Two Neglectable Advantages for Meta in 2024!

After the iOS privacy policy change in 2022, $Meta Platforms, Inc.(META)$ was temporarily abandoned by investors, but its strong user technology helped it to recover quickly. With ongoing improvements in monetization, as well as continued efforts in Reels and WhatsApp, Meta's stock price has reached new highs.

The current consensus price target for the market is $385, with companies that have recently updated their price targets all raising them to over $400, and some as high as $470.

Investment Highlights

- Stable user base, strengthening monetization of Reels, and potential market share growth for the Facebook shop.

- Two major opportunities in 2024: the demand for Chinese businesses (e-commerce, gaming) to go global, and advertising spending in the US election year.

- AI improving monetization efficiency, cost reduction and efficiency enhancement from layoffs have already increased profit margins, with the potential to better support valuation.

- The current 12-month PE ratio is 24.2 times, expected to decrease to around 20 times by 2024.

High user engagement and continued growth in the advertising business.

Key performance indicators show that Meta's family daily active users (DAU) continue to grow steadily. By Q3 2023, DAU reached 3.14 billion, and monthly active users (MAU) reached 3.96 billion, a 7% year-on-year increase. This growth trend is consistent with the previously observed year-on-year growth trend, maintaining a 7% growth rate in Q2 2023.

Therefore, the sustained growth of DAU indicates Meta's ability to retain its existing user base and steadily attract new users. This indicates that Meta's products continue to attract a large audience globally, consolidating its position as a major platform for social interaction and content consumption.

On the other hand, Meta's advertising ecosystem within its application family has seen a significant increase in ad impressions for several consecutive quarters. Ad impressions grew by 31% year-on-year in Q3, further continuing the growth rates of 34%, 26%, 23%, and 17% in the previous four quarters.

The growth in ad impressions indicates that users are spending more time on the platform, creating more opportunities for advertisers. Additionally, this also demonstrates the effectiveness of Meta's advertising strategy in attracting user attention and maintaining high levels of user activity.

In contrast to the growth in ad impressions, Meta has experienced a continuous decline in average ad prices during the quarter. In Q3 2023, average ad prices decreased by 6% year-on-year, compared to decreases of 16%, 17%, 22%, and 18% in the previous four quarters. Although the decline in average ad prices may initially seem concerning, it is logically aimed at attracting advertisers through cost-effective advertising solutions.

There is also an e-commerce opportunity within the product matrix. Instagram is the most popular social media app among Generation Z for shopping, surpassing TikTok and Google's YouTube. For millennials, Facebook and Instagram are the primary social networking tools, followed by YouTube, TikTok, and other social media apps.

This trend will continue, and the younger generation is more accustomed to shopping on social media. META is leveraging this trend and has started collaborating with e-commerce in the second half of 2023, launching new in-app shopping features. Users of Facebook and Instagram will be able to directly click on ads to make purchases.

This will increase Meta's monetization opportunities as the volume of ads from Amazon merchants increases, accelerating Meta's ability in-platform shopping. Meta is moving its shop sellers to its own checkout experience, while keeping processing fees unchanged.

At the same time, this will hardly increase costs, so while achieving revenue growth, it can also achieve an increase in profit margins.

Diversification of revenue beyond advertising

Meta's continued profitability is not limited to its core advertising platforms Facebook and Instagram. Its biggest growth points are actually in WhatsApp, Reels, and the recently established Threads, which will become long-term core value drivers for Meta.

Diversification of revenue beyond advertising channels demonstrates its ability to withstand risks and utilize various sources of income. Other revenue reached $293 million in Q3 2023, a 53% year-on-year growth, with substantial contributions from the WhatsApp Business platform. The significant growth in commercial message revenue on the WhatsApp Business platform indicates Meta's strategic monetization of various functionalities beyond traditional advertising methods.

From an international revenue perspective, the accelerated spending of Chinese advertising clients in the e-commerce vertical in the third quarter and the overall growth of advertising client regions reflect Meta's ability to attract advertising clients from different geographical markets. Business-friendly factors for advertising clients, such as lower shipping costs and relaxed regulatory requirements in the Chinese gaming industry, have also contributed to this growth.

In India, 60% of WhatsApp users interact with business application accounts every week, demonstrating the widespread use of commercial messages for business purposes. The revenue from ads clicked and sent from India has doubled year-on-year, confirming the revenue potential brought by commercial messages.

As of December 4, 2023, Threads has 141 million users, but the growth rate has significantly slowed in recent months.

Short video Reels drives engagement on Instagram and monetization for Meta

On the other hand, Reels has had a significant impact on user engagement on Instagram. Since its launch, the usage time of Reels on Instagram has grown by over 40%. The surge in user engagement indicates Meta's strategic progress in introducing practical content formats, making users more willing to spend more time on this feature. As a result, the popularity of Reels among users has increased Meta's monetization opportunities.

Furthermore, Reels has already reached a level of net neutrality in overall ad revenue for the company. This means that the revenue generated through Reels ads has balanced the investment and resources put into the development and maintenance of this feature.

Instagram has a competitive advantage in engagement, allowing it to charge higher fees, especially in advertising. The average cost per click for Instagram ads is as high as $3.56, while platforms like Facebook, Twitter, and $Pinterest, Inc.(PINS)$ $Snap Inc(SNAP)$ are below $2.

Meta's focus on advancing artificial intelligence technology is evident from its significant investments in AI-driven solutions and platforms to leverage monetization potential. The company utilizes AI in various aspects, including generative AI models (such as Llama 2) and recommendation AI systems, to support dynamic information feeds, Reels, advertising, and integrity systems.

