What Makes Salesforce Magnificant 7+?

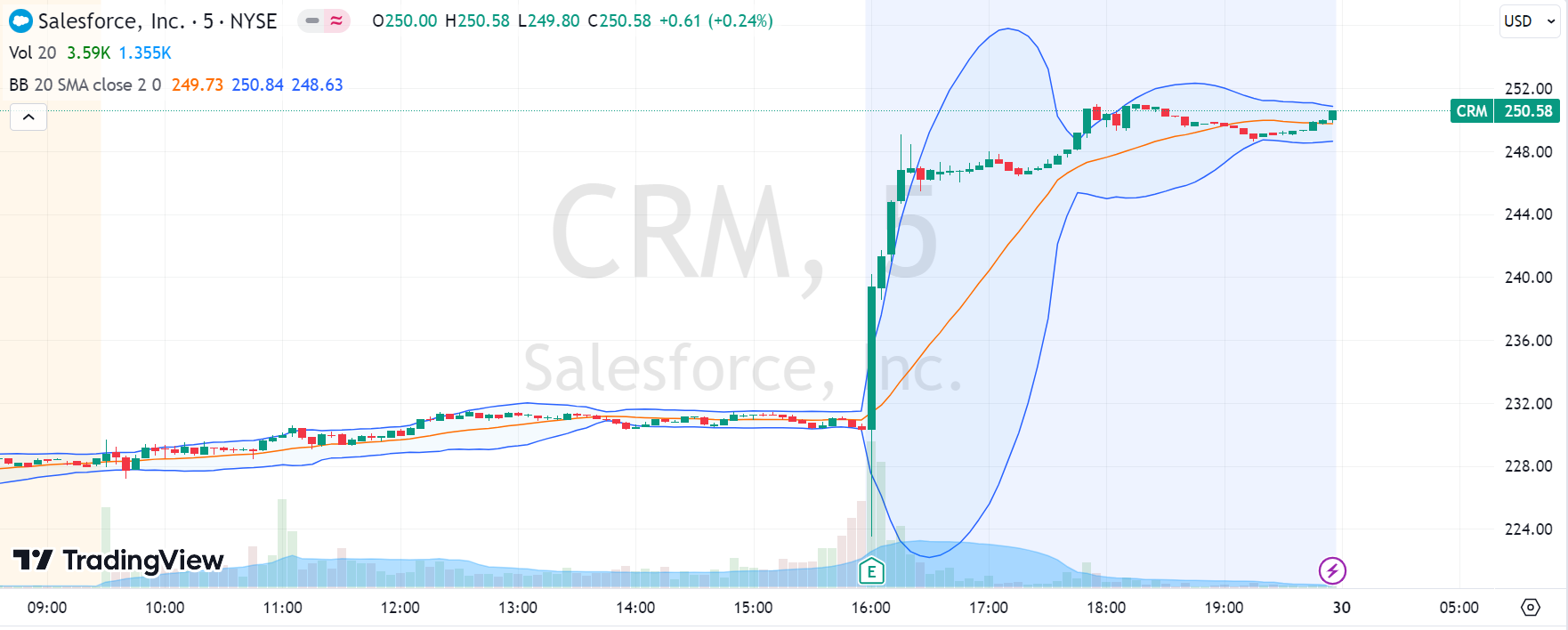

$Salesforce.com(CRM)$ announced its Q3 earnings report for the 2024 fiscal year ending on October 31, 2023. As the market had already raised revenue expectations, this quarter's performance was almost in line with market expectations. However, the company still raised guidance for the next quarter, causing the stock price to rise by 11%+ after hours.

In fact, CRM's stock has risen nearly 100% this year, making it one of the top performers among the Magnificent 7 and also one of the best performers in the S&P 500. The stock's jump this year is mainly due to better-than-expected performance and guidance, making it the leading software company in the AI market.

Investment highlights

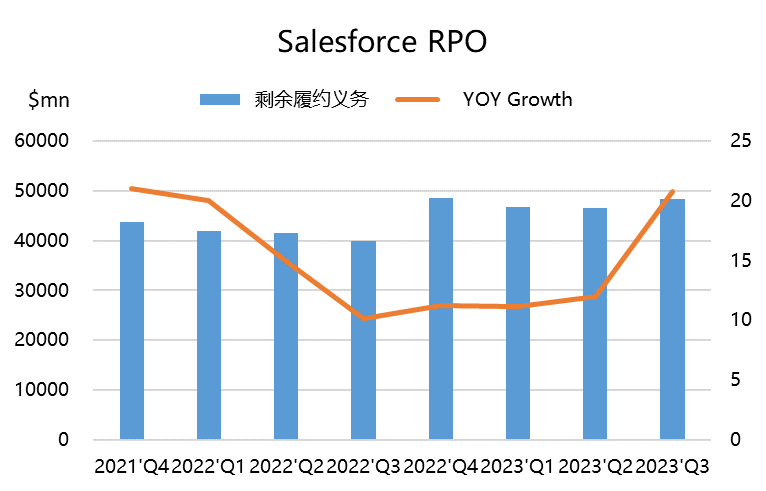

Several companies' earnings reports showing that the macroeconomic environment is not pessimistic, and that commercial activities related to AI still have growth potential. The company's several leading indicators are still excellent, with cRPO exceeding expectations and deferred revenue remaining stable, both maintaining double-digit year-over-year growth rates that exceed revenue growth, indicating that order growth is still relatively stable.

