Xiaomi Q3: Definitely Rise Again

$XIAOMI-W(01810)$ announcing its Q3 2023 financial report. Due to the recent hot sales of Xiaomi 14, the company's stock price surged from the bottom, even providing some guidance for the Hong Kong technology sector. Therefore, this financial report has become a focus of market attention. $Xiaomi Corp.(XIACY)$

Investment highlights

Overall, Q3 revenue and profits both exceeded market expectations, further verifying the success of the company's "dual-brand strategy" and its momentum of "rising from the ashes."

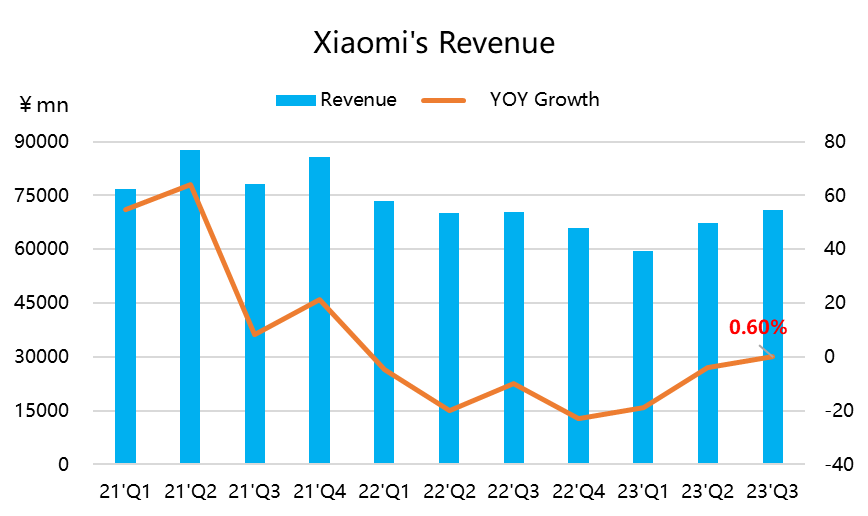

Revenue growth is not surprising. This quarter's revenue reached 70.89 billion yuan, a year-on-year increase of 0.6%, and the first time since Q4 2021 to recover positive growth. Smartphones, IoT, and internet services including advertising all performed well.

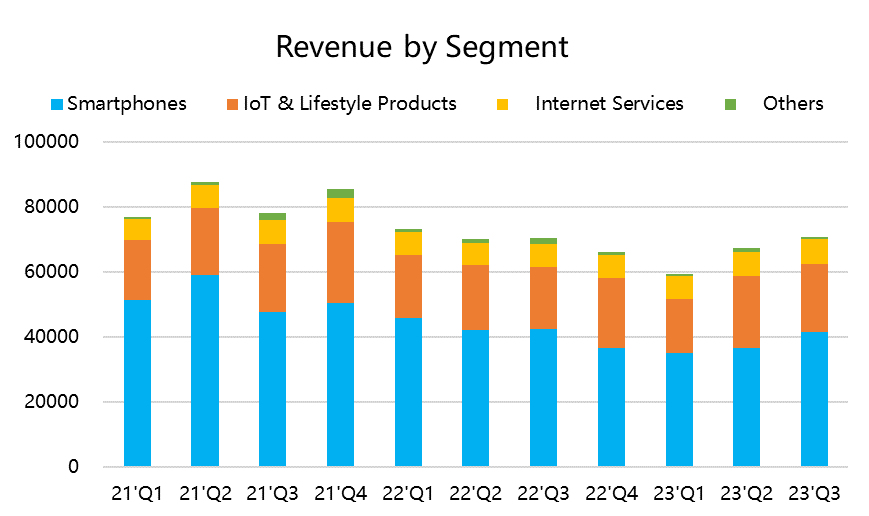

Although smartphone revenue declined, it was higher than the industry average, and market share increased. The "high-end strategy" and "inventory reduction" worked together effectively, but the next quarter is more worth looking forward to. Overall, smartphones fell by 2% on the first day, but the expected decline was 6%, so it performed well. In the overall environment where global shipments in Q3 fell (-1.1%), Xiaomi's shipments increased by 4.0%, and its market share reached 14.1% (+0.5%), ranking third in the world in 55 countries. The average selling price (ASP) decreased by 5.8% year-on-year, mainly due to strong growth in shipments in emerging markets with lower ASPs such as Latin America, Africa, and the Middle East (which can also help reduce inventory), but ASP in mainland China increased (high-end route). The proportion of overseas business increased from 45.2% last year to 48.9%. Although India is restricted, European business is booming.

