BIG TECH WEEKLY | Game Of Expectations

Big-Tech’s Performance

The big tech earnings season has officially begun, but this July is clearly a month of heightened volatility, superimposed on a variety of scenarios such as the "Trump trade" and the "interest rate cut trade", and it seems that investors have begun to worry about the risks associated with the over-concentration of big tech.

As Tesla and Google's earnings this week did not ease market sentiment, on the contrary, it is more likely to force out the "risk aversion", on the contrary, the yen previously caught in the Carry Trade was released.That the next few other big technologies to leave the space is very small.

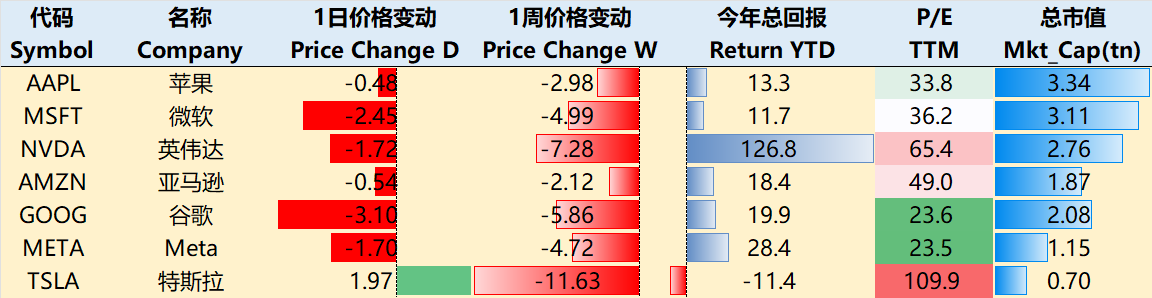

Through the close of trading on July 25th, all of the big techs closed lower over the past week.The top performers were $Amazon.com(AMZN)$ -2.12%, $Apple(AAPL)$ -2.98%, $Meta Platforms, Inc.(META)$-4.72%, $Microsoft(MSFT)$ -4.99%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ -5.86%, $NVIDIA Corp(NVDA)$ -7.28%, $Tesla Motors(TSLA)$ -11.23%.

Big-Tech’s Key Strategy

Sentiment during earnings season was pessimistic, with "Big Beat" dropping slightly, "Little Beat" dropping sharply, and "Miss" dropping wildly?

Tesla, due to the continued decline in car-making margins, as well as the delay of Robotaxi, investors sold off further after the report, Google, despite the strong performance of key metrics, but also due to YouTube is not so strong, as well as capital expenditures, also fell slightly.This, coupled with the previous staggered earnings season with weaker performance from non-cyclical companies like CRM and WDAY, also set a cautious tone for the entire earnings season.

Expectations for next week's software big tech companies are even more important, as a sequential selloff would inevitably have a greater impact on the broader market, further depressing expectations from a sentiment perspective and leading to "habitual selling".

MSFT: Azure growth expectations remain high (consensus +30.7% YoY), and Copilot deployment is going well (personal production sector consensus +9-11% YoY), pulling software sales back up.In addition, LinkedIn may be in some trouble (lighter hiring environment), but the PC division may have better guidance due to AI PCs. Microsoft rarely disappoints investors, but in the absence of major new catalysts, it's more of a Priced-in vs.Microsoft rarely disappoints, but in the absence of major new catalysts, it's more of a Priced-in vs. "Sell the fact" game, but once the growth rate falls short of expectations, it may not necessarily sell off, but reconsider its weighting, which could lead to more Rebalancing outflows.

META: Google's search advertising business greatly exceeded expectations, in fact, also gave META some guidance, also previously said that this year, CPI fell back, consumer goods companies are highly competitive, the increase in e-commerce advertising, coupled with the election year spending, Meta should be benefited.But Trump's hatred of Meta makes this part of the expectation may fall through, coupled with investors are more concerned about the inputs and outputs of the AI side of the company, there is also because because of excessive capital expenditure caused by investor antipathy.In addition does not rule out like Google, said clearly "the impact of amortization may gradually affect profitability".

