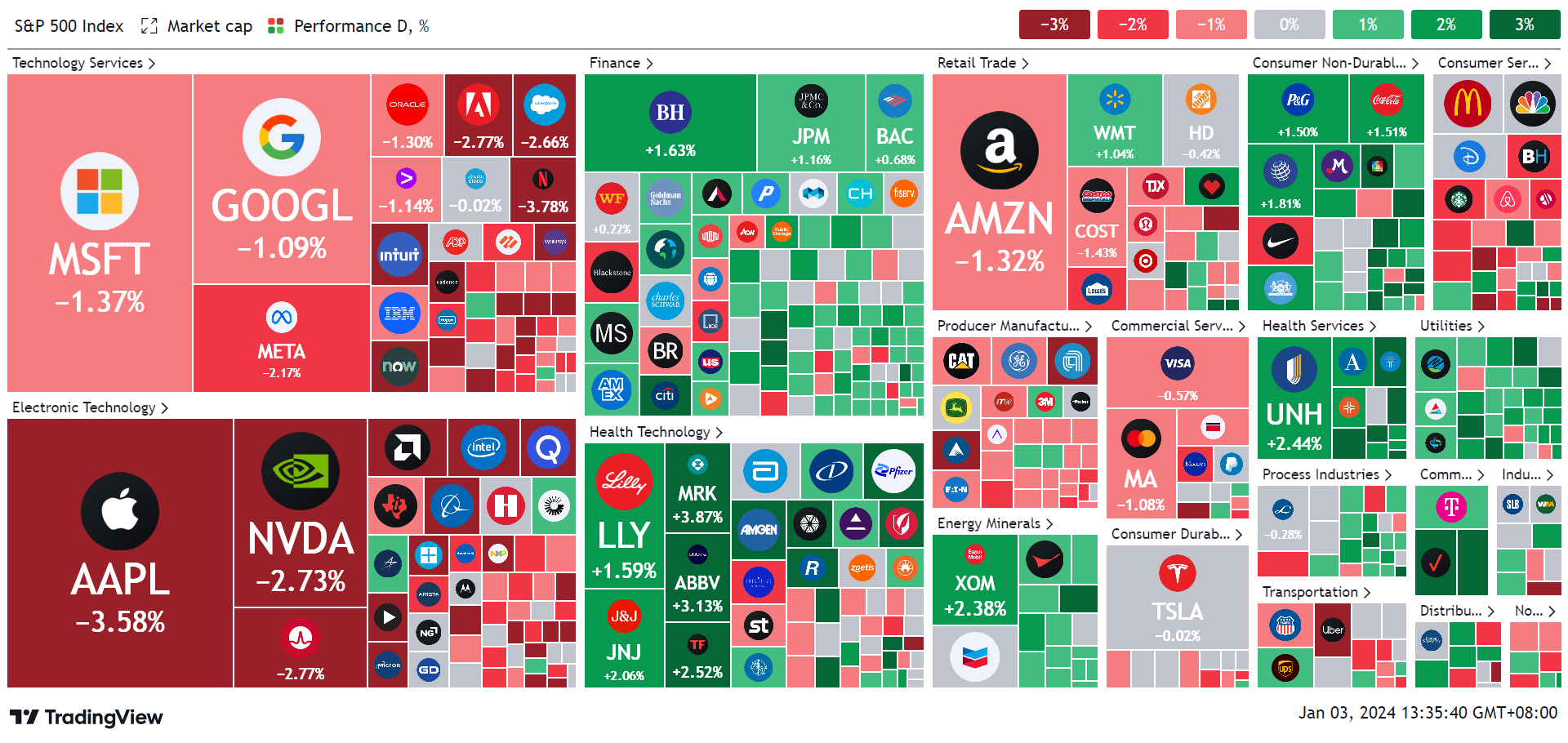

Some neglectable changes in 2024, starting from Apple

In the first trading day of 2024, technology companies experienced a sharp pullback, leading to a significant decline in the $NASDAQ(.IXIC)$ and a clear sector differentiation.

$Apple(AAPL)$ in particular saw a 3.58% pullback, with no fundamental changes. $Barclays PLC(BCS)$ downgraded Apple from "overweight" to "equal weight," lowering the TP tp 160. They hold a pessimistic view on the sales performance of the iPhone 15 and have low expectations for the iPhone 16.

Since its release in September, the iPhone 15 sales have been underwhelming, but it still performed strongly during the upcoming shopping festivals. While overall sales may not be surprising, this year's price increase may lead to higher profit margins. Additionally, TSMC's 3nm capacity is mainly dedicated to Apple, maintaining a leading position in terms of chips.

