Best Option Strategy For Slightly Declining Market?

Recently, a lot of users posting short orders of $NVIDIA Corp(NVDA)$ , but the strong stock price has made them swallow their losses after NVIDIA continues to make new highs.

Whether it's a game of "short-term pullbacks" or the anticipation of an "inflection point," options can often be used to make gains while reducing losses.Compared to naked shorting, buying Put and selling Call on a single leg, a combination of option strategies is often more suitable for investors with limited risk appetite.

In the case of PUT, for example, is there a strategy that can satisfy both:

Being bearish and short, with the opportunity to eat profits on retracements;

The ability to minimise losses and even still make a profit if things don't go as planned and the stock moves in the opposite direction;

Reduces premium depletion for the option buyer;

The answer is: yes.

Put Ratio Spread

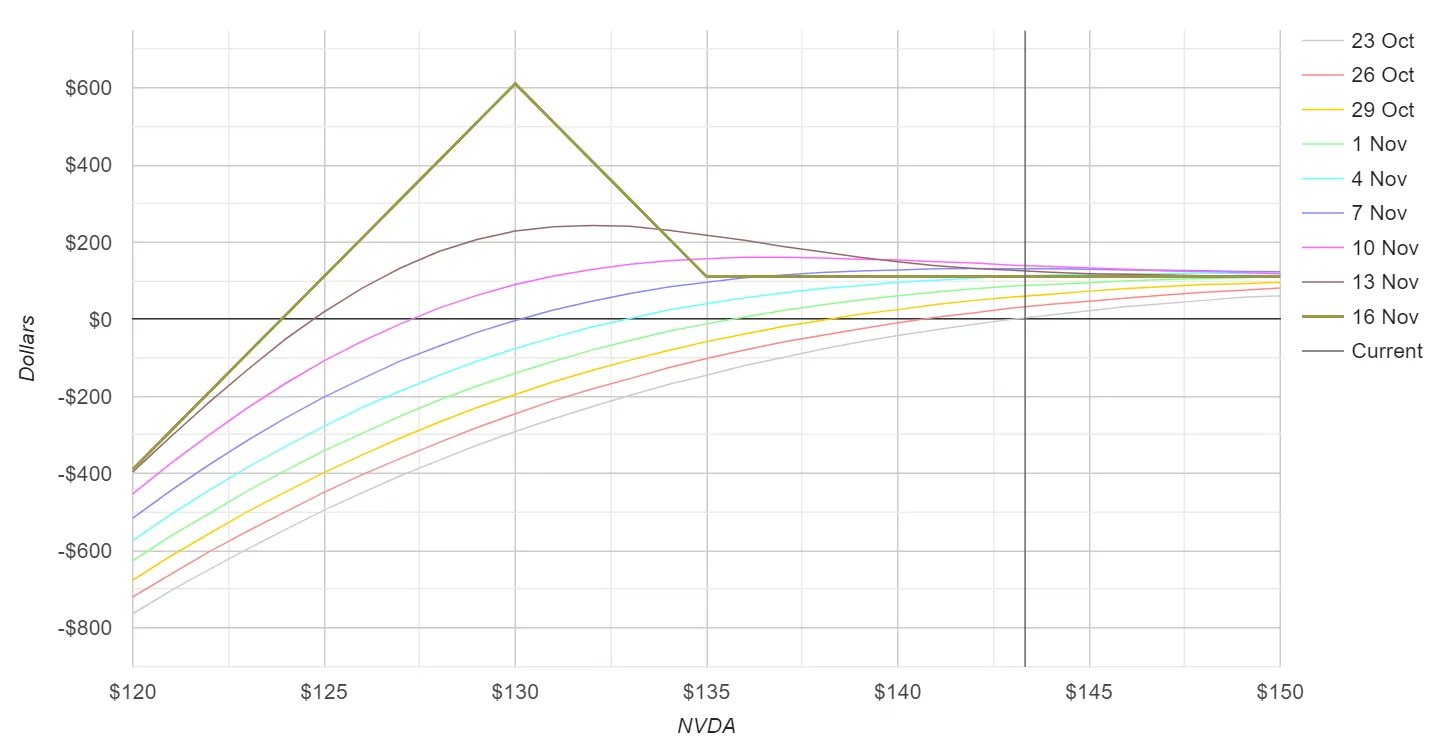

