MU Q3 Review, fantastic earnings but too much priced-in?

$Micron Technology(MU)$ in the 26th U.S. stock market after-hours released Q3 financial results for fiscal year 2024, the overall results in line with market expectations, the storage industry face turnaround driven by its revenue and gross margin rebound, the next quarter of business is expected to improve, but there are also some problems and challenges.

Investment Highlights

Overall performance: Revenue of $6.811 billion, up 81.5% year-on-year, slightly better than expected, and net income of $332 million, remaining profitable. Revenue rebound was mainly driven by growth in the DRAM and NAND businesses, while operating profit and margins rebounded on the back of improved gross margins.

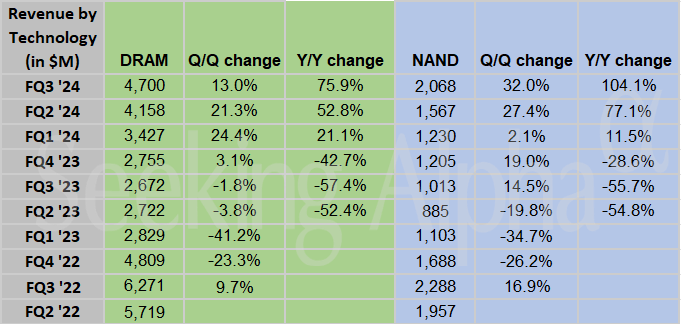

DRAM and NAND business rebound: the price end of the quarter were both double-digit YoY improvement, DRAM business revenue of $4.692 billion, up 13% YoY, shipments had a mid-single-digit decline, prices recovered by about 20%; NAND business revenue of $2.065 billion, a 103.8% YoY improvement in volume and price, YoY growth of 32%.

Operating Expenses: Operating expenses were US$1,141 million, an increase of 16.8% year-on-year. The operating expense ratio was stable, with varying degrees of growth in selling and administrative expenses, and R&D expenses.

Next Quarter Outlook: Revenue is expected to be $7.4-$7.8 billion, largely in line with expectations, and gross margin is expected to be 32.5% to 34.5%, in line with expectations and continuing to improve sequentially.

Market Expectations: driven by rising storage prices and AI demand, the stock price was higher in the early period, and "Price-in" the performance of the expected good, but the company did not give stronger expectations, affecting the market's confidence, the current share price contains too much expectation, the company's performance and expectations are difficult to support.

Storage Industry Expectations: Storage is cyclical, HBM brings phases of growth to see, but it is difficult to get out of the cycle of attributes.

Conference Call Review

Data Center Business Growth: AI demand is driving significant revenue growth in the data center business, which is expected to continue in fiscal 2024 and 2025.

Advanced Technology Node Advancement: DRAM and NAND technology nodes continue to be upgraded, with 1-gamma DRAM and next-generation NAND nodes advancing on schedule.

Promising progress in HBM business: HBM shipments are growing, generating significant revenues, and are expected to reach a market share comparable to DRAM by 2025.

Cost and Supply: DRAM and NAND front-end costs are expected to decrease in 2024, industry supply is lower than demand, and Micron will control supply and capital expenditures.

Future Capital Expenditures: Capital expenditures will be approximately $8 billion in fiscal 2024, with a significant increase in 2025 to support programs such as HBM and the construction of new U.S. plants.

Market Outlook: Industry demand for DRAM and NAND bits is projected to grow in the mid-teens by 2024, with favorable demand growth in the medium term.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.