Is Uber a defensive stock?

Uber jumped nearly 11% after reporting Q2 earnings and is one of the few consumer sector companies that can give investors confidence by outperforming expectations and passing guidance in the second quarter.

Investment highlights

Strong performance.

Gross Bookings increased 21% year-over-year (at constant currency), in line with trip growth.

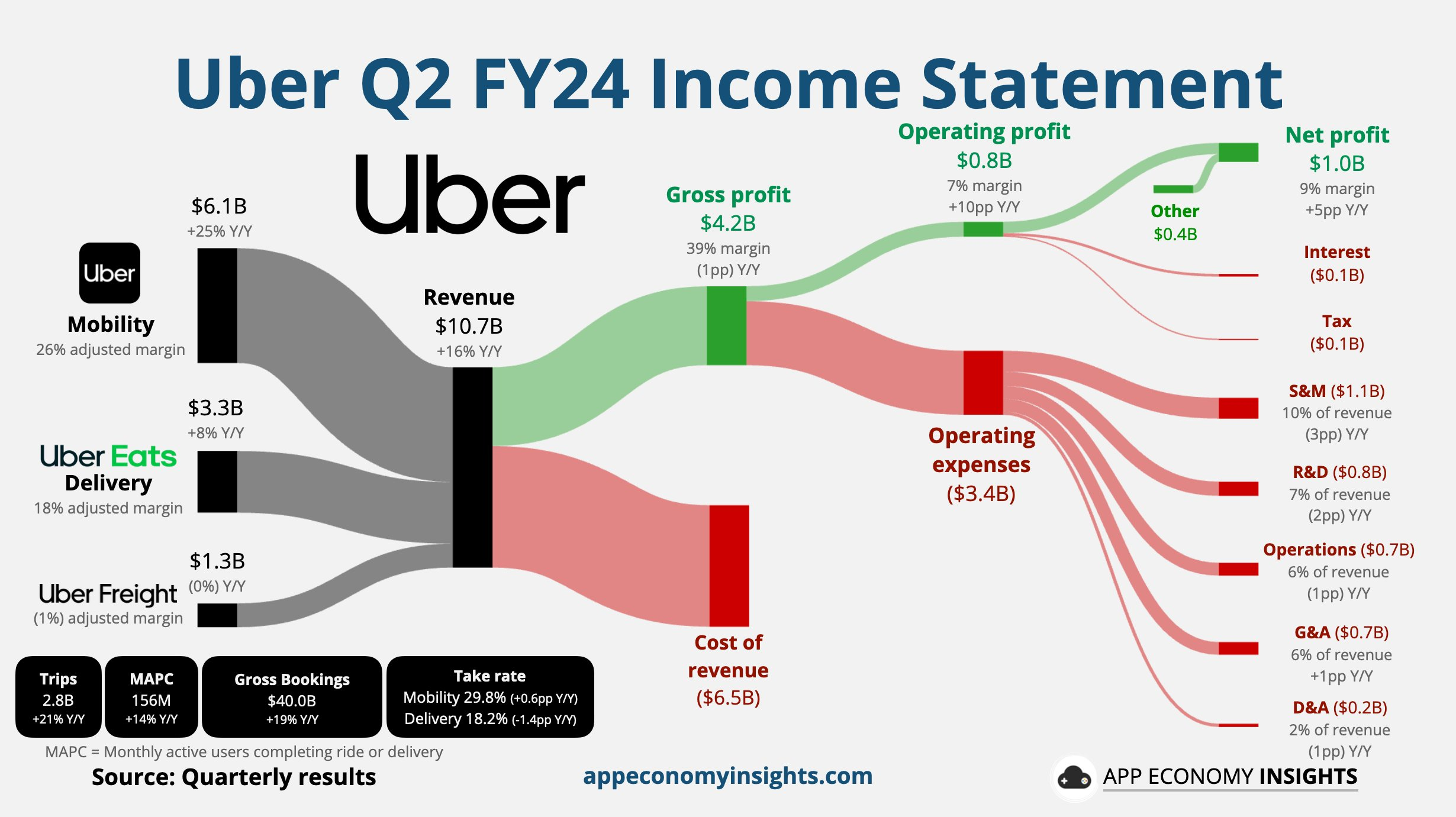

Revenue grew 15.9% year-over-year to $10.7 billion, well ahead of consensus market expectations;

