around 30 times earnings, it may not be considered high given the growth rate in 2021, but with current revenue reaching a bottleneck and relying solely on an increase in the proportion of services (Apple Store revenue may be a hidden risk) and improved operational efficiency, it may still be too strained.

Fortunately, pessimism towards Apple has been present for some time and is partly priced into the market. We should pay more attention to the 10 trading days after this financial report to see if there will be further profit-taking brought by long-term institutions.

Of course, as the largest weighted stock in the market, Apple's trading is no longer just a reflection of its own valuation but also reflects market sentiment. Therefore, if sentiment remains extremely pessimistic in the short term, there may still be capital inflows led by speculative trading, arbitrage, and other quantitative funds.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.