3 Reasons To Buy BP For 2024

Summary

- BP has underperformed in the past year, but a 6.6% price jump on its recent results indicates that the tide can turn in 2024.

- With a comfortable dividend payout ratio and the potential for an earnings upside this year, dividends can continue to grow while increased share buybacks can also bump up the price.

- While its slow transition to cleaner energy is a long-term concern, going by BP's forecasts, for now, the stock looks good based on possible returns to investors and market multiples.

Matt Cardy/Getty Images News

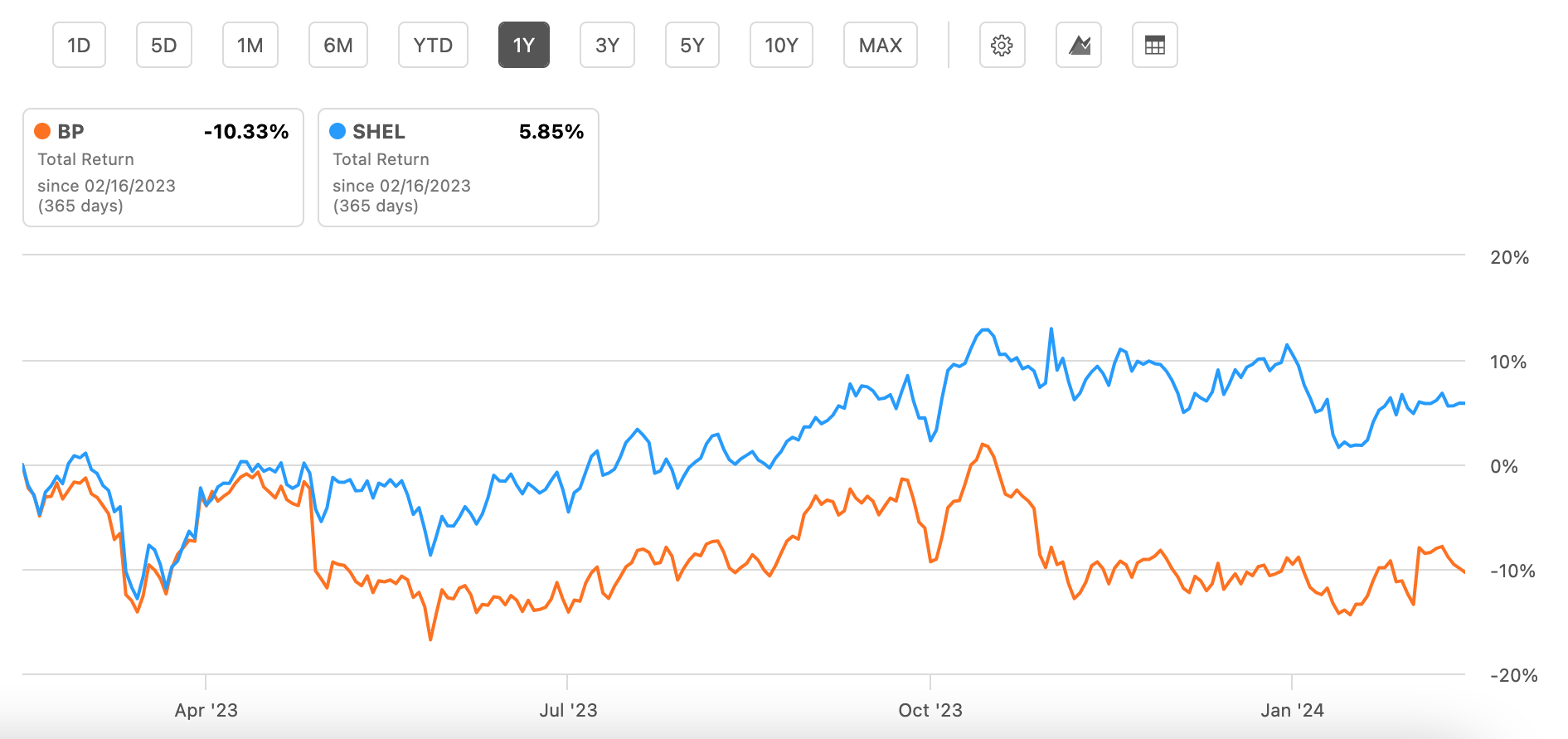

Compared to its UK-based peer Shell plc (SHEL), the oil and gas stock BP p.l.c. (NYSE:BP) has underperformed in the past year. Not only has its price declined by 13% even as Shell has risen by a small 2.7%, but the total returns are negative too (see chart below).

The past doesn't always have to form the future, though. Especially not after its price jumped by 6.6% on the release of its recent full-year 2023 results. So there's hope yet. Here I present three reasons why fortunes could smile on BP investors this year. However, the risks from its slow transition process for long-term investors are touched upon as well.