At the same time, the company's previous price increase benefits were not offset by price-sensitive customers, and large companies still maintain stickiness. AI-driven office suites can further strengthen the company's product ecology and improve future cash flow levels.

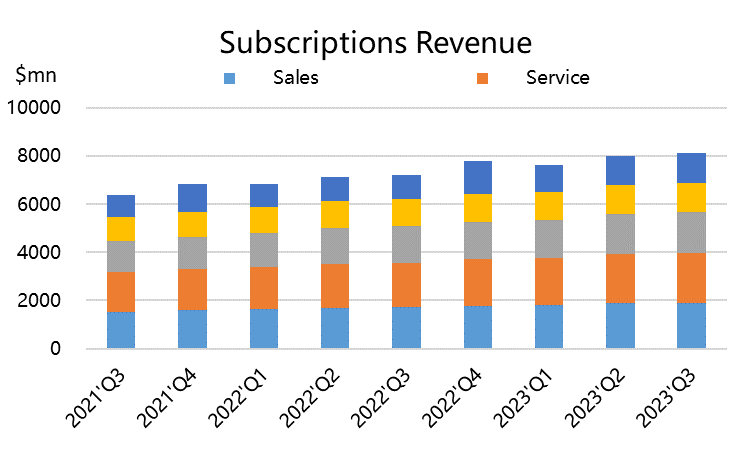

In addition, the performance of acquired businesses, including Tableau and Slack, is also a focus of investor attention. Although they can continue to help customers like Rubrik, Canara Bank, and the US Navy view and understand their data and make data-driven decisions, they still face some business closures and other issues. Moreover, $Microsoft(MSFT)$ Power BI has increased its market share due to AI infiltration, which has had a certain impact on Tableau.

In addition, after aggressive investor Elliot entered the game, the company paid special attention to operational efficiency, and its profit margin continued to soar, with an improvement in full-year profit margin guidance.

For valuation, comparing market-to-earnings ratios based on direct GAAP profits is not appropriate because depreciation and restructuring costs are unlikely to have a negative impact on the company. Therefore, when valuing the company, EBITDA multiples should be considered.

Currently, TTM and 24 expected valuations are both below the industry average, indicating room for growth. The average EV/EBITDA (TTM) of the top 10 companies in the industry is 34 times, expected to be 25 times in 2023 and 22 times in 2024.

Expected EBITDA for 2024 will reach $14.7 billion. Discounted at an average WACC of 10.5% and calculated at an EV/EBITDA multiple of 22 times, its per-share value can reach $297, still with 18% room for growth.

Earnings Review

Revenues

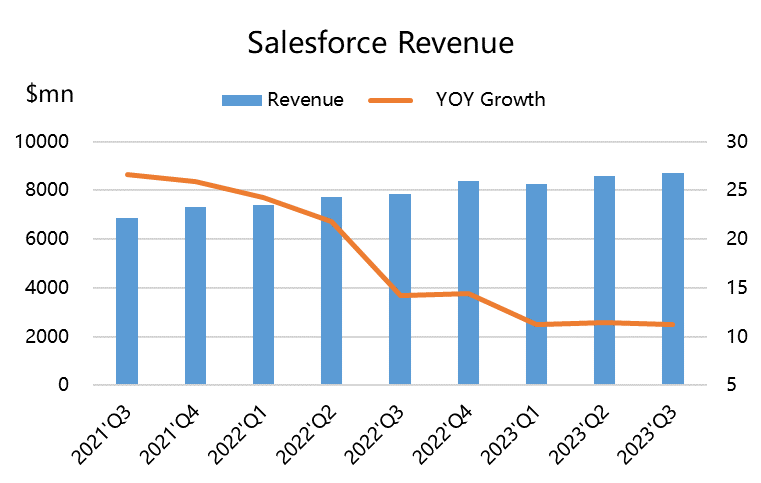

Revenue reached $8.72 billion, almost in line with expected $8.71 billion, a year-over-year increase of 11%, which is also a 10% increase when calculated at a constant exchange rate.

Subscription and support revenue was $8.14 billion, higher than expected $7.91 billion, a year-over-year increase of 12.5%. Professional services and other revenue were $600 million, a year-over-year decrease of 4%.