As for the iPhone 16, there are rumors of unexpected changes, particularly significant changes in the optical lens, with related information already present in the upstream supply chain. Demand-wise, it will depend on the overall macroeconomic situation. However, the cyclicality of tech products is not strong.

Therefore, is it likely that the market sold off the largest weighted stocks due to this repetitive information?

Unlikely. I believe there are three more important reasons:

1. Tax Loss Harvesting: In 2023, large tech stocks were overall very strong, so fund managers are more likely to close out losing positions at the end of December, while retaining or increasing holdings in high-yielding large tech stocks to defer capital gains tax to future years.

2. Window Dressing: To showcase strong holdings of large tech companies in the quarterly report (or to adjust to the target position as required by IPS), over-allocated large tech stocks at the end of December will be sold off due to excessive risk exposure.

3. Crowded Trades: With the development of quantitative and algorithmic trading, the consistency of trading trends has increased, resulting in an accumulation of positions in continuously profitable stocks and amplifying market buying and selling rhythms. This convergence of effective factors in the stock market has led to a "crowded trade" phenomenon similar to foreign exchange and futures trading. This is particularly evident during downturns (because nobody wants to fall behind).

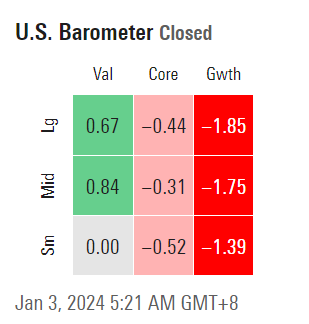

In this scenario, a shift in style is an inevitable result. The change in Morningstar's market style table on January 3rd is particularly noticeable, with overall pullback in growth stocks and capital inflows into value stocks.

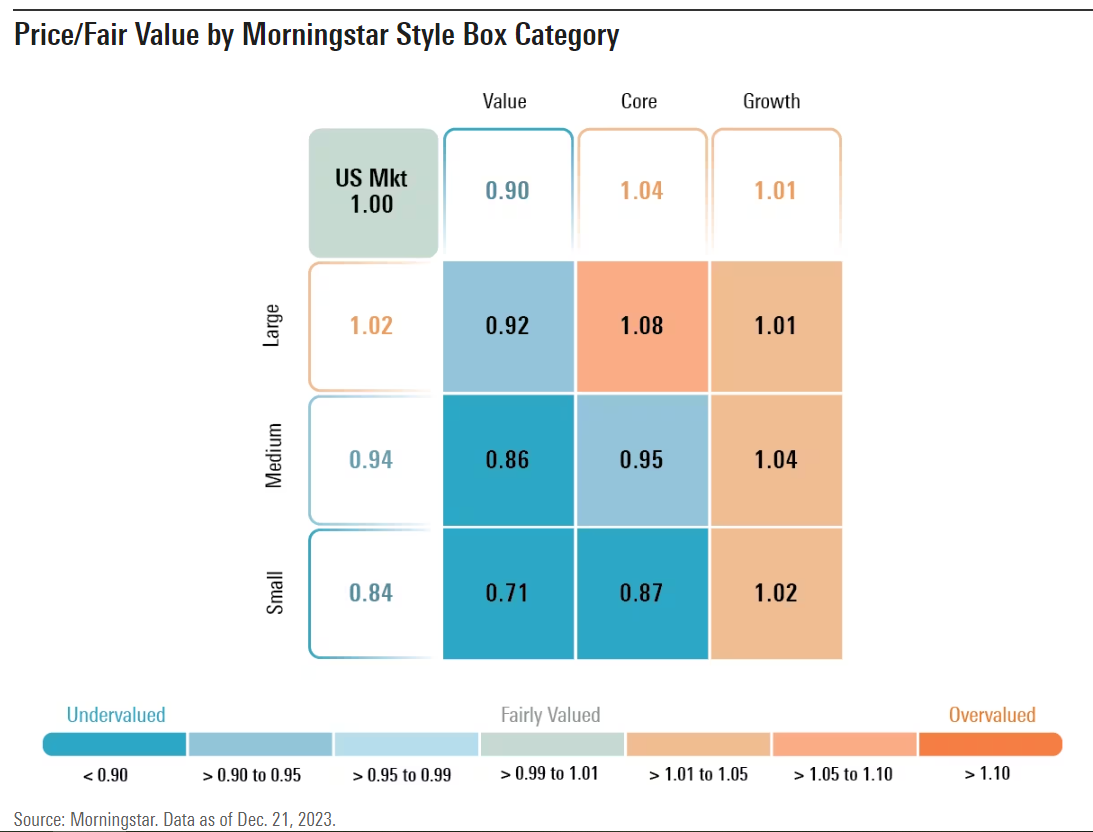

From a valuation perspective, as of the end of December 2023, due to market expectations of a slowing economic growth rate and the stock market approaching high levels, several overvalued sectors may be constrained, but undervalued sectors can provide relatively large safety margins as a result.