After the earnings report comes out, in addition to the traditional revenue, profit, as well as several main business trends and guidance, but also pay attention to what "easy to be amplified by investors' emotions" details?

Capital expenditure cycle.With NVIDIA seeing a lot of capital outflows, investors may be past the "raise your bets as long as you invest in AI" stage, and are starting to shift their attention from the "profit cycle" to the "capex cycle"."These include, but are not limited to

The impact of depreciation and amortization on profitability;

Impact on free cash flow.Even as strong as Microsoft: the FY25 Capex is expected to exceed $50 billion (and could reach $67 billion), which would result in a decline in the FY25 free cash flow margin of about 100 basis points, from 27.5% in FY24 to 26.5%;

Impact on changes in revenue and margin guidance for the next quarter and full year.

Impact of Currency Rates.The strong dollar in Q2 is bound to have an impact on the international business segment, which will further impact the overall margins.However, looking at the current trend of interest rate cuts, relief is expected in the next six months.

The impact of macroeconomic headwinds, rate cuts are expected to mitigate the impact of the crunch to some extent, but the same is also more favorable to smaller tech stocks, especially growth stocks (eased financing environment), which will make investors reconsider rebalancing their positions in growth stocks.

Big-Tech Weekly Options Watcher

META is due to report Q2 earnings next week, following several quarters of fairly dramatic earnings day performance, so current week-to-week IVs are currently at high levels.

Looking at the current options distribution, in contrast to this week's TSLA, META is instead a bit higher in PUT open interest, which of course has been impacted by the earnings report from Google, also in the AI advertising business, as well as the recent big pullback in tech stocks.In terms of specific positions, the 470 and 400 positions have the most PUTs on them, on the one hand the 470 had previously fallen from out-of-the-money to in-the-money, suggesting that shorts are still hoping to survive the earnings report (and possibly hedging their bets to hedge their bets), whereas the PUT at 400 is more of a support.

