Big-Techs' Dip: Why Google Still Cheap?

$Alphabet(GOOGL)$ in my opinion, is a company with low risk, stable performance, excellent asset quality, and the ability to benefit from both inflation and interest rate cuts among major tech companies. In 2024, although Google's revenue growth may be slow, the expected profit growth will be higher, and it is also poised to gain a higher market position in the field of AI. $Alphabet(GOOGL)$

Investment Highlights

- Google's advertising business has been growing steadily for a long time. In the potential structural adjustments in 2024, it is expected to achieve higher operational efficiency, thereby improving its profitability.

- Its dominant position in the advertising field enables it to benefit from the interest rate cuts in 2024.

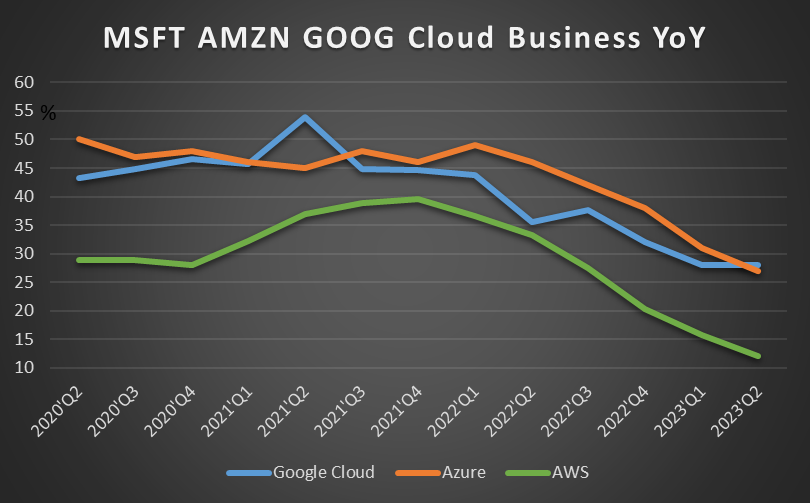

- Despite competition in cloud computing and artificial intelligence, Google Cloud's growth rate has been on par with Microsoft (MSFT) and $Amazon.com(AMZN)$

- With most tech companies completing cost-cutting measures, it is expected that the growth rate of cloud business spending will return.

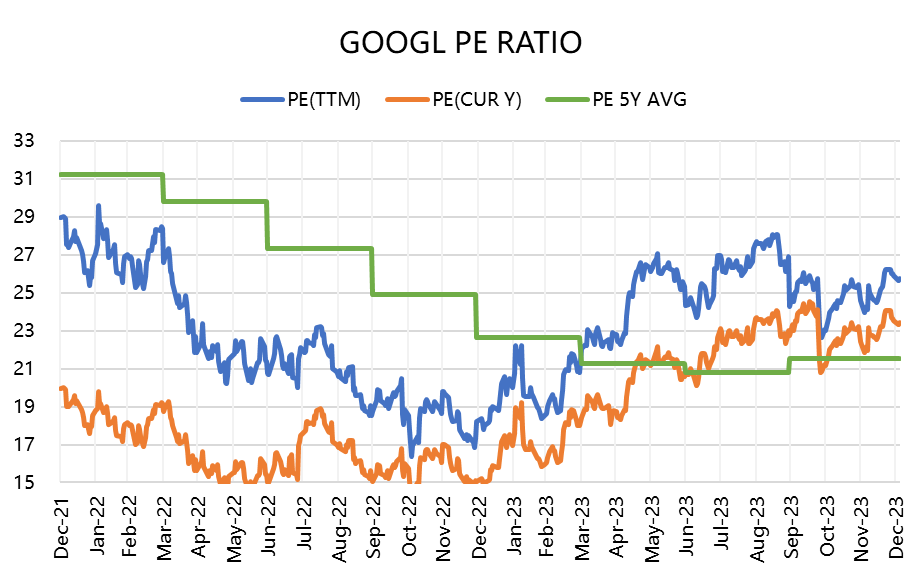

- The current TTM PE valuation is 26 times, lower than Microsoft and Apple, but Google has higher profit growth expectations and more attractive EBITDA multiples.

Major business Change in 2024

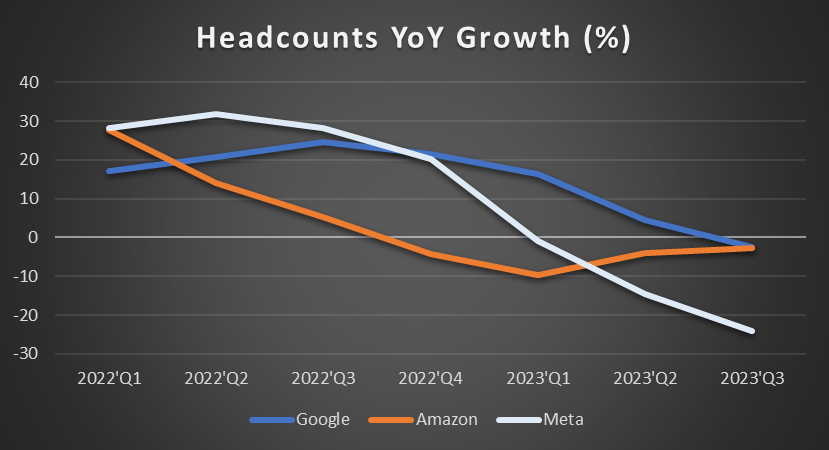

Previously, Sean Donahoe, head of ad sales for major US customers, revealed that Google's ad sales team is undergoing restructuring. Although he did not mention any layoffs, there have been rumors in the market that as many as 30,000 positions may be cut. Although this may not happen quickly, operational reforms brought about by the restructuring are inevitable.

