US-China real estate divergence: who's adding and who's subtracting?

The "backwardation" of the monetary and credit cycles

In 2022, the money and credit cycles in China and the United States diverged markedly. China chose to cut interest rates and money supply growth accelerated, with M2 increasing by RMB 25.8 trillion for the year 2023. The U.S., on the other hand, raised interest rates, and the year-over-year growth rate of money supply turned negative, with a net decrease in M2 of $504.3 billion.

United States: "New tricks" for second mortgages

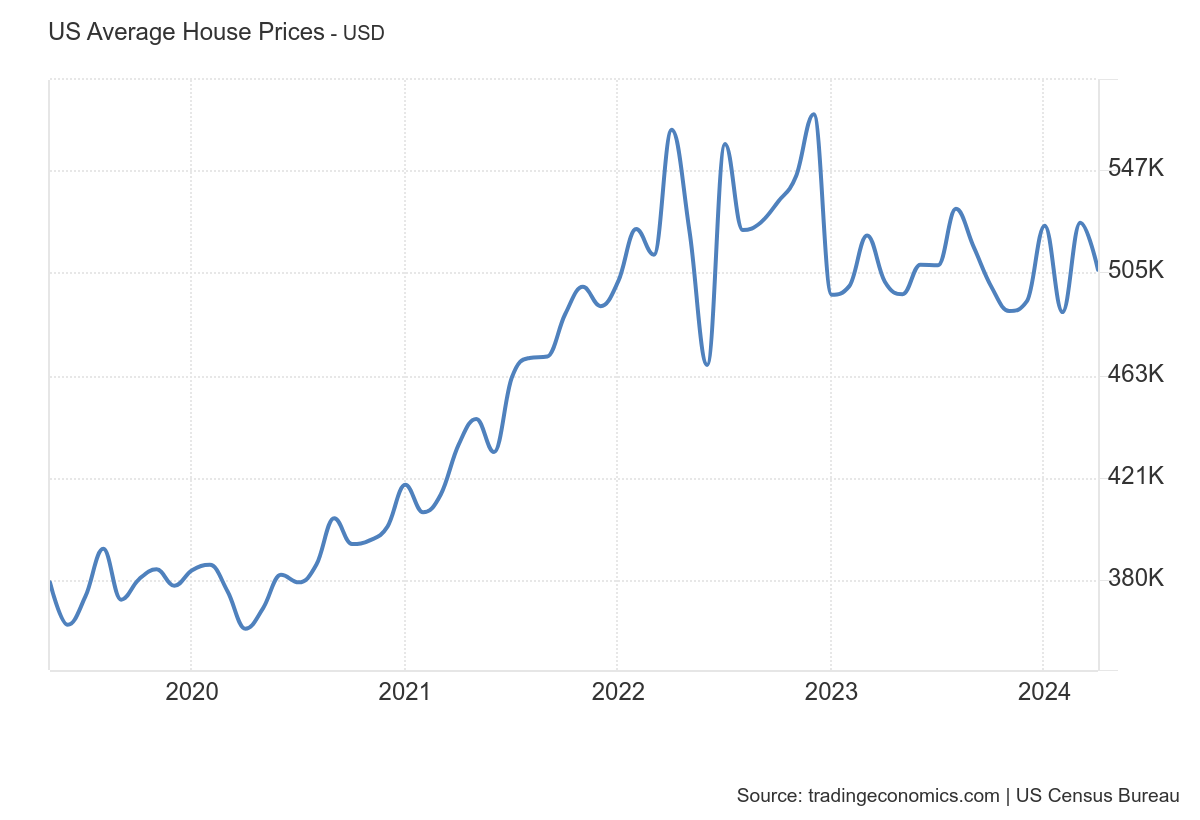

The U.S. real estate market faces constraints of insufficient housing supply, and home prices continue to climb. The wealth effect on residents from rising home prices has been significant, but refinancing a mortgage is not cost-effective in the current environment of high mortgage rates. Therefore, Freddie Mac $Freddie Mac (FMCC )$ has introduced a second mortgage program that allows residents to take out a second mortgage on their home equity to obtain a second loan and liquidate their home wealth at a lower interest rate.

Significant Home Price Upside: Median home prices have risen nearly 50% since 2020.

Second mortgages: The involvement of government-backed institutions lowers lending rates, helping residents to access more low-cost funds in the existing interest rate environment, allowing the wealth effect of rising house prices to be realized, supporting residents' consumption and investment, and further supporting corporate cash flow.

China: "Arbitrage" in consumer loan-for-mortgage swaps

In China, the high interest rates on stock of housing loans and the slow pace of adjustment have led to residents choosing to repay their loans early to alleviate debt pressure. The weighted average interest rate for personal housing loans from financial institutions currently stands at 3.69 per cent, with the first mortgage rate at 3.59 per cent and the second mortgage rate at 4.16 per cent.

The balance of personal housing loans was $38.2 trillion in Q1 2024, down about $700 billion from the high of $38.9 trillion at the end of last year's Q1, with the fastest decline in Q2 and Q3 2023, down $300 billion and $200 billion, respectively.

At the same time, the rapid decline in consumer loan interest rates for residents to provide arbitrage space, with low-interest consumer loans to replace the stock of mortgage loans, although it seems to increase the leverage, in fact, is to reduce the debt burden.

Mortgage rates: higher than consumer loans, prompting residents to seek lower interest rate loan products.

Consumer loan replacement: provides an opportunity to reduce the debt burden, but there is also a risk of loan renewal. If the new consumer loans do not enter the real economy and stimulate consumption, they will remain in the financial system.

Leverage."

asset revelation

U.S.: Consumption supported, economic slowdown but interest rate cuts unlikely.

China: The market may show structural market as residential credit contracts and the economy lacks domestic energy.

$S&P 500(.SPX)$ $Invesco QQQ(QQQ)$ $NASDAQ(.IXIC)$ $DJIA(.DJI)$ $US10Y(US10Y.BOND)$ $US30Y(US30Y.BOND)$ $USD/CNY(USDCNY.FOREX)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.