Earnings | Why Netflix didn't reach new high?

$Netflix(NFLX)$ was the first to report Q3 results after the bell on 18 October.The strength of its results is also indicative of the strength of the US economy, given the growing share of advertising revenue.

The only downside is that the Americas region, where the "shared account crackdown is almost complete", especially in Latin America, did not add as many users as expected.

Investment highlights

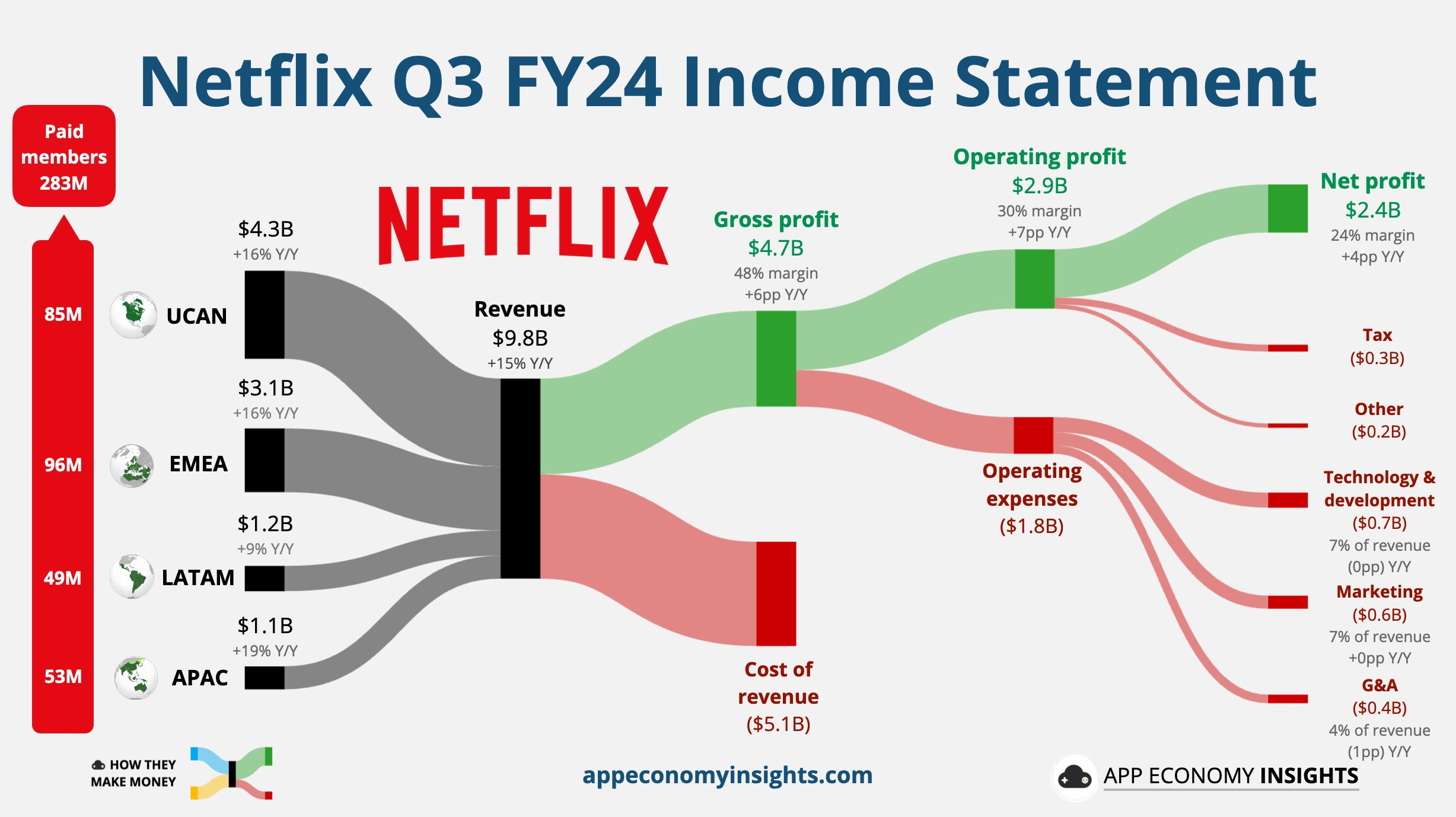

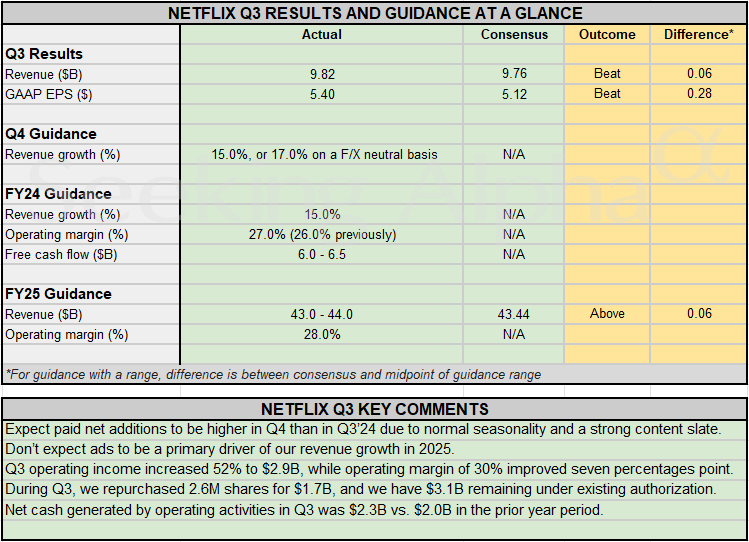

Revenue grew at a 15% year-on-year rate to $9,825 million, continuing a two-year high and beating market expectations of 13.5%.Nifty's 2024 revenue growth is dependent on the results of the crackdown on shared accounts and the growth of its advertising business;

Profit continued to outperform, with operating profit of $2,909 million, up 51.8 per cent year-on-year, well ahead of market expectations of $2,720 million and the company's guidance of $2,730 million, thanks to two things:

Growth in the high-margin advertising business;

Lower amortisation costs due to lower content spend from last year's writers' strike.

