Kuaishou Q3: Let the profit run

Kuaishou-W (01024) announced its Q3 2023 financial report. The recent regulatory expectations for live-streaming e-commerce caused the company's stock price to experience a pullback. However, due to optimistic expectations for Q3 performance and excellent performance on Singles' Day, the stock price rebounded again. $KUAISHOU-W(01024)$ $KUAISHOU-WR(81024)$

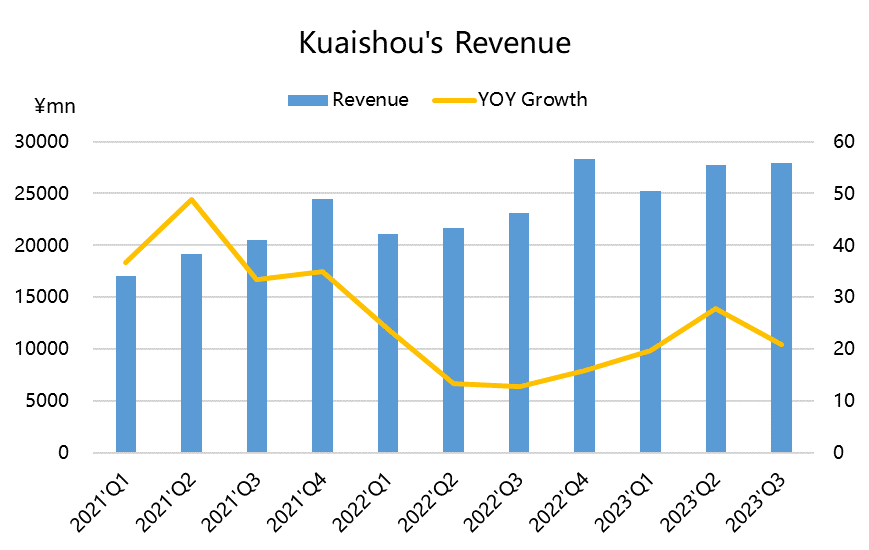

The revenue performance in Q3 was almost in line with market expectations, but the profit performance exceeded expectations. In addition to the company's further reduction in bandwidth costs (a major expense for short video companies), which led to an increase in gross profit margin, the continued decline in the three major expense ratios also contributed to higher net profit and improved the company's cash flow and valuation basis.

Investment Highlights

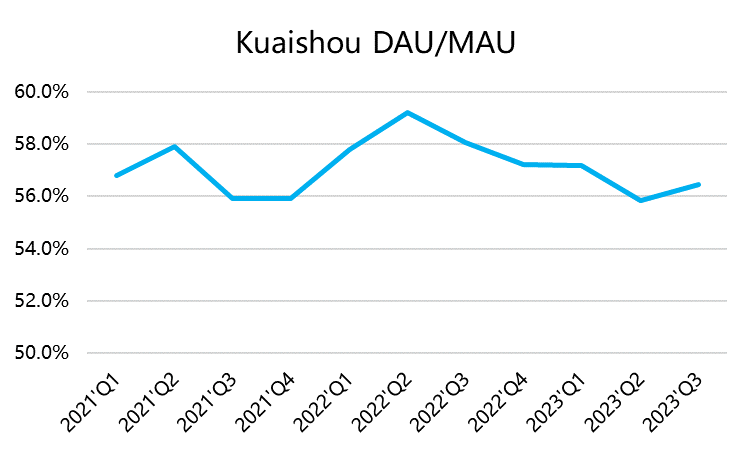

User growth and stickiness remain in good condition. Monthly Active Users (MAU) reached 685 million, and Daily Active Users (DAU) reached 387 million, both reaching new highs. There is still room for further growth. DAU/MAU reached 56.5%, with an average market time of 129.9 minutes per DAU. This is due to diversified high-quality content supply during the summer and continuous algorithm optimization. Short dramas and mini-games are important contributors to growth.