Consolidated revenue from Travel and Delivery grew 19% year-over-year to $9.4 billion, or 20% on a constant currency basis;

Adjusted EBITDA increased 71% year-over-year to $1.57 billion, beating the market consensus estimate of $1.5 billion.

Free cash flow improved to $1.72 billion from $1.14 billion last year.

User Growth.

Expanding its user base by 14% to 156 million, and increasing frequency of use by 6%.

7.4 million drivers and delivery drivers worldwide.

Travel

Uber's consumer profile is strong, with a record-sized user base and record frequency of use, and total travel bookings up 23%.

Total trips booked grew 21% to 2.77 billion, ahead of the consensus estimate of 2.72 billion trips

No signs of weakness or downgraded spending in any income group were observed; management indicated that even if macroeconomic concerns materialize, Uber is confident that it will perform well because of the countercyclical nature of its platform.

Takeaway performance.

The number of first-time users of Uber Eats in the U.S. hit a new high for the past five quarters.

The Uber One membership program covers 50% of total takeout bookings.

Self-driving strategy.

Uber is in late-stage discussions with several global self-driving companies to join its platform.

Emphasized Uber's unique value to self-driving players, including high asset utilization and sophisticated go-to-market technology.

Established partnership with BYD to introduce more than 100,000 new electric vehicles in global markets.

Advertising Growth.

Advertising revenue now exceeds $1 billion annualized operating rate.

Ad spend in the grocery and retail businesses more than tripled year-over-year.

15% of Eats users now use the grocery service, an increase of about 200 basis points year-on-year.

Guidance.

The mobile travel business is expected to maintain mid-20% year-over-year growth (on a constant currency basis) in Q3 2024.Total bookings are expected to be $40.25 billion to $41.75 billion, compared to the general market expectation of $41.3 billion.

Meanwhile, the company said Q2 initial authorization to begin share repurchases while we continue to drive long-term shareholder returns.

Investment Highlights

About Autonomous Vehicles (AV)

The CEO said that while specific details are confidential, overall, self-driving players are significantly more likely to be utilized on Uber's platform than in the captive channel.Uber's marketplace technology improves fixed-asset utilization, and the incremental benefits of self-driving are expected to outweigh Uber's average 20% draw rate.The Company does not believe the self-driving market will be a winner-take-all situation, and Uber will continue to maximize marketplace mobility, combining human drivers and self-driving technology.

On the profitability of the takeout business and the realization of profitability in the grocery and retail businesses

Significant economies of scale in the takeaway business, with technological advances reducing the cost per transaction.Advertising revenues have grown significantly and refunds and reimbursement costs are decreasing.Lower customer acquisition costs, improved customer retention, increased advertising revenues and growing merchant volumes in the grocery business support the path to profitability in both the grocery and retail businesses.

New Growth Business, Advertising

Significant revenue growth in the advertising business, which has exceeded an annualized operating rate of $1 billion.Diversified product offerings and membership program Uber One membership program covers 50% of total takeout bookings, driving user frequency and dollars spent

Cycle-resistant defense characteristics, and consumer base.

Solid consumer base: Despite macroeconomic uncertainty, Uber's consumer base remains solid, with a record-sized user base and frequency of use.

Countercyclical nature of the platform: Uber's platform is countercyclical, with a greater supply of drivers helping to reduce rider costs and improve service reliability.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- popzy·08-07Great job on the analysisLikeReport

- cutzi·08-07Nice beatLikeReport