CrowdStrike: Poised To Deliver Another Strong Quarter

Summary

- CrowdStrike has a flawless earnings surprise history over the last sixteen quarters, which increases the probability of another strong beat versus consensus estimates.

- The company demonstrates strong performance across all vital business metrics, with accelerating ARR growth and rock-solid customer retention rates.

- CrowdStrike's expanding strategic partnerships with cloud and AI companies increase the likelihood of positive forward-looking comments during the earnings call.

- Current valuation is attractive, according to my discounted cash flow simulation.

Sundry Photography

Investment thesis

My previous bullish thesis about CrowdStrike (NASDAQ:CRWD) aged well as the stock delivered a staggering 71% rally since November 2023, significantly outpacing the broader U.S. market. The company reports its Q1 FY2025 earnings next week, on June 4th. Today I want to preview the upcoming earnings release and how this might unfold in light of recent developments. In summary, I am quite optimistic about the upcoming earnings release and my analysis suggests that this profitability and growth superstar is fairly valued. Since "it's far better to buy a wonderful company at a fair price than a fair company at a wonderful price", I reiterate my "Strong Buy" for CRWD stock.

Recent developments

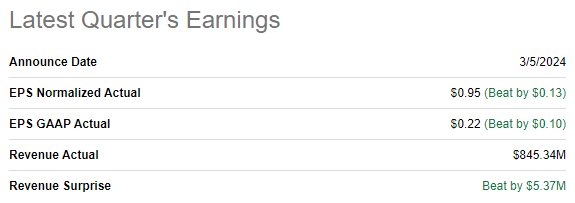

CRWD released its latest quarterly earnings on March 5, surpassing consensus revenue and EPS estimates. Revenue grew by 33% YoY. The adjusted EPS more than doubled, from $0.47 to $.095.

Seeking Alpha

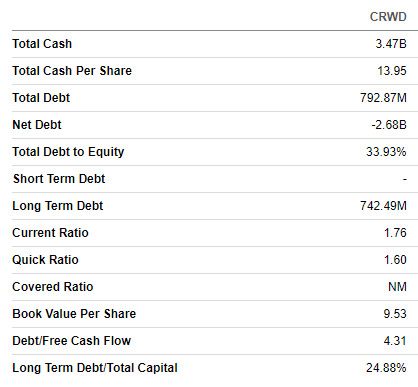

CRWD continued exercising its impressive operating leverage with a notable expansion of key profitability metrics. The cross margin improved from 72.5% to 75.3% YoY, which helped in expanding the operating margin from -9.7% to 3.5%. Strong operating performance helped to generate a $406 million net change in cash, and CRWD had a $3.5 billion cash pile as of the latest reporting date. Debt is well below a billion, which is nothing compared to the company's $84 billion market cap. The balance sheet is a fortress and positions CRWD well to continue investing in growth and innovation.

Seeking Alpha

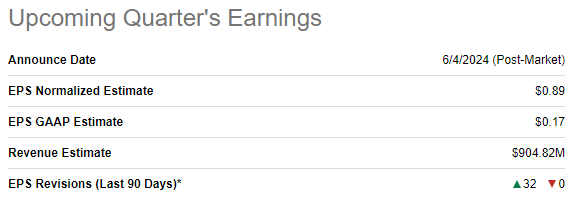

The upcoming earnings release is scheduled for June 4. Consensus estimates expect Q1 FY 2025 revenue to be $904 million, meaning a 30.6% YoY revenue growth. The adjusted EPS is expected to outpace revenue increase and expand from $0.57 to $0.89, indicating a 56% YoY growth. When the adjusted EPS growth outpaces revenue dynamics it is a robust bullish sign meaning that the company continues exercising its operating leverage and scaling the business means more value for shareholders. Another positive sign is that Wall Street analysts are bullish about the upcoming earnings release, with 32 EPS upgrades over the last 90 days.

From the QoQ perspective, revenue is expected to grow as well, by 7%. The EPS is expected to shrink sequentially by six cents, but quarter-over-quarter seasonality in profitability seems okay to me.

Seeking Alpha

There are a few more reasons to be optimistic about the upcoming earnings release. Past achievements do not guarantee future success, but significantly increase the probability of future success. The fact that CRWD has a flawless earnings surprise history over the last 16 quarters means that the probability of beating consensus estimates again on June 4 is extremely high.

My expectation that the company will surpass consensus estimates on June 4 is also supported by the aggressive pace of hiring new employees. My search on LinkedIn shows there are 1,233 job openings from CrowdStrike. This is a clear indication of the management's confidence in the sustainability of the massive growth momentum the business experiences.

The management's target operating model looks doable across key metrics. I am so confident because CRWD's TTM profitability metrics are already close to targets. Since CRWD has a strong history of demonstrating operating leverage, I am highly confident that with the expected revenue growth, profitability metrics are poised to expand further.

CRWD's latest earnings presentation

Dynamics across key business performance metrics demonstrated by the company in Q4 also increases my optimism about the upcoming earnings release.

CRWD's latest earnings presentation

CRWD's Falcon Platform demonstrates its cross-selling strength, which I see from the expanding percentage of customers adopting five or more modules. Deals with eight or more modules more than doubled YoY. Compared to Q3 FY2024, subscription customers with five or more, six or more and seven or more modules have also expanded by one percentage point for each category.