Price Returns, BP and SHEL (Source: Seeking Alpha)

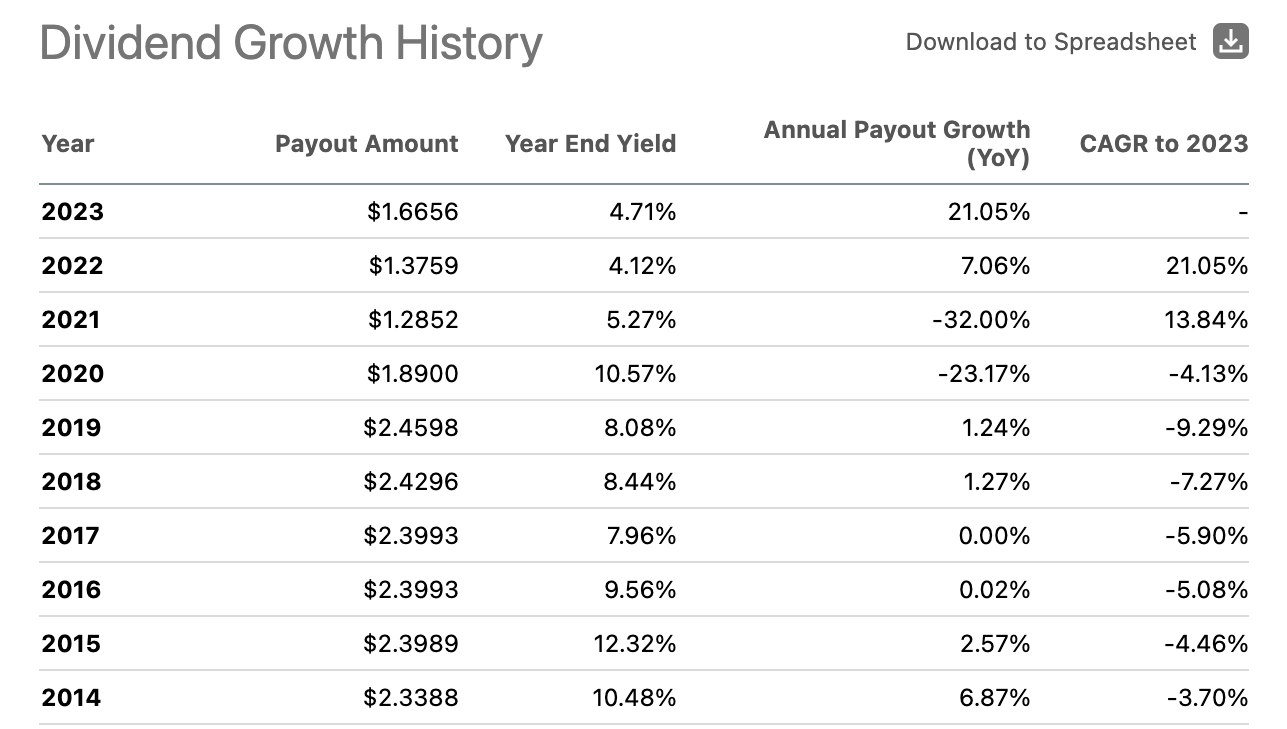

#1. Dividend outlook and share buybacks

BP's dividends are a highlight for the stock. While they haven't grown consistently over the past decade because of the cyclical nature of the business, there has been a consistent dividend payout over this time (see table below).

Moreover, a simple average of the year-end yield is at a substantial 8.5% in the last 10 years. Even now though, its trailing twelve months [TTM] yield isn't bad at 4.9%, higher than Shell's at 4.1% and also the energy sector's median yield of 3.8%.

Source: Seeking Alpha

The outlook for dividends is also positive for 2024 after the company's latest earnings update. This is even though the company's preferred profit measure, underlying replacement cost [RC] profit, has almost halved to USD 8.7 billion (2022: 16 billion) on lower realisations and higher depreciation and amortisation costs during 2023.

Even after having increased dividends by a notable 18.5% year-on-year (YoY) during the year, the dividend payout ratio for 2023 is a comfortable 35.7%, indicating that there's room for further increases this year. This is especially worth mentioning considering analysts' earnings per share [EPS] expectations of USD 4.77 per ADS, essentially flat from the USD 4.78 seen for 2023. At worst, it means that the dividends will remain unchanged, which isn't too bad an outcome considering its present dividend yield.

Further, the company has also announced USD 3.5 billion worth of share buybacks for the first half of 2024 (H1 2024). This is 3.5% of the stock's current market capitalisation, which could support its price this year. It plans buybacks worth at least USD 14 billion through 2025, potentially offering even more support to the stock.

