Will Meituan plunge again after Q3 Earnings?

$MEITUAN-W(03690)$ announced its Q3 earnings after Oct. 28. How compete and survive together with Douyin will become the main investment theme for the next few quarters.

Investment highlights

Meituan's Q3 performance is mainly reflected in the conflicting business sectors. In the post-"stay-at-home" era, the delivery and grocery business segments have been weak, while the offline dining and transportation businesses have shown growth.

Delivery has become increasingly stable, with a steady increase in profit margin, but it may be lacking in highlights. The opening of the offline economy will inevitably have a certain impact on online delivery. Although the delivery business grew by 14% YoY this quarter, it was lower than the instant delivery and distribution, which grew by 23% YoY. Moreover, the growth mainly relied on the frequency and scale of purchases by "medium-to-high frequency users," in other words, it relied more on "sticky old users." This makes lowering subsidies to improve profit margin more effective. Since Q2, the growth rate of delivery orders has no longer had a clear advantage compared to the overall market, indicating that the delivery industry is also becoming stable. At the same time, this has also led to increased competition among food and beverage merchants, resulting in Meituan benefiting from their profits.

Offline dining business is still growing strongly but has been largely affected by Douyin (Chinese Tik Tok). The commission rate has recovered the fastest this year, with transaction volume growing by 90% YoY and revenue growing by 30% YoY. Although it is not as high as the 47% growth in Q2, this growth rate is still strong because the base of Q3 2022 was higher (reached a higher level). We believe that one very important factor is the competition among food and beverage merchants (various new brands competing for market share). On the other hand, the transportation business has also made a strong recovery and contributed to Meituan's higher-profit revenue. At the same time, the fierce competition among offline merchants has increased advertising revenue, with a YoY growth rate of 31%, exceeding commissions. This at least proves that investments have yielded results.

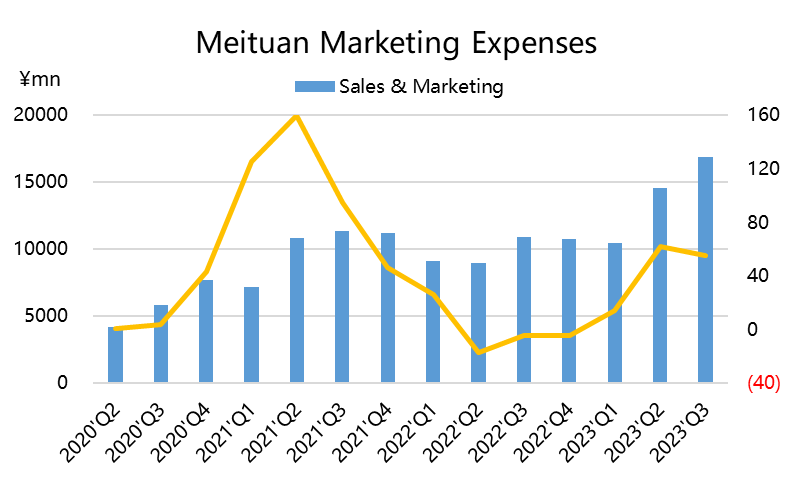

But how efficient are these results? The marketing expense ratio has grown by more than 55%, and the proportion of marketing expenses has risen again to 22.1%. As a result, the operating profit margin of core businesses (including offline dining and delivery) has decreased from 22.5% last year to 17.5%, mainly due to subsidies for offline dining business, which exceeded investor expectations. In principle, if the delivery profit margin exceeds expectations and the hotel business explodes unexpectedly, it can significantly increase profit margins. However, it still cannot make up for the losses in the offline dining business. Therefore, investors can consider that currently, income is insufficient to cover expenses.

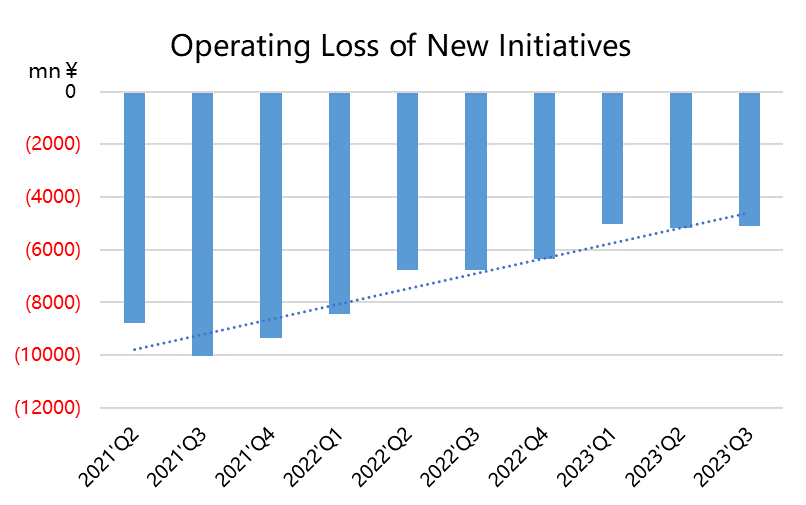

The performance of new business growth and loss reduction was below expectations, with a year-on-year growth rate of only 15% and an operating loss rate increasing from 23% in Q2 to 27%. Obviously, Meituan wants to focus more on operational efficiency.