AI's impact on user engagement and monetization capabilities

The end-of-year release of Llama 2 has already seen over 30 million downloads, representing Meta's leading position in large-scale development and deployment of advanced AI solutions. AI-driven feed recommendations have increased user engagement by 7% for Facebook and 6% for Instagram. This demonstrates the effectiveness of AI algorithms in curating personalized content for users, thereby enhancing their engagement on the Meta platform.

Furthermore, integrating AI tools for advertisers, such as the Advantage+ shopping ad series and Advantage+ creative tools, has yielded substantial results, including $100 billion in annual revenue from shopping ads and over half of advertisers using Advantage+ creative tools to optimize their ad images and text.

Meta's strategic focus on enhancing its products, particularly live experiences such as reels and click-to-message ads, reflects its emphasis on innovation and user engagement. The evolution of Reels from an early initiative to a core part of Instagram and Facebook signifies its integration into the platform's fundamental experience.

Finally, Meta is striving to improve the performance of Reels ads through ranking enhancements and increased interactivity, aiming to strike a balance between engagement and revenue growth.

Opportunities in the election year advertising

According to Magna's forecast, digital ad spending will continue to grow in 2024, with pure-play digital media spending expected to increase by 9.4%, indicating the advertising industry's reliance on digital platforms. Meta, with its extensive social network, is a major beneficiary of this favorable trend. Meta and TikTok lead global social media ad spending at $182 billion, with a projected 15.2% year-over-year growth in 2023.

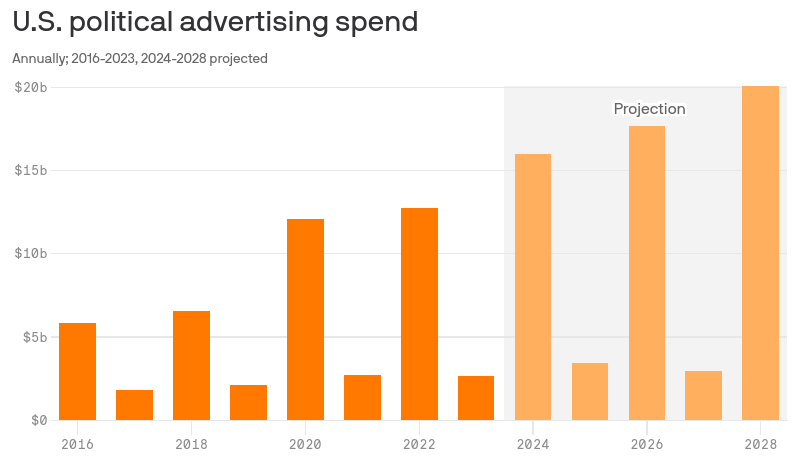

Against the backdrop of the upcoming 2024 U.S. election cycle, the exponential growth in political ad spending is driving Meta's profit growth. Political ad spending is expected to reach $15.9 billion, which bodes extremely well for Meta's revenue growth. Specifically, political ad spending in the 2024 election cycle is projected to be 31% higher than in the 2020 cycle. Based on trends, ad spending could reach $20 billion by the 2028 election cycle.

During the U.S. presidential election, there is a positive correlation between Meta's revenue and political advertising. In addition, elections often increase user activity on social media platforms, leading to an increase in ad impressions and further promoting Meta's revenue growth. Lastly, the shift of U.S. advertising budgets from traditional media to digital channels provides Meta with the opportunity to capture an expanding share of the digital advertising market.

According to Bloomberg, the 2024 U.S. presidential election is expected to drive a record $10.2 billion in political ad spending, with digital platforms including Meta projected to receive around $1.2 billion. However, other sources forecast political spending to be higher, nearing $16 billion.

This influx of funds is primarily dominated by broadcast television but also includes social media to a large extent, presenting significant revenue opportunities for Meta. The increase in political ads and content on the Meta platform may boost user engagement and ad revenue, impacting its financial performance and stock value.

Will 2024 see another metaverse insanity?

In 2021, the metaverse sparked a craze due to NFTs in the cryptocurrency bull market. In October 2021, Facebook announced its rebranding as Meta. Meta's Reality Labs division reported a loss of $15.75 billion based on TTM and a cumulative loss of $31.125 billion since the third quarter of 2021.

Although metaverse applications are currently mainly limited to the gaming industry, there are many applications in advertising and e-commerce.

The augmented reality market is expected to grow from $25.1 billion in 2023 to $71.2 billion in 2028, with an astonishing compound annual growth rate of 23.2%, while the virtual reality market is expected to grow from $12.9 billion in 2023 to $29.6 billion in 2028, with an 18% compound annual growth rate.

With the release of Apple's Apple Visio Pro, headsets may once again attract attention. IDC predicts a compound annual growth rate of 96.5% for VR headsets from 2023 to 2027 and 30% for AR headsets. Meta held a market share of 50.2% in the second quarter of 2023.

AR/VR and the metaverse are still in the innovation trigger stage, with significant room for technological innovation, and great development potential in social media and e-commerce.

Valuation

META had $61.1 billion in cash and $60.1 billion in marketable securities at the end of Q3, far exceeding current liabilities of $30.5 billion, indicating a very healthy balance sheet.

Total expenditure in 2024 is expected to jump from $89 billion in 2023 to $94-99 billion, partly from Reality Labs and partly from AIGC infrastructure investments.

The company's PE for the past 12 months is 24.9 times, higher than the average for the past 5 years, but not exaggerated relative to the high at the beginning of 2022. The expected performance improvement in 2024 will be the best support for the company's valuation. At the current price and market expectations for 2024 earnings, the forward P/E ratio for 2024 is around 20 times, returning to the 5-year average level.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.