In terms of market capitalization, small-cap stocks remain the most attractive, with a 16% discount, followed by mid-cap stocks at a 6% discount, while large-cap stocks are slightly above fair value.

In terms of types of stocks, value stocks remain the most attractive, with a 10% discount, while core stocks have already entered overvaluation, and growth stocks are basically at fair value.

Among the "Big Seven," except for $Alphabet(GOOG)$ , which is still undervalued, the others are already above fair value. Apple (AAPL) is the most overvalued, so more selling trades occur in Apple during pullbacks.

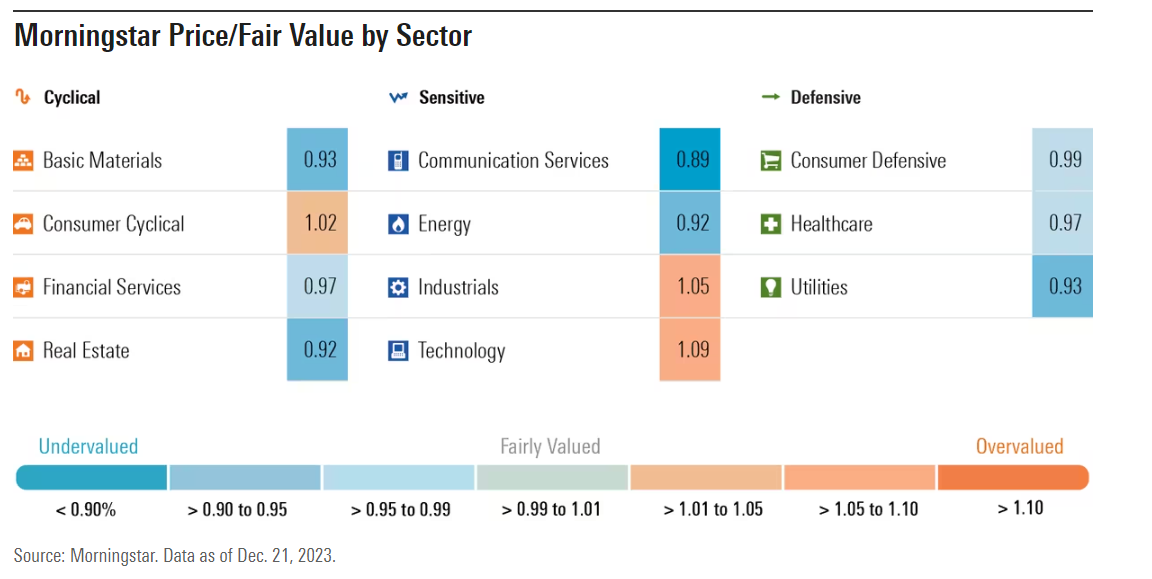

Looking at sectors

1. The technology industry was the third most undervalued industry at the beginning of 2023. After a year, it rebounded to fair value, and after a pullback, it rebounded to overvaluation. This mainly stems from upward performance and accelerated stock price growth.

2. Consumer discretionary stocks were the second most undervalued sector in 2023 and are now fully valued. There has been performance recovery, but stock price recovery has remained flat.

3. The industrial sector has entered overvaluation. The real estate industry performed strongly in the fourth quarter, but its value remains severely undervalued.

4. The most undervalued industry is still communication. It has been the most undervalued industry since 2023, and even considering its above-market returns, its value remains underestimated.

5. With the drop in oil prices, the energy sector has become the most highly valued sector; the utilities sector sharply declined as interest rates rose and is now undervalued.

For 2024, undervalued assets, especially small-cap value stocks, may have opportunities to stand out. The financial industry, including banks, is attractive due to its strong cyclical nature during interest rate cuts. In industries sensitive to economic data, communication services still remain attractive. Additionally, healthcare and utilities will provide strong support during market pullbacks due to their strong defensive nature.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.