Tencent's Mixed Q4 Earning: Domestic Game Down While Ads Up

At the close of the Hong Kong stock market on March 20th, $TENCENT(00700)$ released its financial report for Q4 and the full year of 2024.

Investment Highlights

Income slightly below expectations, with the gaming business lagging behind and the monetization of video acts growing.

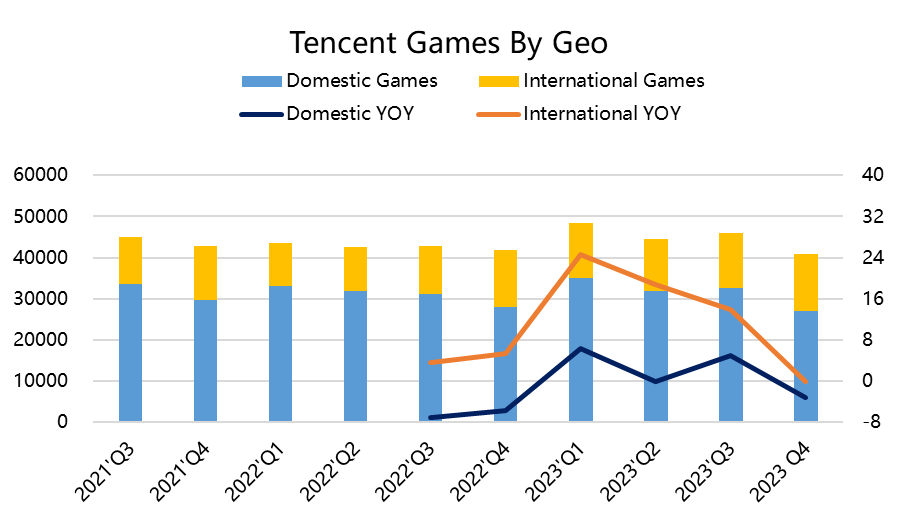

Particularly, domestic games are underperforming, with older games showing relatively better performance, but inevitably entering a downward cycle, while new games are below expectations and are at a disadvantage compared to similar competitors. Overseas game growth remains steady and serves as a strong support.

Additionally, with the help of AI, advertising further improves efficiency, and the rise in video acts also boosts the benefits of the WeChat ecosystem.

Furthermore, offline financial activities have strengthened, with financial technology showing stable improvement. There has been a significant increase in gross profit margin, benefiting from changes in cost structure. They have actively reduced high-cost businesses like video, audio, and gaming streaming, while increasing high-margin services like advertising and influencer marketing.

Meanwhile, the costs of projects like the ecosystem and online distribution have increased proportionally more than income. The drop in net profit stems from the promotion of new games.

Administrative expenses have remained stable, but marketing expenses increased by 79% year-on-year, partly due to a low base last year, but mainly due to expenditures on content promotion, indicating some difficulty in maintaining the status quo of domestic games.

The impairment of invested companies has increased, but with minimal impact. Earnings before interest, taxes, depreciation, and amortization (EBITDA) profit increased by 20% after the most important adjustments, despite the absence of dividends from Meituan.

Generosity continues in dividends and repurchases, with dividends rising by 42% to 3.4 Hong Kong dollars, and the plan is to increase repurchases from 49 billion Hong Kong dollars to 100 billion Hong Kong dollars in 2024.

In the short term, with positive sentiment following the inflow of funds into the Hong Kong stock market, major shareholders have not stopped selling, but the pace has slowed in the past week. It may still be necessary to support repurchases in the near future.

In terms of valuation, Tencent's earnings multiples remain at an extremely low level over the past 10 years, with the PE for the past 12 months at 14.3 times, far below the 10-year average of 31 times; and the EV/EBITDA for the past 12 months at 9.8 times, significantly lower than the 10-year average of 23 times.

