FedEx's plunge means weaker demand, or competition?

$FedEx(FDX)$ plunged nearly 10% after hours due to its Q2 earnings report ending on November 30th, which fell short of expectations and lowered guidance for the next quarter. As investors look to the performance of logistics companies to gauge the global macroeconomic environment, particularly the level of commercial activity, this could also become an important indicator.

The company's downward revision also suggests that consumer spending during the year-end holiday period (from Thanksgiving to Christmas and New Year) may not be as strong as anticipated. However, does the company itself encounter urgent issues that need to be addressed?

Image

Investment Highlights

1. The company's poor performance is attributed to insufficient demand. Not only did the Q2 performance up to the end of November fall short, but it also lowered the overall expectations for 2024, indicating an "economic contraction." With FedEx's revenue declining for the past 5 quarters and the volume of shipments decreasing for 9 consecutive quarters, there is indeed a trend of "cost-cutting" in logistics.

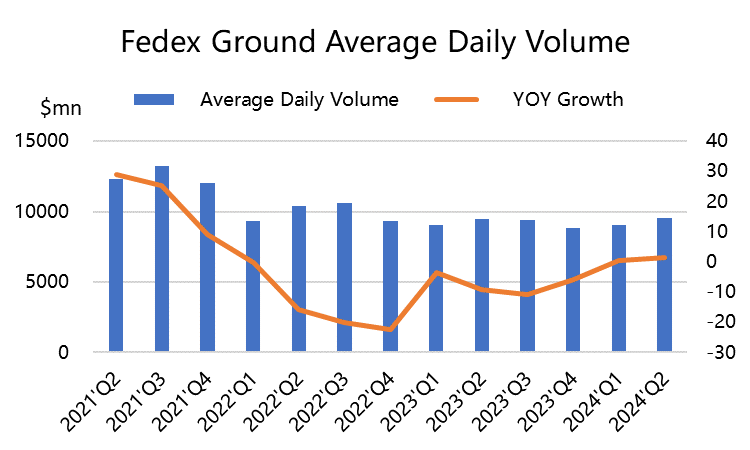

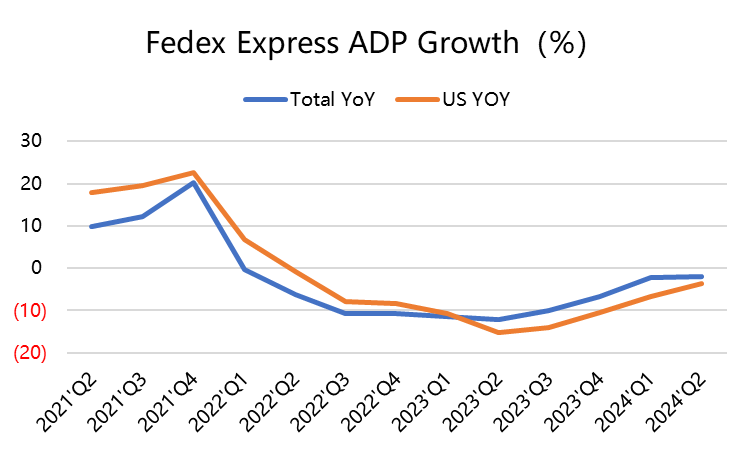

2. Consumers are shifting from express delivery to more cost-effective ground. The company's express delivery volume is declining, and air shipments have been declining year-on-year since mid-2022, while ground transportation volume has stabilized over the past two quarters. Consumers are to some extent reducing unnecessary "high-cost" transportation and turning to lower-priced shipping methods. However, from a macro perspective, continuous inflation has indeed posed a problem of rising living costs for consumers, but actual consumer spending has not decreased.

3. Intense competition among peers, FedEx may be losing market share. According to third-party data reports, online consumer spending during the 2023 "Black Friday" shopping season increased by 6% year-on-year, which is still a very strong growth in the context of inflation. $Amazon.com(AMZN)$ itself has a strong logistics system and holds an advantage in "last-mile" delivery services, while the emerging low-cost e-commerce platform Temu $Pinduoduo Inc.(PDD)$ has also rapidly gained market share and popularity due to its low prices.

Among Temu's main cooperative delivery service providers is FedEx, but $United Parcel Service Inc(UPS)$ has a larger shipment volume, which may also contribute to FedEx's declining market share.

From this quarter's financial report, the daily average volume of international express delivery decreased by -0.61%, much lower than the domestic volume in the U.S. (-3.52%) and the overall volume (-2.02%), but the number of low-priced shipments has significantly increased, thereby reducing the unit price. In addition, the volume of local international business recorded a year-on-year growth of over 5%, indicating a recovery in demand for international express delivery.

Performance Overview

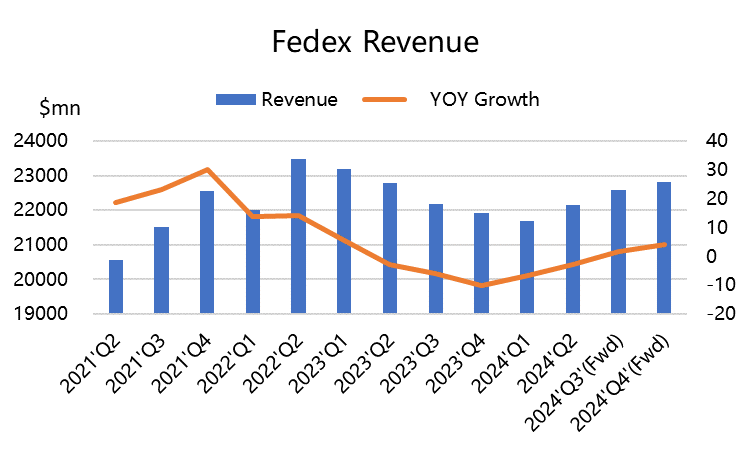

Revenue was $22.2 billion, a 2.6% year-on-year decrease, lower than the market's expectation of $22.4 billion.

The adjusted operating profit is $1.42 billion, lower than the market's expected $1.49 billion, and also lower than the same period last year of $1.21 billion. The operating profit margin is 6.4%, higher than last year's 5.3%. The increase in operating profit margin is mainly due to the execution of the company's DRIVE plan and continued focus on service and revenue quality.

In the three major business segments, FedEx Ground's revenue and profit have increased, mainly due to improved earnings, reduced costs, and increased volume. The cost per package has decreased by 2%, mainly due to lower linehaul costs and improved first and last mile productivity.

FedEx Freight's revenue decreased by 3.8% due to a decrease in freight volume, but operating profit increased, mainly due to cost reduction and improved operational efficiency.

Meanwhile, the most important FedEx Express operating income has significantly decreased (-5.6%), returning to the level of the second half of 2020. The decline in revenue is due to a decrease in shipment volume, reduced fuel surcharges, reduced demand surcharges, and a shift to lower-yield services.

Looking ahead, the company expects a single-digit percentage decrease in revenue for the 2024 fiscal year, with earnings per share of $17.00 to $18.50, lower than the market's expected $18.22.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.