At the same time, it is obvious that Xiaomi 14 is currently selling well and is expected to have a stronger impact on Q4 performance. Therefore, Q4 performance is more worth looking forward to, and there is almost no suspense in returning to growth and increasing profits.

IoT devices hit a new high, white goods grow against the trend, and "cost-effective AI products" become a star. It must be said that the 8.5% year-on-year growth of IoT business in the fiercely competitive Chinese home appliance market is very rare and exceeds market expectations. This is also due to the high growth of smart large appliances. More importantly, the gross profit margin increased by 4.3% to reach 17.8%. The AIoT platform has connected an additional 699 million IoT devices, a year-on-year increase of 25.2%. Currently, more and more emphasis is placed on intelligence, and consumers have more choices of cost-effective AI products. Xiaomi's user group can also be regarded as a key factor for future synergies.

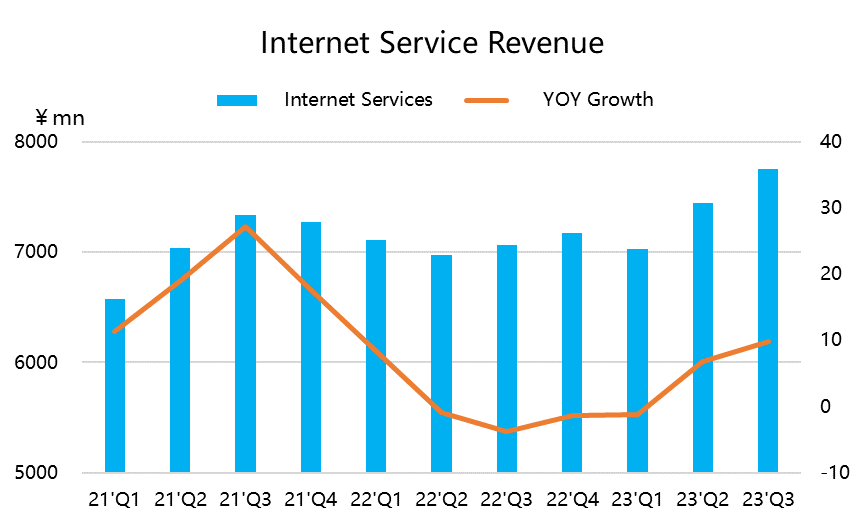

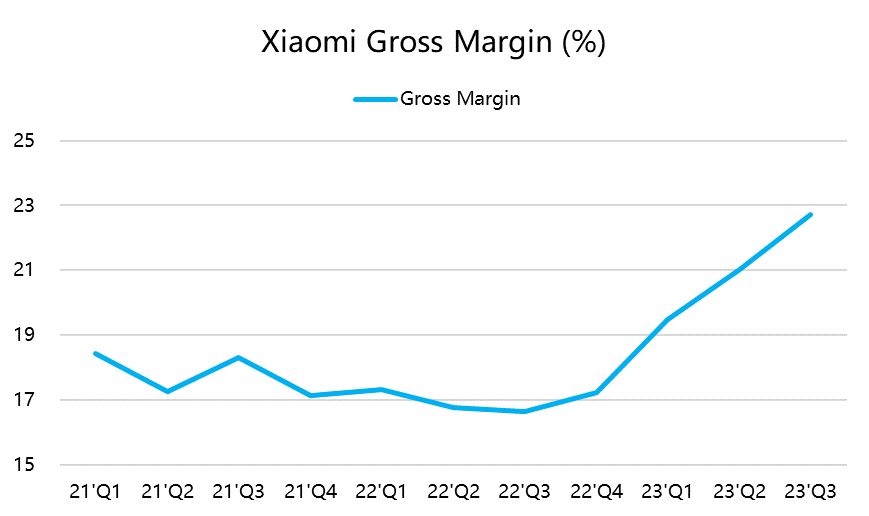

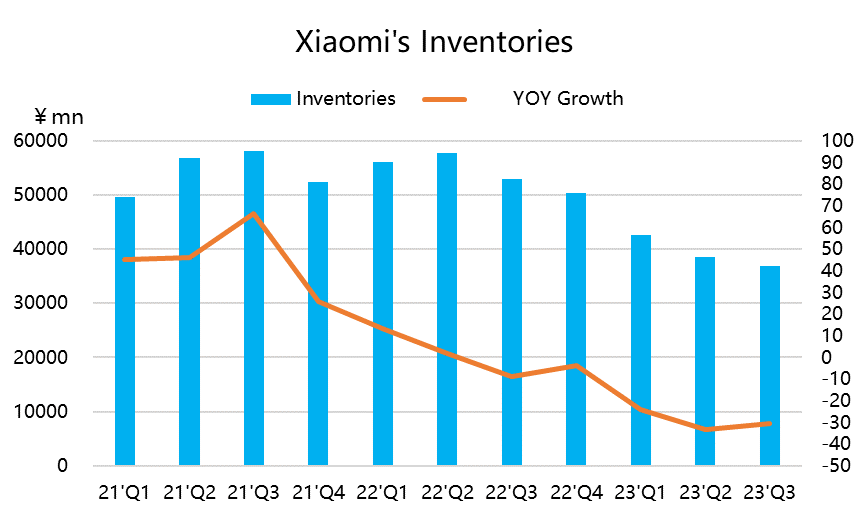

High-profit businesses have helped boost the overall profit margin of the company. In Q3, the gross profit margin increased by 7.7 percentage points. In addition to the effect of the new "high-end" route for smartphones, the increase in the proportion of high-profit businesses, such as a 9.7% increase in revenue from internet services, with an unexpected 3.5% increase, was mainly driven by advertising, and the gross profit margin also reached 74.4%, an increase of 2.3%. The refined operation of advertising business resulted in a record high overall revenue of 5.4 billion yuan. Gaming revenue also reached 1.1 billion yuan, a year-on-year increase of 56%. In addition, inventory fell by 30% this quarter, reaching a new low in 11 months. The overall internet service business maintained long-term growth.