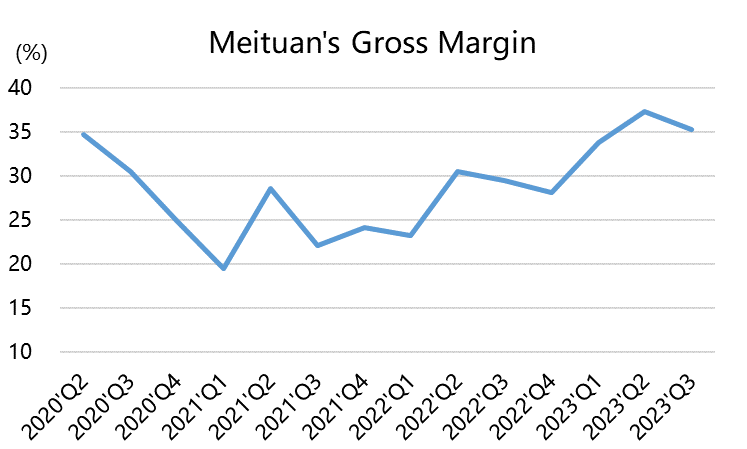

Although the profit margin has indeed increased, uncertainty can still scare away investors. Although net profit growth has exceeded 200%, it also includes the impact of depreciation and amortization, financial income and expenses, profits from joint ventures, and fair value changes in other financial investments. Adjusted net profit increased by 62% year-on-year, adjusted EBITDA increased by 29% year-on-year, and the main advantage is still the increase in gross profit margin (from 29.6% to 35.3%).

However, given the competition and subsidy model, investors have reason to doubt that this profit margin will continue to decline. Of course, the management was pessimistic about the profit margin guidance in Q2, so the entire quarter Meituan's stock price was not strong.

Currently, there may be some pressure on the demand side in Q4, especially for tourism and in-store businesses, and ByteDance's recent abandonment of games to focus on in-store businesses has also put great pressure on Meituan. Although Meituan's valuation is relatively low, it is still difficult to recover to an optimistic level.

Q3 Earnings Rerview

Revenue Side

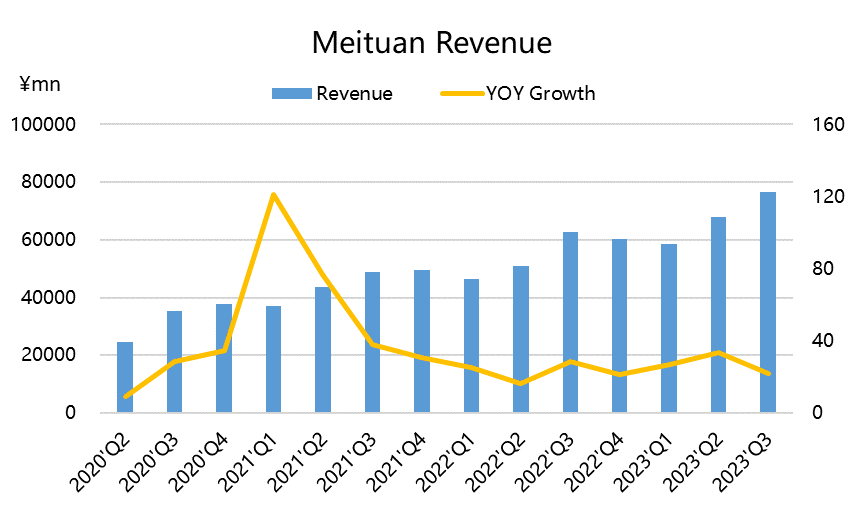

Overall revenue reached 76.5 billion yuan, a year-on-year increase of 22.1%, slightly higher than the market's expected 76 billion yuan;