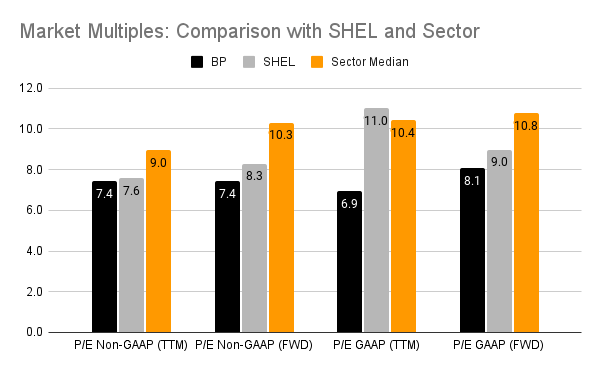

#2. Attractive market multiples

Next, with the stock's price fall over the past year, it's trading at attractive market multiples now (see chart below). Specifically, the non-GAAP forward price-to-earnings (P/E) ratio, which is instrumental in determining its dividends, is at 7.4x.

This is not only lower than the corresponding ratio for SHEL but even lower than that for the energy sector's median ratio. This indicates that its price can see an uptick of anywhere between 11% to 39%. The average price rises based on SHEL's and the sector median's P/E indicate a 25% likely price rise.

Source: Seeking Alpha

#3. Supportive factors at play for 2024

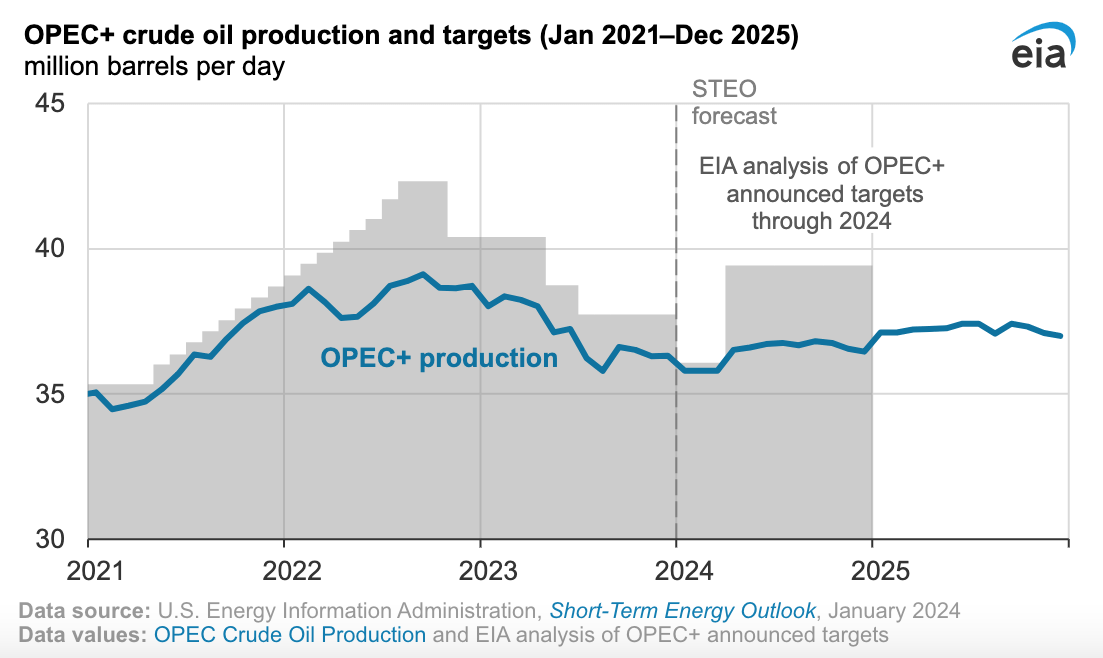

Even though the EPS estimates for 2024 reflect little change from 2023, as discussed above, there are factors at play which can bump it up. The first is oil prices, which can be more favourably placed this year. After an 18% YoY decline in Brent Crude's price in 2023, the US Energy Information Administration forecasts the figure to be at USD 82/bbl this year. This is hardly any different from last year, as OPEC+ countries are expected to keep their production relatively muted.

At the expected 36.4 million barrels per day, their production figure is 9.5% below the average production of 40.2 million barrels per day during the five years of 2015-19 before the pandemic. The production targets are based on weaker global demand, and going by the expected slowdown in the US economy this year and China's less robust than forecast post-pandemic recovery, the trend can persist.

Source: EIA

However, BP itself targets "slightly" higher production this year, which can reflect in earning gains. Additionally, by the end of the year, the company's net debt was down to USD 20.9 billion, the lowest level seen in 10 years. This is significant right now, considering it has seen a 42% YoY increase in interest expense in 2023, shaving off 4% from the underlying RC profit.

