Q1 Earnings Special| Which Big Bank Wins in Q1 Earnings Season?

Six Too-Big-To-Fail US banks have all released Q1 2024 financial reports.

With the macro still tight, but economic activity strong, all of them beat without surprise, business department in divergence.

Interest margin keeps narrowing but improved, the interest income has noticeably dropped, but the overall market expectation is not high. JPMorgan and Wells Fargo's partial interest income did not meet expectations, and the market had already priced this in.

CPI strong, short-term interest rate cut expectations fell, and it is still difficult to see growth in the interest margin.

Investment banking business as a whole is recovering, among which the growth of fixed-income underwriting business is the most noticeable. Wealth management business is growing steadily overall, and active market trading also creates more value for banks.

Banks face the pressure to control costs. Goldman Sachs and Morgan Stanley laid off 900 and 396 people respectively, Bank of America has reduced more than 4700 people since Q1 2023, and Citibank has a layoff plan of 7000 people. On the contrary, JPM added 2,000 employees in Q1.

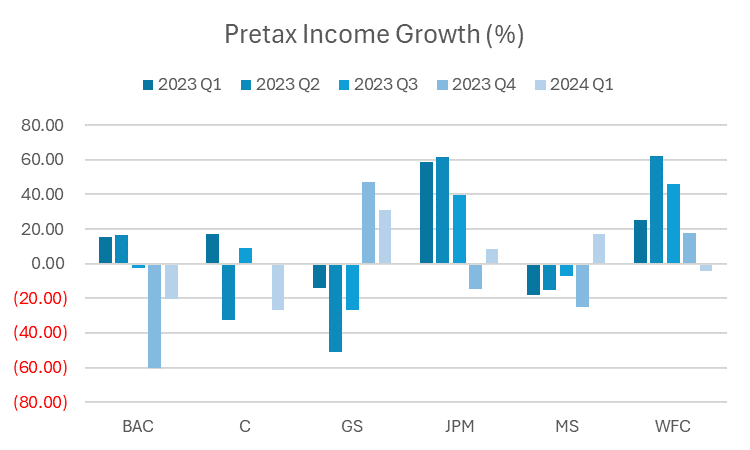

Looking at the growth of pre-tax profits, Goldman Sachs and Morgan Stanley performed the best.

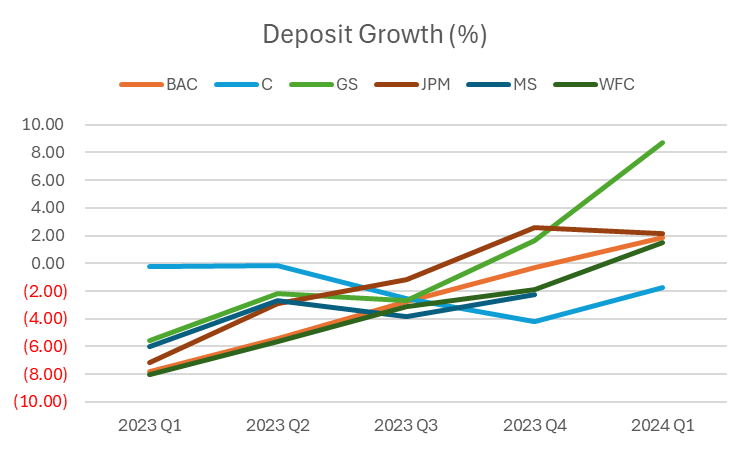

In terms of deposit growth, Goldman Sachs and Morgan Stanley performed the best.