Net profit reached 5.99 billion yuan, including 1.7 billion yuan in car costs. The three major expenses were relatively controlled, and the adjusted net profit increased by 180% year-on-year and 16.5% quarter-on-quarter to reach 6 billion yuan. At the same time, cash reserves were sufficient, reaching 127.6 billion yuan, with a free cash flow of 5.66 billion yuan, which also provided strong support for car manufacturing. The financial report did not reveal too much about the car project, and it is expected that there will be relevant introductions during the conference call.

In terms of valuation, including Q3 financial report data, Xiaomi's multiples PE has returned to around 22 times; the EV/EBITDA for the past 12 months has fallen to around 15 times, both lower than the average of the past five years.

Q3 Earnings Review

Revenue

Revenue was 154.6 billion yuan, a year-on-year increase of 10%, which was basically in line with market expectations of 152 billion yuan, and the year-on-year growth rate was the same as that of the previous quarter;

Among them, revenue from smartphones was 41.649 billion yuan, a year-on-year decrease of 2%, higher than the market expectation of 41.183 billion yuan, mainly due to a decrease in average selling price (ASP);

However, revenue from IoT and consumer products was 20.673 billion yuan, a year-on-year increase of 8.5%, higher than the market expectation of 20.418 billion yuan;

Internet service revenue was 7.756 billion yuan, a year-on-year increase of 9.7%, higher than the market expectation of 7.599 billion yuan; among them, advertising revenue was 5.4 billion yuan, a year-on-year increase of 15.7%; other revenue was 817 million yuan.

Profit

Gross profit margin was 22.72%, higher than the market expectation of 21.41%, mainly due to the fast growth of high-gross-margin service business. At the same time, the gross profit margin of the smartphone business was 16.6%, an increase of 7.7 percentage points year-on-year.

Overall inventory was 36.8 billion yuan, a year-on-year decrease of 30.5%, the lowest in 11 quarters.

Adjusted net profit was 5.99 billion yuan, a year-on-year increase of 182.9%, higher than the market expectation of 4.65 billion yuan. Note that this profit includes a cost of 1.7 billion yuan for the car-making business, and the photo of Xiaomi's car has been exposed, with good market evaluation based on its appearance.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Newnew·2023-11-20HiLikeReport