YTD 203%+ But Still In "Buy List"!

There's a gaming software stock that's up 203% year-to-date, but the market thinks its growth story isn't over yet.

Shares of the company fell to over $10 at the beginning of 2023 due to the high interest rate environment that has closed in on the suppressed advertising and gaming market, and have now risen to over $120.As the Federal Reserve has officially begun a rate-cutting cycle, this type of strong-performing growth stock could draw further coveted funding.

It’s $AppLovin Corporation(APP)$.

AppLovin's growth potential

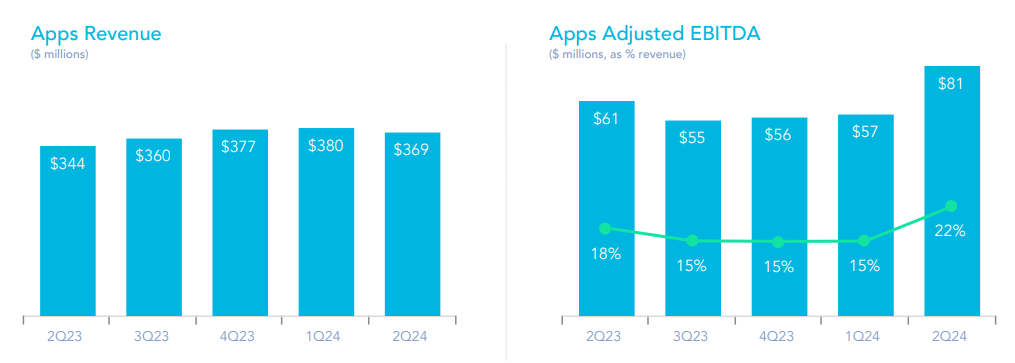

AppLovin's comprehensive software platform is becoming a key intermediary in the mobile gaming advertising space, and its success is largely due to its marketing software AppDiscovery

AppDiscovery is powered by AI-powered AXON technology, which effectively identifies potential users and improves their interactions with the app, and the impact of the AXON technology is just beginning, with the recent launch of AXON 2.0, which will make the model even more accurate as data accumulates, providing higher value to advertisers

Currently, its eDiscovery product installs are growing at an impressive rate, with Q2 results showing an increase in growth from 17% last year to 82% currently (87% in Q1 and 77% in Q2).

Outstanding gaming advertising partnerships and the prospect of entering other in-app advertising markets expected from the second quarter of fiscal 2024.Management stated that the software business is currently growing at 83% CAGR, with long-term potential in the range of 20%-30%, which will further improve cash conversion levels.

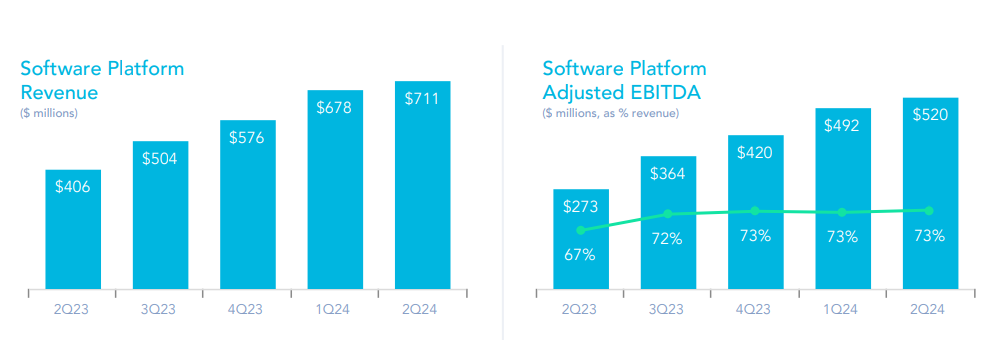

Margins will also continue to improve as AppLovin's software platforms progressively capture a larger market share, and its revenues are more efficiently converted into profit (EBITDA).

Whereas previously the software platform accounted for only 18% of Group sales and cash liquidity was low at the time, by H1 2024 the business will have accounted for nearly two-thirds of Group sales and cash liquidity will have improved to over 35%.

Financial performance

App's average revenue per active monthly user (ARPMAP) also grew to $52 (up 8.3 percent sequentially and 13 percent year-over-year), and the ad tech company reported a profit that exceeded expectations in its most recent earnings report, despite a decline in the number of active monthly users.