Guidance was raised slightly for the full year, with revenue growth for Q4 expected to be similar to Q3 at over $10bn, about 8% higher than the market's expectations, while the full year 2024 will be up 15%, at the high end of the 14-15% range for which guidance was given in Q2.Meanwhile, operating margins rose to 30% from 22% a year ago, bringing full-year expectations up to 27% from 26%, and to 28% in 2025.

Overall net subscriber additions of 5.07 million were above market expectations of 4.51 million, but SURPRISE varied widely by region.The US and Canada (+690k actual vs +700k expected) and Latin America (-70k actual + + +980k expected) missed expectations, while EMEA (+2.17m actual vs +1.44m expected) and Asia (+2.28m actual vs +1.56m expected) greatly exceeded expectations.ARPU also declined due to growth in lower priced regions and a larger share of lower priced ad accounts.

Paid subscriber growth in the US and Canada was largely in line with expectations, but also showed a lack of growth, which doesn't bode well for future price increases, and could conceivably be similar in Europe.

The unexpected decline in Latin America, which was much worse than expected, is also a wake-up call for the potential negative effects of the crackdown on shared accounts in "developing countries", and could be repeated in future additions in Southeast Asia.Those regions that are "unwilling to continue to pay for unshared accounts" tend to be more sensitive to price increases.

The advertising business has clearly become a driving force behind the company's revenue and profit growth, advertising users grew 35% YoY, even higher than the previous quarter's 34%, while in countries where advertising is available, about 30% of new registrations chose ad-supported packages, and in the overall market for ad packages, the proportion of users who chose ads has reached 45% or even higher.In terms of overall disclosed data, there are now more than 70 million advertised users, which pulls down overall ARPU but also raises expectations for advertising growth.

The rebound in free cash flow, in addition to improved operating margins, comes in part from the company's Q3 issuance of new debt.The full year 2024 cash flow target was raised from $5-6bn to $6-6.5bn due to a significant increase in investment in content starting this year, in addition to using $1.7bn to buy back 2.6m shares in Q3, and at this pace, the remaining amount can be repurchased for another 2 quarters.

The market is not without concerns, with the main point being that the 25-year margin expectations may not pan out.Margins are up significantly in Q2 and Q3, benefiting to some extent from lower amortisation from less content last year, while next year there is more uncertainty about margins because of higher amortisation.

Ad revenue may bring higher margins when it comes up as a percentage of revenue, but the ad packages themselves are depressing ARPU and face the dilemma of difficult price increases.

As it continues to invest in AI to improve advertising efficiency, Nifty is also not as big as $Amazon.com(AMZN)$ $Alphabet(GOOG)$ $Meta Platforms, Inc.(META)$ Big players like these have strong R&D capabilities, so it may be difficult to keep a lid on R&D expenses.

More heavy hitters, especially sports j programmes, have very high promotional expenditure and it is difficult to move big on marketing expenses.

In addition, the gap between the company's previous Q2 to Q3 guidance was too large, which also made investors' guidance for the company itself much less favourable.

Overall, the market's previous expectations for NFLX were very adequate, so such a big over-expectation after the earnings report, up at 5%, is lower than the pre-earnings IV implied 7.9%, such a situation, most of the call options are difficult to take profits.Of course, the new film season in Q4 is still something to look forward to, with the market already pulling out all the stops in anticipation of a second season of The Squid Game, but again, that's not something to look forward to when that's already built into the stock price, and it will all come back to haunt them in the event that it falls short of expectations.

In terms of current valuation, with a 28% margin expectation for next year, the current price implies a 31x PE expectation for 2025, which is quite high compared to the industry, as well as not too low compared to the big tech companies.

Earnings Review

Revenue overall revenue of $9.825 billion, up 15 per cent year-on-year, beating market expectations of $9.78 billion, after the company guided for 13.9 per cent year-on-year growth;

Operating profit was $2.909 billion, up 51.8 per cent year-on-year, well ahead of expectations of $2.72 billion and above guidance of $2.73 billion; operating margin was 29.6 per cent, up 7.2 percentage points year-on-year, higher than the market's expectation of 27.8 per cent and company guidance of 28.1 per cent

Diluted EPS of $5.40, up 44.8 per cent year-over-year, compared to analysts' expectations of $5.16 and company guidance of $5.10, and up 48 per cent year-over-year in the second quarter.

In terms of subscribers, paid streaming subscriptions grew by a net 5.07 million in the third quarter, down 42 per cent year-on-year, ahead of market expectations for an increase of 4.52 million, with a total of 282.7 million paid members at the end of the quarter, compared with analysts' expectations of 282.15 million.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.