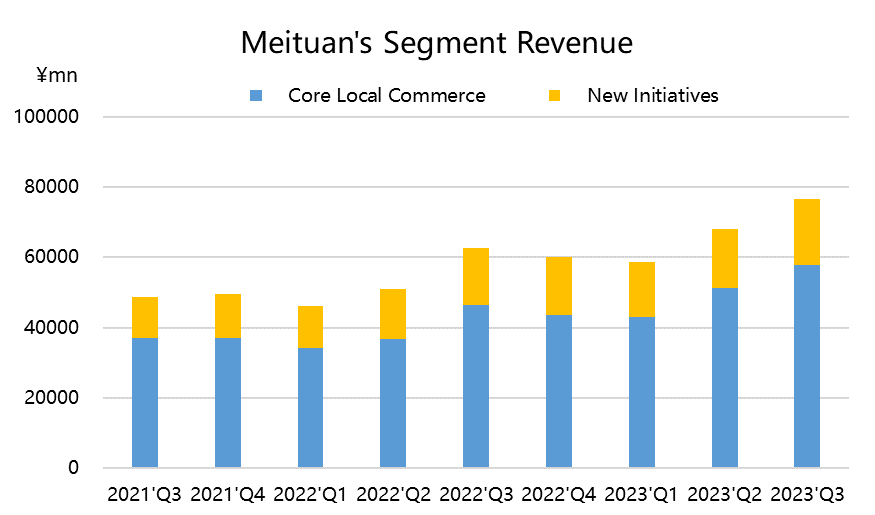

Among them, core local commercial revenue was 57.7 billion yuan, a year-on-year increase of 24.5%, higher than the market's expected 56.8 billion yuan; innovative business revenue was 18.8 billion yuan, a year-on-year increase of 15%, lower than the market's expected 19.2 billion yuan.

From another perspective,

Takeaway revenue was 23 billion yuan, a year-on-year increase of 14.3%, lower than the market's expected 23.4 billion yuan;

Commission revenue was 20.9 billion yuan, a year-on-year increase of 30.5%, higher than the market's expected 19.4 billion yuan;

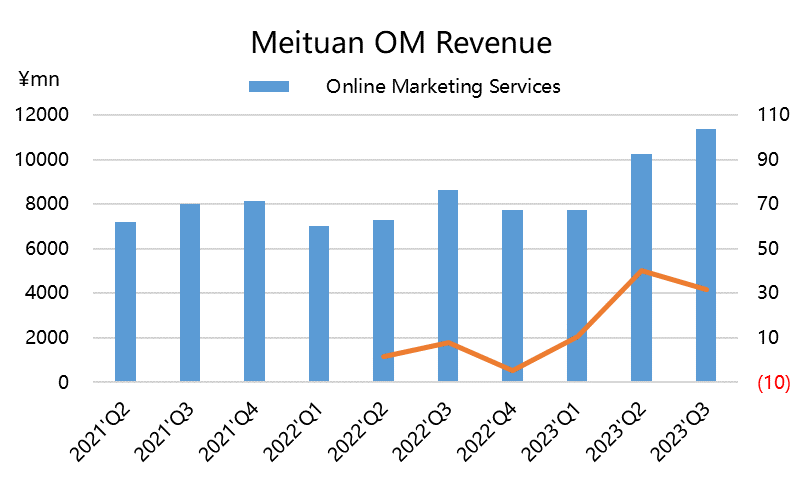

Online marketing service revenue was 11.4 billion yuan, a year-on-year increase of 31.6%, higher than the market's expected 10.7 billion yuan;

Other service revenue was 2.15 billion yuan, a year-on-year increase of 43.1%, basically in line with the market's expected 2.13 billion yuan.

Profit Side

Gross profit margin reached 35.3%, higher than the market's expected 33.5%.

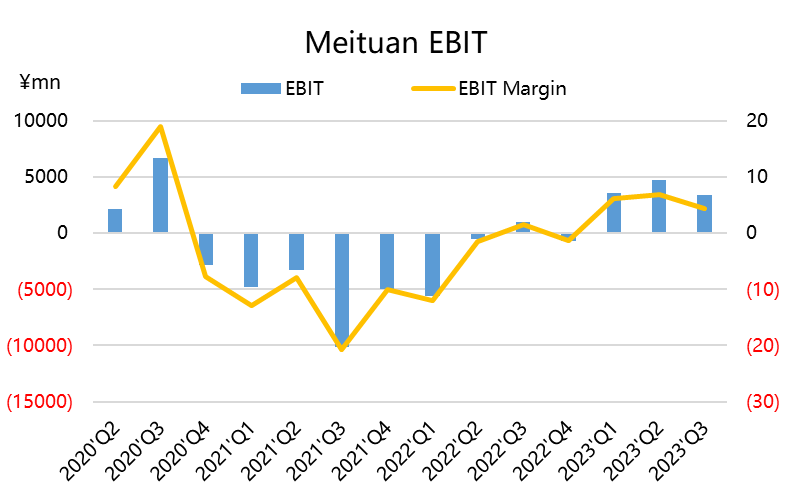

Earnings before interest and taxes (EBIT) were 3.36 billion yuan, a year-on-year increase of 2 times, higher than the market's expected 3.16 billion yuan;

Adjusted EBITDA was 6.19 billion yuan, lower than the market's expected 7.13 billion yuan.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

I don't think it's a good opportunity to invest in this stock

Your analysis of its fundamentals is very helpful to me!

03690The competition we face now is not small.

I hope Meituan can continue to surprise us

Meituan’s current fundamentals are really good.