Adjusted earnings before interest, taxes, depreciation and amortization (adj EBITDA) margin of 55.6% (up 3.9 percentage points sequentially and 11.2 percentage points year-over-year)

GAAP EPS of $0.89 (up 32.8% sequentially and 304.5% year-over-year).

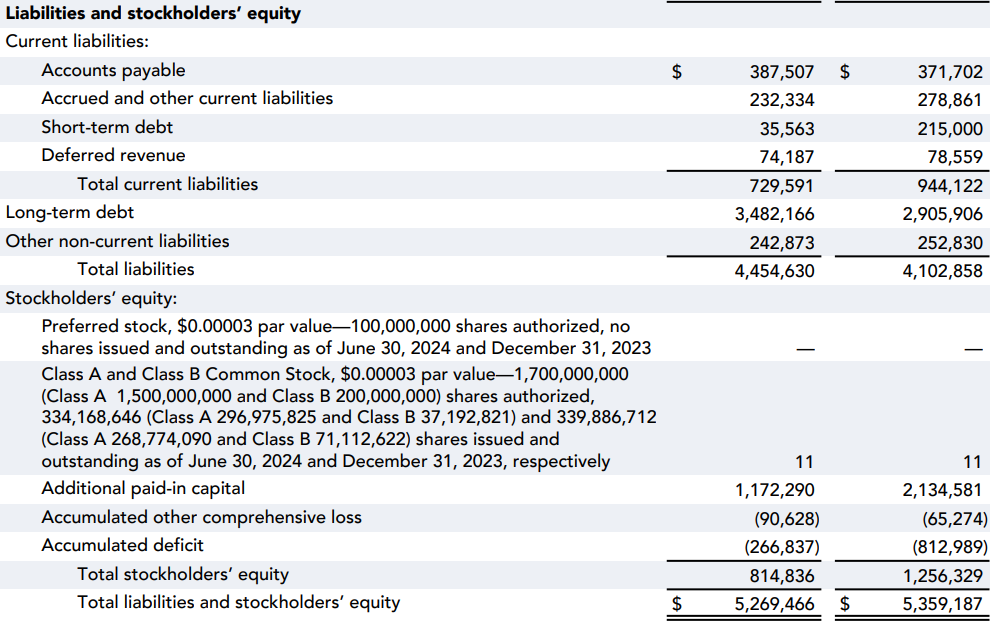

This is despite the fact that AppLovin faces high financial leverage, with the company's debt standing at approximately $3.55 billion as of the first half of 2024, equivalent to 4.3 times its ordinary share capital.However, since the second half of 2023, the company's operating profit has improved significantly enough to cover its interest expense, which is now more than 5x.

Note: The more indebted a company is, the more it will benefit from the interest rate cut cycle.

Valuation Analysis

With an average EV/EBITDA multiple of less than 12x over the past three years, the company remains a concern with a current forward-looking EV/EBITDA multiple of 16.8x, which is still below the industry average of north of 23.3.

However, this premium is justified by its positive EBITDA outlook.

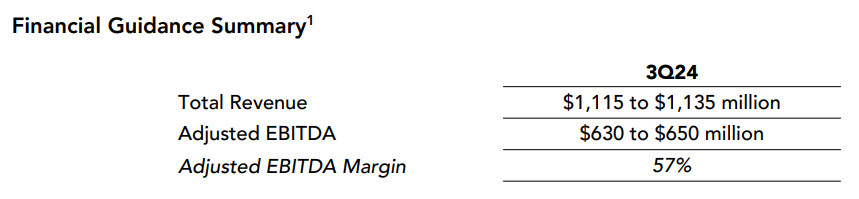

Management hinted at continued improvement in EBITDA margins in the third quarter, which are expected to reach 57%.

The market forecasts that AppLovin will post EBITDA growth of 15% and revenue growth of 13% in FY2025, and EBITDA growth of 16% and revenue growth of 14% in FY2026.

Summary

In summary, AppLovin stock remains attractive and therefore still worth buying due to the positive impact of AXON's technology on installed base, favorable EBITDA and cash flow outlook, and continued bullish market trends.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.