Why TSMC Performs Better in Q1 than ASML?

$Taiwan Semiconductor Manufacturing(TSM)$ can be described as a money-making machine only to $NVIDIA Corp(NVDA)$ . In the recently announced Q1 financial report for 2024, it indeed exceeded expectations as expected.

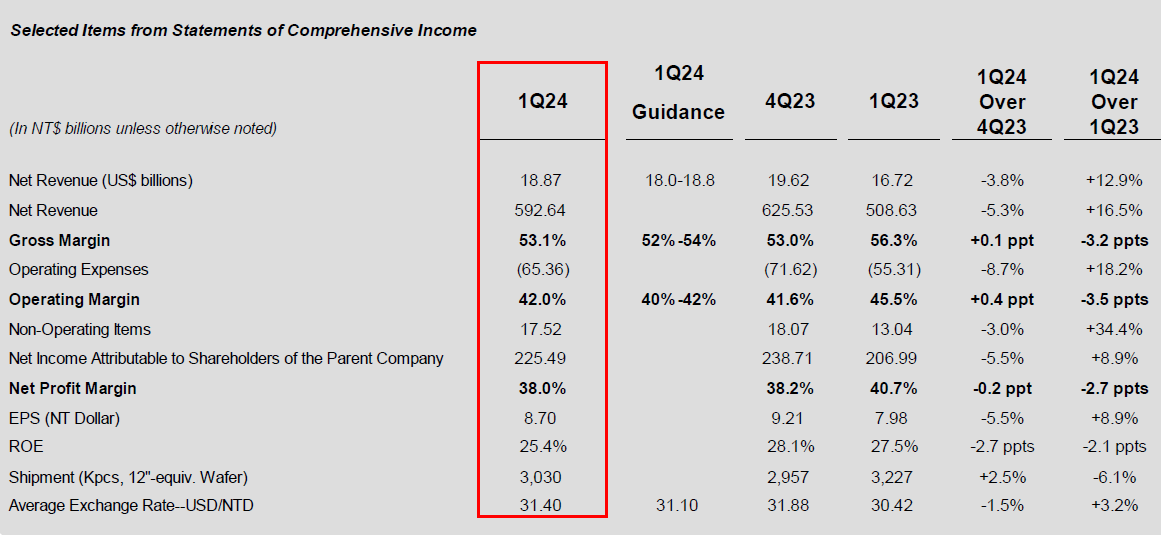

Revenue was 592.64 billion New Taiwan dollars, market expectation was 583.46 billion New Taiwan dollars

Gross margin was 53.1%, market expectation was 53.0%

Net profit was 225.49 billion New Taiwan dollars, market expectation was 215.1 billion New Taiwan dollars

Compared with the disappointment earning of $ASML Holding NV(ASML)$ yesterday, it can be described as a world of difference.

In fact, the most important thing for the demand for lithography machines is not the "fluctuating cancellations" in the mainland area. Relatively speaking, the mainland area still contributes 49% to ASML, but the customers in Taiwan, South Korea, the United States and other places are relatively conservative in their demand for ASML.

Some people may find it strange, isn't it the lack of AI computing power that drives the demand for chips? But TSMC did not say that it needs more lithography machines, there may be two reasons

The capital expenditures (CapEx) for 2022 and 2023 are relatively high, and the long-term demand for new plant construction has been calculated. The CapEx for 2024 is relatively conservative and there is no plan to further increase expenditure. In other words, it is not that aggressive;

The demand driven by AI may not have been transmitted to the end of equipment such as lithography systems, but it may rebound with the start of TSMC's US factory and the further improvement of other high-end process factories.

According to the guidance in TSM's 2023 annual report, the CapEx for 2024 is expected to be between 28-32 billion USD, with only 5.77 billion spent in Q1.

For the next three quarters, the average expenditure per quarter is expected to reach 7.42 billion ;

This may also be the basis for ASML's senior management to remain optimistic about the performance guidance for 2024.

I think it's okay that TSMC's capital spending is not too aggressive. The sales of Apple's iPhone15 did not meet expectations, and the sales forecast for the whole year of 2024 is also being revised down. This may lead to subsequent "cancellations." In the future, more capacity will undoubtedly shift to HPC and data centers.

At the same time, major manufacturers such as $Apple(AAPL)$ , $Alphabet(GOOG)$ , and $Meta Platforms, Inc.(META)$ all have plans to develop their own portal chips, because Nvidia is too dominant, not only there are capacity issues, but also problems with the autonomy of hardware systems. But whether Nvidia can meet all the demand or not, TSMC is still the final winner.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- lolmei·04-18😎LikeReport