Earnings Review

Top line

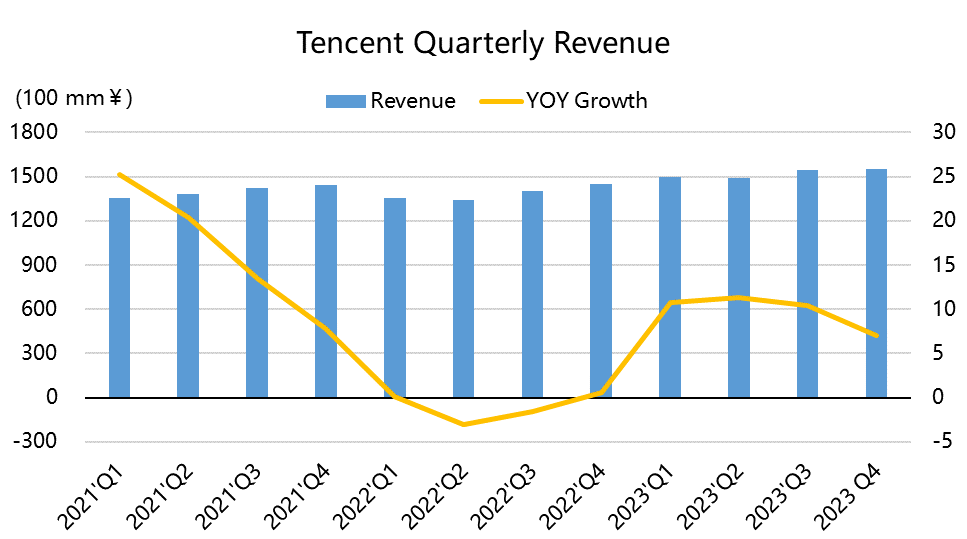

Revenue was 155.2 billion yuan, a year-on-year increase of 7%, slightly lower than the market's expected 157.4 billion yuan, with a year-on-year growth rate falling back to single digits;

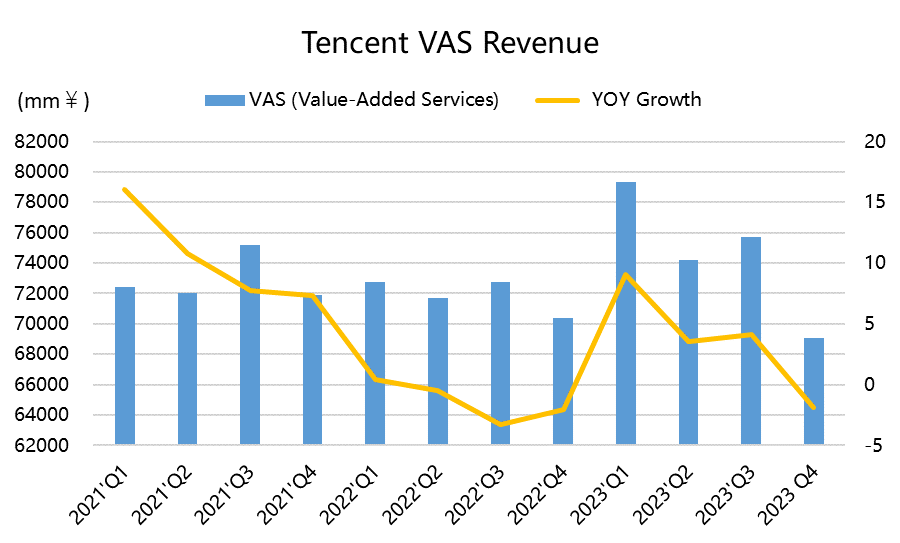

Among them, value-added business revenue was 69.1 billion yuan, a year-on-year decrease of 2%, lower than the market's expected 72 billion yuan; with domestic game revenue of 27 billion yuan, a year-on-year decrease of 3%, falling short of the expected 30.2 billion yuan; international game revenue was 13.9 billion yuan, a year-on-year increase of 1%, slightly lower than the market's expected 14.5 billion yuan; social network revenue was 28.2 billion yuan, a year-on-year decrease of 2%.

The online advertising business reached 25.7 billion yuan, a year-on-year increase of 21%, far exceeding the market's expected 28.3 billion yuan;

The financial technology and enterprise services business revenue was 54.3 billion yuan, a year-on-year increase of 15%, higher than the market's expected 54.8 billion yuan.

Bottom line

Gross profit increased by 25% year-on-year, with the gross profit margin rising from 43% last year to 48%.

Operating profit was 41.4 billion RMB, a year-on-year increase of 42%, lower than the market estimate of 46.7 billion. It saw a 7% decrease compared to the previous period,

Net profit was 42.7 billion RMB, a year-on-year increase of 44%, Non-IFRS net profit was 157.69 billion RMB, a year-on-year increase of 36%.

Adjusted EBITDA was 59.5 billion yuan, a year-on-year increase of 20%, slightly lower than the expected 60.6 billion yuan.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Brando741319·2024-03-25Will performLikeReport