In comparison, Google cut around 12,000 jobs in 2023, while $Meta Platforms, Inc.(META)$ and Amazon (AMZN) had a higher proportion of layoffs.

2024 will be another year for Google to pave the way for the upcoming AI-based thorough restructuring.

As for why they are targeting the advertising business? I believe that the integration of AI and automation technology is crucial. In other words, AI will first become a tool to improve Google's operational efficiency.

AI is increasingly used to test ad copy variants, provide keyword suggestions, optimize visual elements, and provide engagement tools. It also helps to segment audiences more accurately for more precise ad targeting and to conduct predictive analysis to anticipate opportunities and challenges in ad campaigns. Meanwhile, the number of short video ads on YouTube Shorts will increase, and search will become more visual, with images and graphics becoming more common in search ads.

Specific AI integrations underway include the Google Search Generative Experience, which integrates generative AI into a smooth and user-friendly Google experience. The company also has a significant advantage in its AI efforts with data from 4 billion global users.

AI Means A Lot to Google

Gemini, which was recently launched, is a new series of large-scale language models that are expected to enhance the application experience similar to Google search generation. Google AI is also being added to operating systems, which may drive revenue from new areas such as chatbots, co-pilots, and APIs.

Google owns the Android operating system, Gmail, Chrome web browser, Google Classroom, navigation platforms like Maps and Waze, as well as Google Photos. It also ventures into the hardware field with products like Pixel smartphones, Nest smart home product line, Chromebook, and the streaming device Chromecast.

The company is also involved in some more forward-looking projects such as autonomous driving (Waymo), quantum computing (Sycamore), smart cities (Sidewalk Labs), and even healthcare artificial intelligence, taking ethical considerations of artificial intelligence seriously in its expansion.

One area of significant investment for GOOGL is artificial intelligence ("AI") and machine learning ("ML"). It aims to use this technology across the entire company, including search, cloud computing, and other fields. Some specific areas of focus include translation, computer vision, and natural language processing.

Two important moats - Chrome and YouTube

Google has many advantages. Its search engine holds a 90% market share in the search engine market. Even though Microsoft's Bing gained some users at one point due to loading ChatGPT's Copilot, it did not have a visible impact on Chrome. Google has at least five products that are leading in their categories and 9 products with over 1 billion users. The company also provides advertising through its targeted advertising technology across the Google network, including AdSense, AdMob, and Google Ad Manager. Through these programs, the company delivers ads based on the content of customer websites or apps, geographical location, and other factors. In 2022, the Google network generated $32.8 billion in revenue, reaching $23 billion in the first 9 months of 2023.

YouTube is the world's second most popular social media platform, with its premium ad-free service having 28 million subscribers. It generated $29.2 billion in revenue in 2022 and reached $22.3 billion in the first 9 months of 2023. Unlike other media platforms, it does not require substantial investment in content but operates on a revenue-sharing model with content creators. As of the latest reported data in 2022, YouTube Music and Premium subscription users have exceeded 80 million.

Previously, short video creators on YouTube could not earn money from video production as they could with long videos. Starting in 2023, GOOGL began sharing 45% of ad revenue with creators in the Partner Program to incentivize them to create content for YouTube Shorts and compete in the TikTok market. Therefore, as long as the entire YouTube community performs better, creators can earn more money.

The income of creators will determine the platform, which may be overlooked by some domestic platforms. $哔哩哔哩(BILI)$

So far, YouTube Shorts seems to be doing well. The latest quarterly report shows that short videos had an average of 70 billion daily views in October, and the company is working to bridge the monetization gap between long and short videos.

Revenue and Profit Growth Outlook for 2024

The outlook for 2024 is that as the scale increases, it will face challenges in revenue opportunities, but with improved efficiency, the company's profit margin is expected to grow.

Over the past 12 months, Google has had a gross profit margin of 56%, an EBIT margin of 27%, a net profit margin of 22%, and a return on equity of 25%. These are among the highest gross profit margins and return on equity found in large tech companies.

At the current price, the TTM P/E ratios for $Microsoft(MSFT)$ $Apple(AAPL)$ are 35.5 and 30 times, respectively, while Google's P/E ratio is 26 times.

At the same time, the expected EBITDA for 2024 is 11.5 times, and after excluding about $4.5 billion in losses from other investment areas, the core business trades at only 11.2 times EBITDA. The current consensus expectation for 2025 EBITDA is $158.3 billion, at 10.2 times.

While Google is not a value investment target, it seems to be the cheapest among its peers, with comparable gross profit margins and much better growth than Apple.

The biggest risk is the U.S. Department of Justice's case against the company, accusing it of monopolistic practices and illegal use of power for its own gain. If found guilty, it could face huge fines, changes in business practices, and damage to its brand reputation. Europe is also likely to launch similar cases. Legal risks have always been one of the most difficult risks to quantify. At the end of 2023, it reached a $391.5 million settlement with 40 states related to tracking personal data.

For investors looking to buy low, these "will eventually be resolved" antitrust cases may present long-term opportunities for intervention.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- moobug·2024-01-08great reading.LikeReport