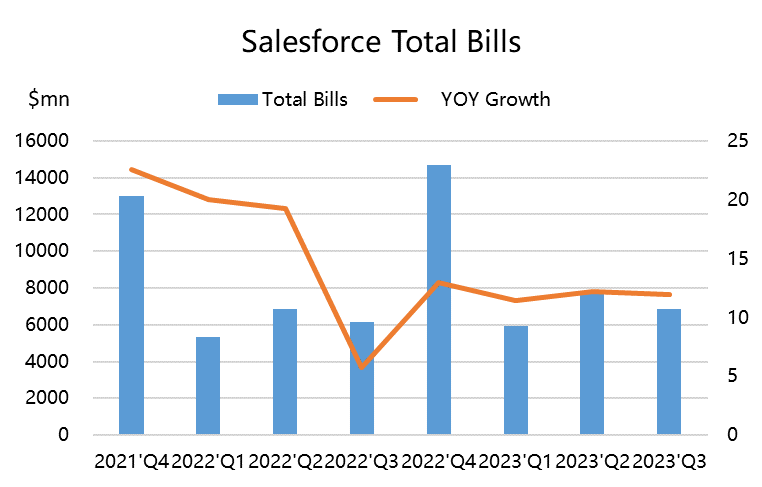

Remaining contractual obligations amount to $48.3 billion, higher than the expected $44.9 billion, a YoY increase of 21%; current remaining contractual obligations reach $23.9 billion, higher than the market expectation of $23.1 billion, a YoY growth of 14%.

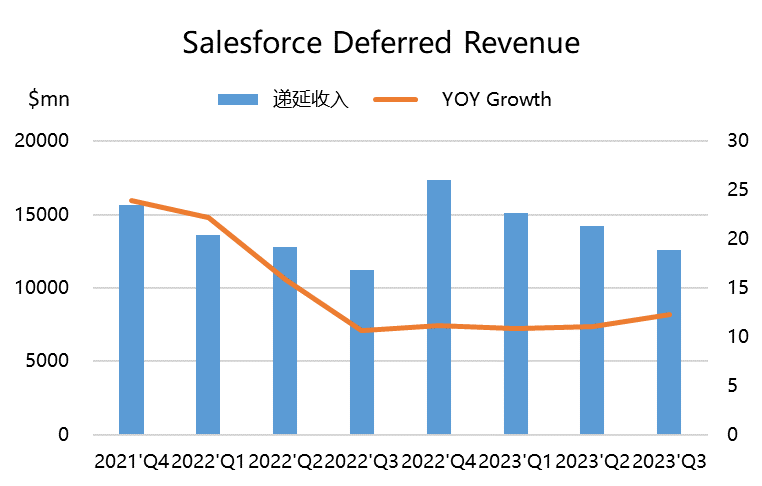

Deferred revenue is $12.56 billion, a YoY increase of 12%, with an expectation of $12.77 billion.

Profit

Gross margin is 79.35%, higher than the expected 78.5%;

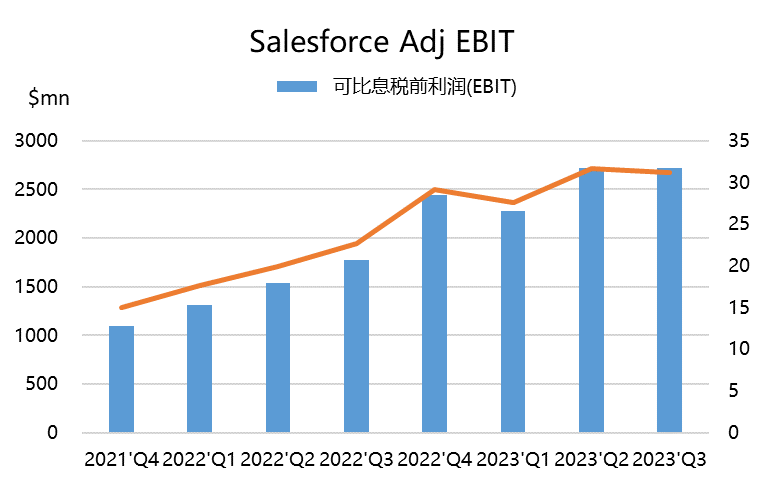

EBIT is $2.71 billion, non-GAAP operating profit margin is 31.6%. Restructuring has negatively impacted GAAP operating profit margin by 60 basis points in Q2.

Non-GAAP diluted EPS is $2.11, while the expectation is $2.06.

In terms of guidance,

The company expects revenue for FY24Q4 to be $9.18 to $9.23 billion, with a market expectation of $9.22 billion. Adjusted EPS is projected to be $2.25-2.26, with an expectation of $2.18.

FY24 full-year revenue is maintained at $34.75 to $34.8 billion, a YoY growth of 11%. Non-GAAP operating profit margin is once again raised to approximately 30.0%.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Salesforce’s fundamentals are pretty good right now.

CRM’s performance this year is really strong

Let's see if this stock can continue to surprise

Salesforce is always worthy of our trust

An increase of 11%, which is really great.