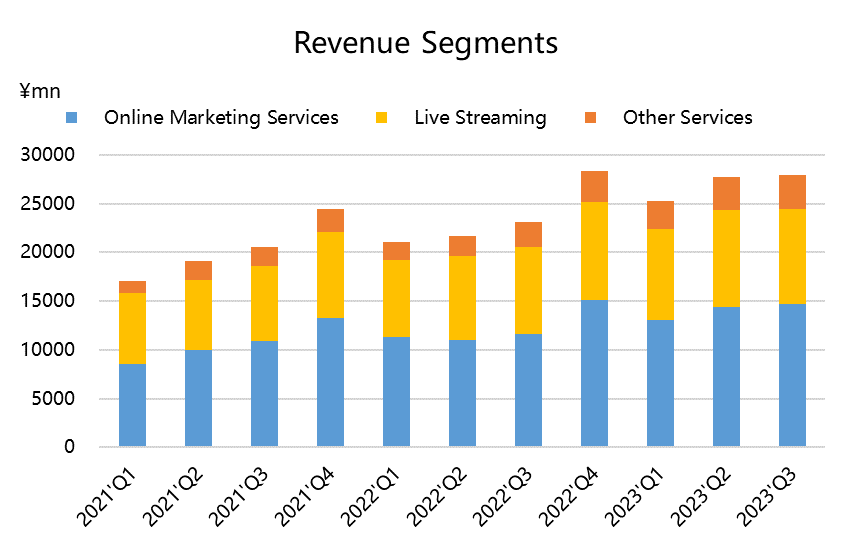

The growth of advertising revenue is not surprising, as the market already had optimistic expectations. Therefore, in Q3, it grew by 26.8% year-on-year and recovered its growth trend on a quarterly basis. At the same time, Ad load and eCPM remained relatively stable compared to the previous quarter. Kuaishou's focus this year is to build a large model for data fusion across domains and industry models with thousands of clients and thousands of models, aiming to enhance the value of advertisers. It is expected that the company will maintain strong revenue from recurring advertising business in the second half of the year.

Live-streaming media continues to grow steadily, as expected. Despite the industry facing issues of canceled ad placements, Q3's live-streaming business still achieved 8.6% growth, about 2 percentage points higher than market expectations. This indicates that KOL cooperation during the summer remained smooth and stable. Additionally, Kuaishou's advertising monetization level is relatively low, so it will continue to focus on cooperation with MCN agencies and top KOLs. However, ongoing regulatory measures in live-streaming will continue to bring pressure, which will further promote the transformation of monetization for broadcasters, MCN agencies, and platforms.

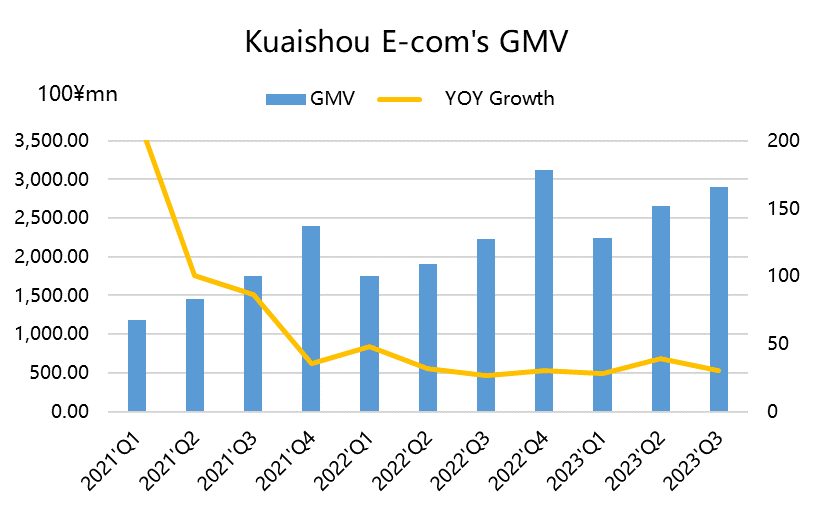

The e-commerce sector is well-prepared, although Q3 is not a shopping season, Kuaishou's e-commerce growth performance is strong. GMV grew by 30% year-on-year, which is in line with market expectations. Considering the deflationary environment in Q3, this performance is not bad. Kuaishou's e-commerce drive comes from its ecosystem based on short videos, enriched product supply, and the growth of active customers. If Kuaishou continues to include e-commerce KOLs in its monetization scope, it can further increase the fee rate and directly help improve the profitability of e-commerce. Meanwhile, although there are strict requirements for e-commerce broadcasters' qualifications, most of the platform's regulations are currently standardized, so the actual impact is expected to be relatively limited.