Big-Tech Portfolio

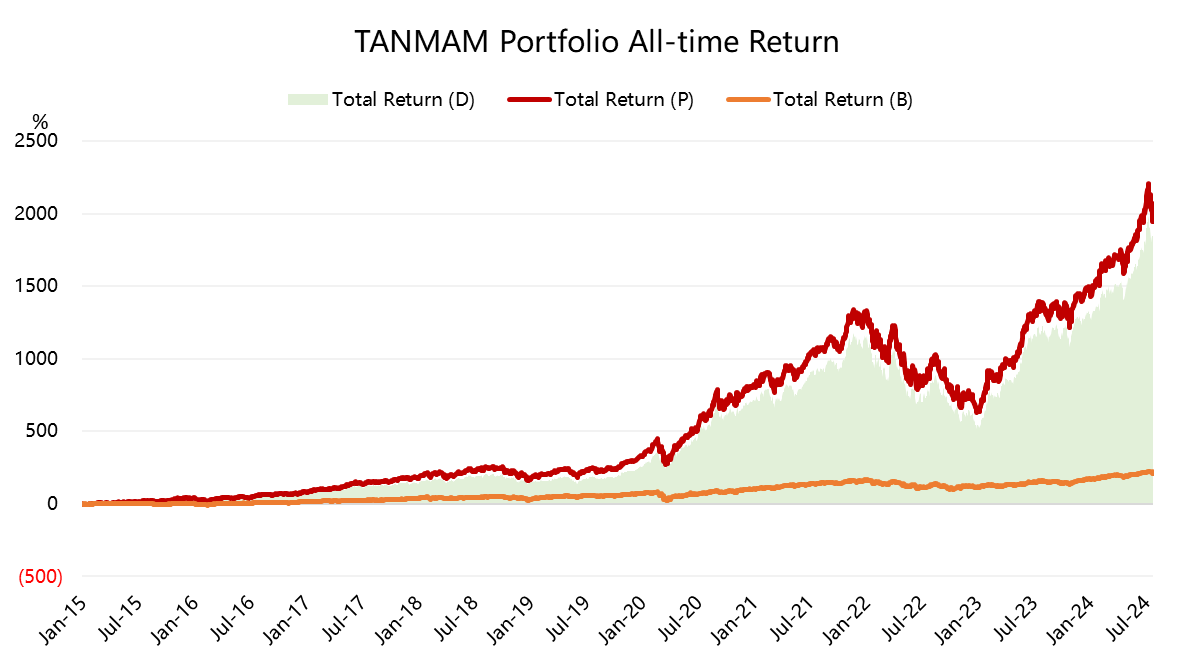

The Magnificent Seven form a portfolio (the "TANMAMG" portfolio) that is equally weighted and reweighted quarterly.The backtesting results are far outperforming the $S&P 500(.SPX)$ since 2015, with a total return of 1,945%, while the $SPDR S&P 500 ETF Trust(SPY)$ has returned 210% over the same period and continues to pull back.

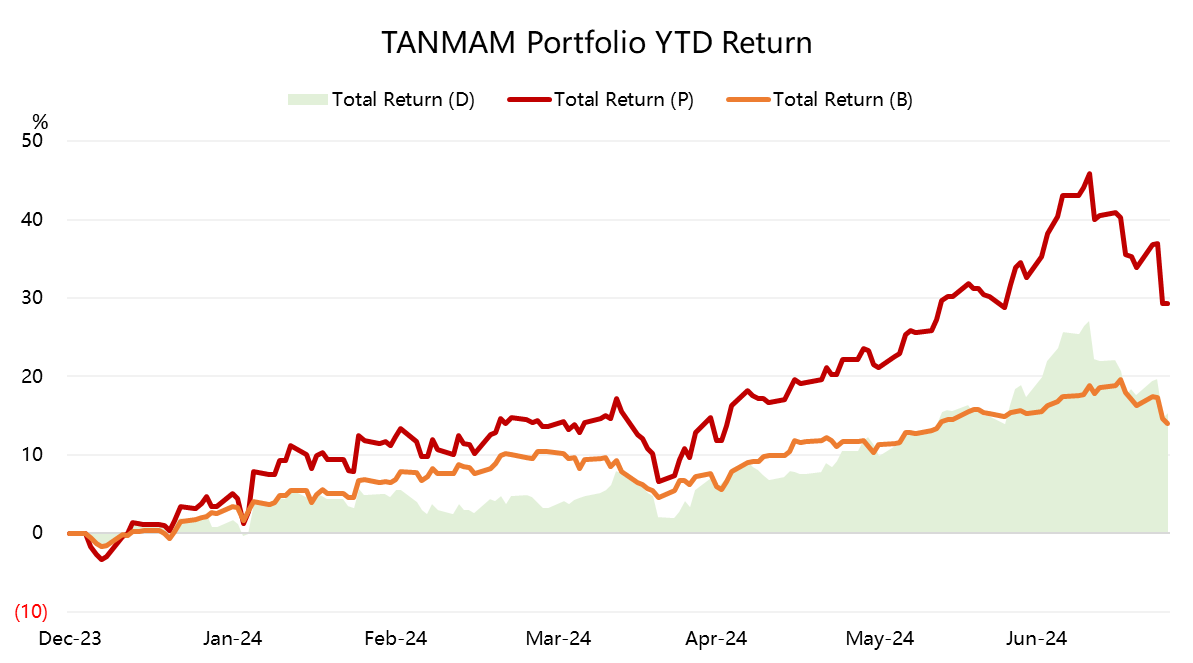

With the broader market hitting new highs this week, the portfolio has returned 29.27% year to date, outperforming the SPY by 14.00%.

Over the past year the portfolio's Sharpe Ratio has fallen back to 1.8 compared to SPY's 1.3 and the portfolio's Information Ratio is 1.4.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- twiddly·2024-07-26Awesome performance by the Big-Tech portfolioLikeReport