If BP continues to focus on reducing net debt in 2024, it's quite likely that at a time when interest rates are already expected to come down, there can be a softening in interest expenses. This in turn can also have some positive impact on the EPS, though the extent to which D&A expenses and lower realisations affect earnings could impact it negatively.

Looking beyond 2024

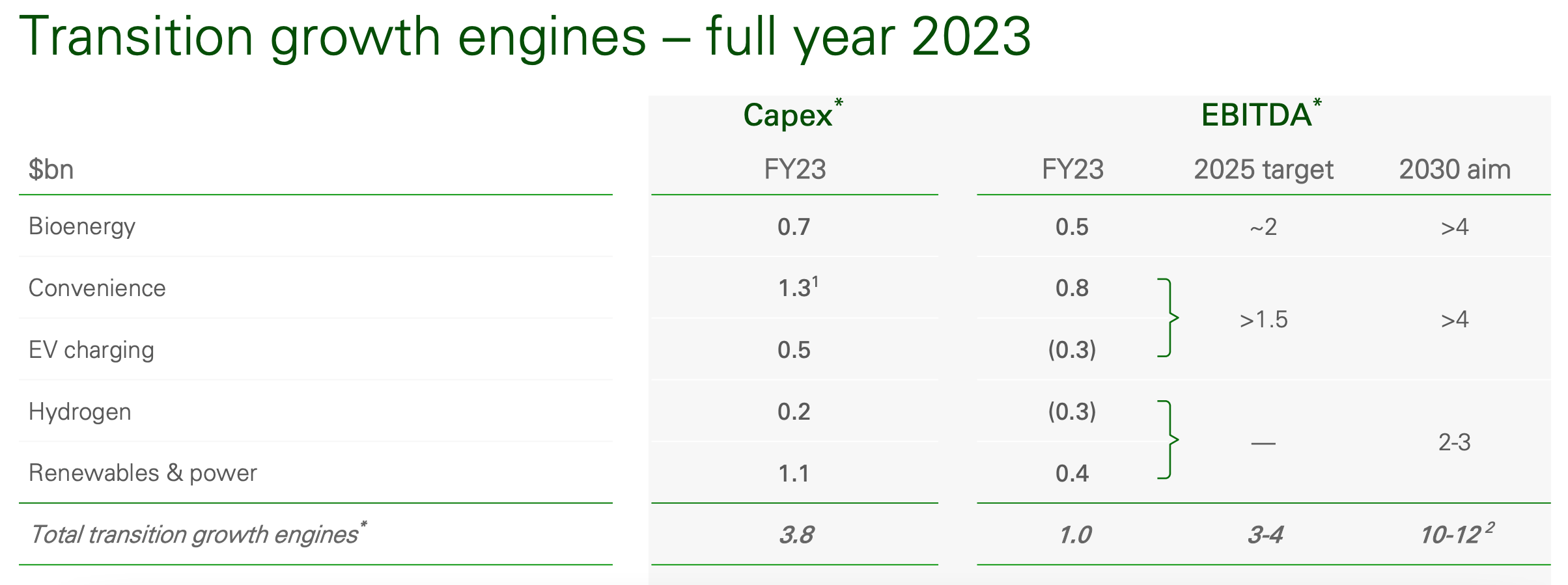

While the stock looks good for now, the energy transition is progressing slowly. In 2023, all five of its transition growth engines, as it calls them, generated a total EBITDA of USD 1 billion compared to an adjusted EBITDA of USD 43.7 billion for the company as a whole.

Of these, EV charging and Hydrogen are still loss-making (see chart below). Their share can rise, considering BP's USD 10-12 billion target by 2030, but how much depends on where the company's total EBITDA is by then. In short, while the world still needs oil and gas for now, BP's progress towards transformation needs to be observed to assess if it makes for a good investment for the long term. And right now, the progress isn't entirely convincing.

Source: BP

What next?

For 2024, there's much going for BP. After a healthy increase in profits in 2023, this year may just see continued earnings growth as oil prices are expected to stay steady, the company increases its production a bit and its focus on reducing net debt can reduce its interest expenses.

In the meantime, its dividend outlook is fine going by its healthy dividend payout ratio and increased share buybacks can increase the stock price. Its market multiples already point towards a price uptick. For these reasons, I'm going with a Buy rating on BP.

However, when considering it as a long-term investment, its transition to cleaner energy is key, which is progressing slowly so far. In fact, even by the end of this decade, it might not have made as much progress as desirable going by BP's own forecasts. This can change, of course, but that remains to be seen.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- YueShan·02-22Good⭐️⭐️⭐️LikeReport