Will Pinterest Plunge Burden Meta's Q2 Earnings?

$Pinterest, Inc.(PINS)$ announced its Q2 results, and while the earnings report did its best to show strong user growth and revenue growth, it fell more than 15% at one point after hours as its Q3 revenue guidance missed market expectations.

Tube with AI support, advertising sales can be improved, but the industry-wide factors - the consumption of sluggish may further deteriorate the advertising market environment, which is not Pinterest a company can resist.The company's conservative expectations are also a wake-up call for the industry as a whole. $Snap Inc(SNAP)$ $Meta Platforms, Inc.(META)$

Revenue expectations for Q3 are $885 million to $900 million, below the market consensus estimate of $909.5 million.

Adjusted operating expenses to grow 17% to 20% to $485 million to $500 million

These factors have led investors to be cautious about future growth, resulting in a decline in the share price.

Investment highlights

AI-driven strategy and product development

AI-powered products and experiences: Pinterest has launched a variety of AI-powered products that have improved ad performance and user experience.For example, by improving search ranking algorithms and launching generative AI-guided searches, Pinterest has improved the relevance and personalization of content recommendations.Then there's Performance+, which helps advertisers optimize ad delivery and budget management.The company also introduced generative AI-guided search, which improves the user search experience and content discovery

Content Curation and Engagement: Pinterest enhanced its content curation capabilities with the introduction of new collage formats and enabled advertisers to utilize these features to create more engaging ad content.

Ability to Take Action: Pinterest introduced several new features to make the shopping journey easier for users, such as price, retailer and brand filters, and video shopping ads.

Regarding the Q3 guidance being below market expectations, the company responded as follows

Macroeconomic and Seasonal Factors: Changes in the macro market, especially the decline in consumption growth since the beginning of this year, make the advertising market still uncertain.Meanwhile, Q3 is usually a seasonal low point for Pinterest's business.

Strategic adjustments at the company level.The Company is moving forward with its full-funnel advertising platform, particularly strengthening its lower-funnel advertising products.These strategic adjustments may take time to fully show results.The company's stated intention to continue to invest in product innovation and user growth may also impact revenue growth in the short term, but in favor of the long term.

Changes in the competitive environment.The company alluded to the impact that increased competition in the advertising market could have on revenue growth.

In addition, Pinterest's major advertisers include brands in the home, food, craft, fashion, beauty and education industries, and consumer brands in this segment are entering the year with declining performance, and optional consumer products are entering a pullback cycle that could have an impact on the advertising industry.

Financial Performance

Revenue: $853.7 million, up 21% year-over-year, beating the market consensus estimate of $848.1 million.The company significantly improved advertising performance through its full-funnel advertising platform, particularly its lower-funnel advertising products

Net Income: non-GAAP net income was $207.2 million, up 46% year-over-year.A loss of $34.94 million in the same period last year turned into a profit of $8.9 million.

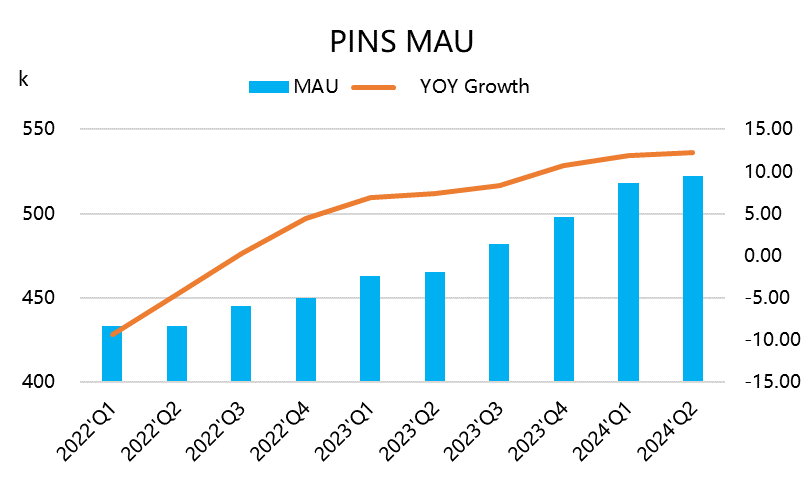

User growth: global monthly active users (MAUs) grew 12% to 522 million, beating market expectations of 518.04 million.

Regional Revenue and User Growth

U.S. and Canada: revenues of $673 million, up 19% year-over-year; 98 million monthly active users, up 3% year-over-year.

Europe: revenue of $143 million, up 25% year-over-year; 136 million monthly active users, up 9% year-over-year.

Other regions: revenues were $38 million, up 32% year-over-year; monthly active users were 288 million, up 17% year-over-year.

Average revenue per user (ARPU)

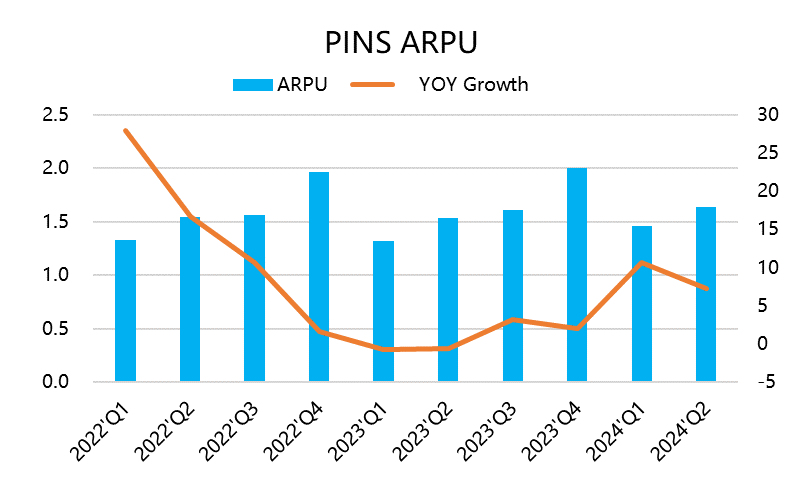

Global: Average revenue per user increased by 8%, from $1.53 to $1.64.

U.S. and Canada: average revenue per user increased 16% to $6.85.

Europe: average revenue per user increased 14% to $1.03.

Other regions: average revenue per user increased by 13% to $0.13.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- HarryCox·07-31Great earnings growth, impressive user growth, and strong regional revenue1Report

- AdelaideFox·07-31Great growth in user base and revenue! Impressive ARPU increase! [Applaud]1Report