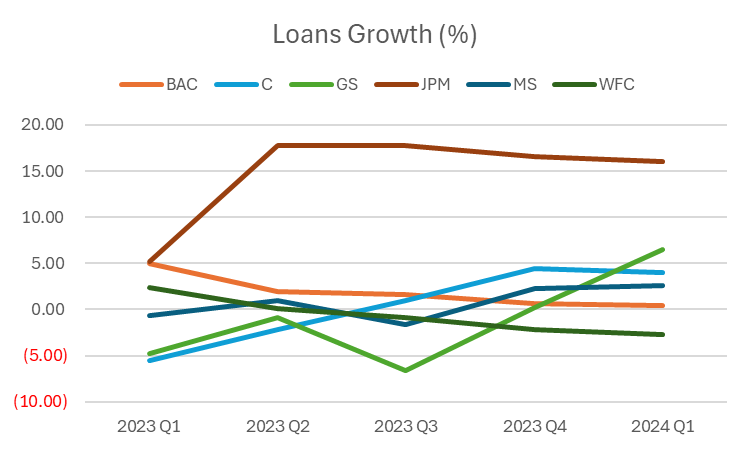

And for loan business growth, JPMorgan stood out.

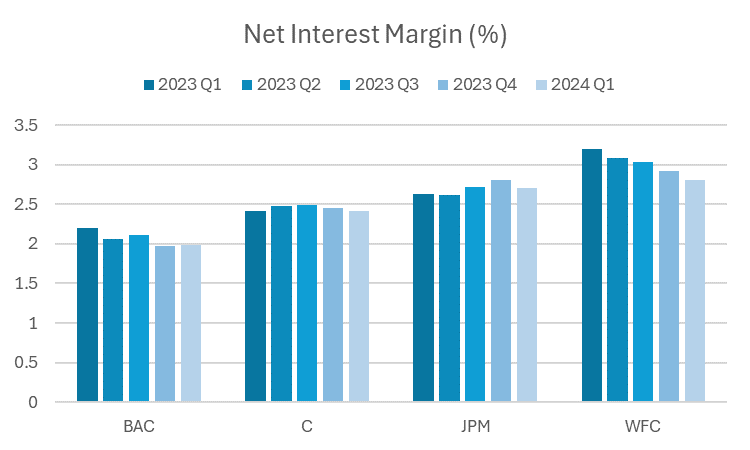

In addition, among the four banks with the largest interest business, the interest margin of Wells Fargo and Bank of America has been declining over the past five quarters, while JPMorgan has rebounded.

For details

Q1's revenue and profits both exceeded expectations, largely due to the robust performance of the underwriting business, which drove the recovery of the investment banking industry, doubling its revenue.

The revenue of the investment banking business grew by 16% year-on-year in this quarter. Fixed income underwriting has been a highlight for two consecutive quarters, benefiting from an increase in the issuance of large corporate bonds.

In addition, the wealth management business is stable and can generate more steady income, helping to balance the income from more volatile businesses such as trading and investment banking.

All major business lines have seen a significant increase in revenue, exceeding market expectations.

Debt underwriting activities driven by leverage financing activities have intensified, M&A transactions have increased driving consulting business revenue growth, and equity underwriting revenue has increased. At the same time, net income from mortgage loans has significantly increased, and net income from money and credit products has increased.

In addition, the income from the sale of the Marcus loan portfolio related to private banking and loans has significantly increased.

Driven by the strong performance of investment banking, fixed income, currency and commodities, and stocks, global banking and market revenue.

Net Interest Income (NII) guidance lacks growth, and people's expectations for the long-term federal funds rate continue to rise, but consumers maintain financial health with the support of a strong labor market, and the net inflows of consumer and community bank wealth management business are strong.

In addition, investment banking underwriting fees performed strongly.

Net interest income fell 2.9% in the first quarter of this year, but still better than expected.

Customers are striving to cope with persistently high interest rates and geopolitical tensions, and income from stock trading in the first quarter has jumped

With the increase in financing cost rates and the decrease in loan balances, net interest income fell by 8%, but at the same time, the total credit loss reserve was reduced to $938 million, with the reduction in loss reserves caused by commercial real estate and auto loans.

Trading income from market business increased and investment banking fees increased.

Profits fell, mainly due to paying more severance pay for unemployed employees, and reserving funds to supplement the government deposit insurance fund. The corporate reorganization plan proposed last September was completed in March.

The performance of the services and banking sectors was excellent, with securities service revenue increasing by 18%.

At the same time, the recovery of capital market and investment banking fees drove a surge in bank revenue.

However, the trading department and financial management business lagged behind.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Brando741319·04-18GoodLikeReport