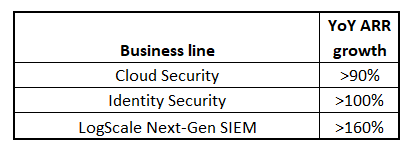

Customer retention metrics are also crucial to understand sustainability of revenue growth pace. Despite a rapid increase in scale, CRWD sustained a 119% net dollar-based retention rate over the last three quarters. The gross retention rate is also stellar and remains stable. CRWD's cross-selling and customer retention help in driving the ARR [Annual Recurring Revenue] growth, which accelerated in Q4 as well.

CRWD's latest earnings presentation

The ARR demonstrates strength across all CRWD's business lines, indicating that all of the company's offerings are extremely hot, and the management has clear vision of customers' needs. With such a strong ARR growth across all business lines, CRWD is poised to sustain its aggressive revenue growth for longer. Since 94% of the company's revenue is generated from subscriptions, CRWD is firmly positioned to maximize benefits of its vast cross-selling potential.

Compiled by the author

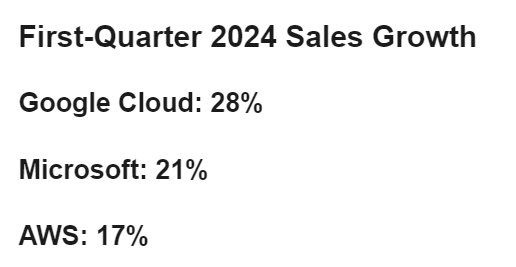

Recent developments also suggest that the management's forward-looking comments are also likely to be positive. On May 2, CRWD announced that AWS is replacing a variety of cloud point products with Falcon Cloud Security. This recognition from the world's by far the largest cloud infrastructure company is a strong bullish sign, emphasizing CRWD's technological edge. CRWD does not only focus on expanding partnership with AWS, but also works closely with Amazon's (AMZN) closest rivals in the cloud business.

On May 7, the company unveiled the launch of CrowdStrike Falcon for Microsoft's (MSFT) Defender to improve the visibility into threats that bypass Defender and the threat hunting required to stop breaches.

CRWD also announced its partnership with another cloud giant, Google (GOOG) on May 9. The initiative is aimed to enhance Mandiant's Incident Response [IR] and Managed Detection and Response [MDR] services by integrating CRWD's Falcon with the Google Cloud's Security Operations platform.

crn.com

My optimism is also supported by the ongoing boom in AI and cloud. All three cloud giants demonstrated robust revenue growth in Q1, which is also highly likely a bullish sign for CRWD. More demand for cloud services also means more demand for cloud cybersecurity. As CRWD expands its partnerships with all three industry key players, I think that the company is likely to absorb strong revenue growth delivered by cloud industry's leaders.

To conclude, CRWD's flawless earnings surprise history and strength across vital business metrics adds to my optimism about the company's ability to deliver another strong quarter. Expanding strategic partnership with the world's leading cloud and AI companies increases the probability that the management's forward-looking comments will be optimistic during the upcoming earnings call.

Valuation update

CRWD rallied by 120% over the last twelve months. YTD performance is also robust with a 36% share price growth. Valuation ratios are sky-high compared to the sector median.

Seeking Alpha

However, most of them are lower than CRWD's historical averages. Moreover, given strong EPS growth potential, the P/E ratio is expected to demonstrate rapid contraction over the next few years.

Seeking Alpha

Looking only at valuation ratios is insufficient for a growth stock. Therefore, I am simulating the discounted cash flow [DCF] model with an 8.5% WACC recommended by valueinvesting.io. As I did in my previous analysis, I rely on consensus revenue estimates for the next decade. The TTM FCF margin ex-stock-based compensation [ex-SBC] is 12%, which is my assumption for the base year. Given CRWD's stellar profitability expansion pace and expected aggressive revenue growth, I incorporate a 100 basis points yearly FCF margin expansion.

Author's calculations

The stock is perfectly fairly valued, according to my DCF model. The business's fair value is very close to the current market cap. I believe that the fair valuation is still attractive because growth and profitability demonstrated by CRWD deserve substantial premium to the share price.

Risks update

In my DCF model I rely on long-term consensus estimates. The growth trajectory is aggressive, as Wall Street expects a 24% revenue CAGR for the next decade, a challenging task even for a superstar like CRWD. The DCF model is very sensitive to changes in revenue growth projections. For example, switching the next decade's revenue growth to 20% makes the stock undervalued by 24%, which is a substantial premium even for a star like CRWD.

Author's calculations

During the upcoming earnings call the management might soften its FY 2025 guidance, which might be negatively absorbed by Wall Street and analysts will notably reconsider growth potential for the entire decade. This will inevitably lead to the stock selloff. On the other hand, the potential guidance boost will likely lead to more aggressive long-term revenue growth projections from Wall Street.

The competition in the cybersecurity space is fierce with several technological stars in the industry like Palo Alto Networks (PANW), Fortinet (FTNT), Zscaler (ZS). To sustain its stellar growth rate, CRWD must differentiate, which requires substantial investments in innovation. In case CRWD sees some stagnation in its market share expansion, the management might initiate R&D spending boost, which will weigh on profitability growth.

Bottom line

To conclude, CRWD is still a "Strong Buy". I expect the company to deliver another strong quarter, with the management keeping a robust outlook. The valuation is still attractive as the stock is fairly valued at the moment.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- AdelaideFox·05-31Overall, I agree that CRWD is still a strong buy.LikeReport