In terms of valuation, as it has just started to make profits, based on the PE ratio of 2024, the current price corresponds to a PE ratio of about 30 times; based on market expectations for EPS in 2025, it corresponds to a PE ratio of 16 times.

Earnings Review

Revenue

Revenue reached 27.95 billion yuan, a year-on-year increase of 21%, exceeding market expectations of 27.71 billion yuan. The growth rate is starting to decline but still remains above 20%.

Among them, internet marketing revenue was 14.69 billion yuan, a year-on-year increase of 27%, in line with market expectations. Live streaming revenue was 9.7 billion yuan, a year-on-year increase of 8.6%, exceeding market expectations of 9.5 billion yuan. Other revenue, including e-commerce, reached 3.54 billion yuan, a year-on-year increase of 37%, in line with expectations.

In terms of regions, domestic revenue reached 27.3 billion yuan, a year-on-year increase of 19%, while overseas revenue reached 650 million yuan, a year-on-year increase of 244%, exceeding expectations of 520 million yuan.

Profit

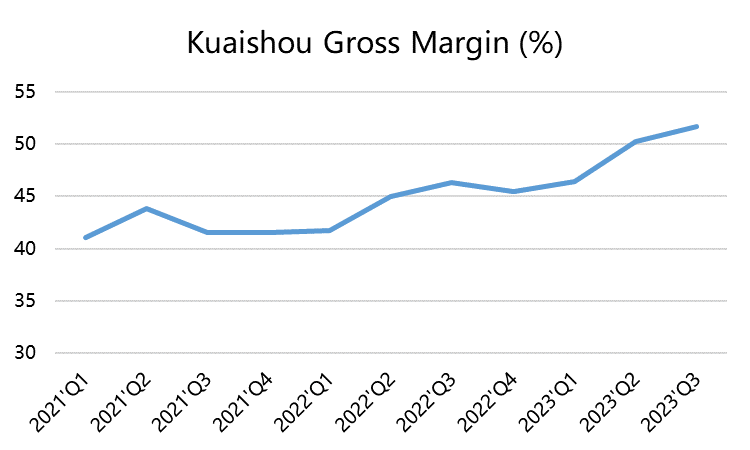

Gross profit margin reached a new historical high of 51.71%, exceeding expectations by 1 percentage point. This is mainly due to high-margin advertising and fast business growth, as well as cost reductions in revenue sharing and bandwidth.

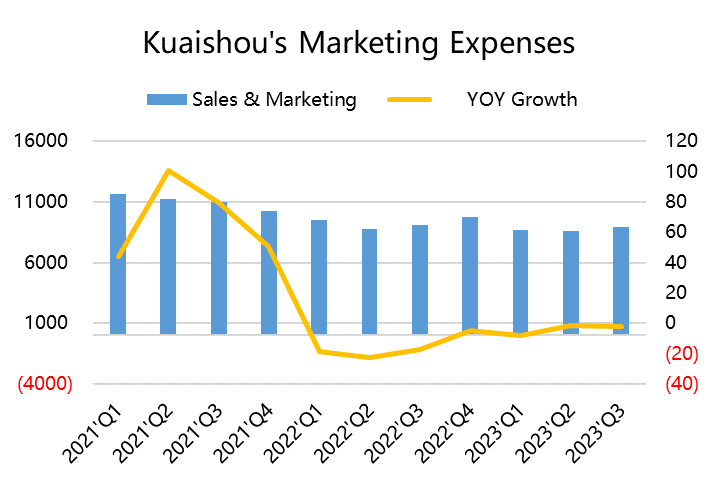

Operating expenses continued to decline, with a 2% decrease in marketing expense ratio, a 16% decrease in research and development expenses, and a 15% decrease in general administrative expenses.

Net profit for the period reached 2.18 billion yuan, and adjusted net profit reached 11.4%.

Adjusted EBITDA reached 4.98 billion yuan, exceeding market expectations of 3.98 billion yuan, and the EBITDA profit margin reached a new historical high of 17.8%.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Very comprehensive and helpful analysis, and I like the orange subtitles of your passage, it makes the reading clearer and more comfortable.