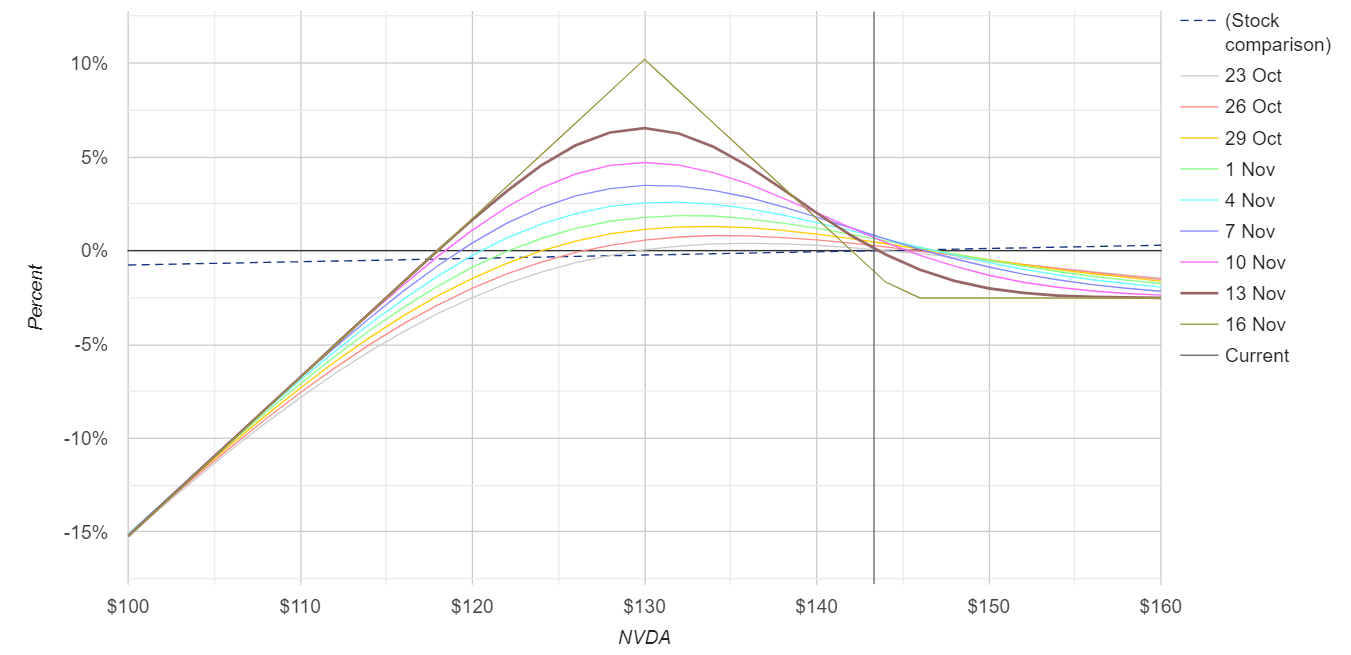

A Ratio Spread is an options trading strategy that involves buying and selling different amounts of put options.A put ratio spread is constructed by buying and selling different proportions of put options (usually on the same strike date).Example:

Long Put Leg: Buy 1 NVDA $135 put, exp 11.08

Short Put Legs: Sell 2 NVDA $130 put, exp 11.08

This spread strategy, which is slightly different from a normal spread, not only profits from "volatility" but also from "no volatility".

The profit curve of a strategy:

There is a profit peak: there is a peak in the profit and loss curve (usually the strike price of the sold option); if the stock remains stable or falls slightly, the result is more favourable than a naked put option.

Possible Loss: While the downside risk can result in unlimited losses as with naked put selling, the upside is capped, which protects you from potential losses during an uptrend in the market.

Characteristics of the strategy.

Ideally, a bearish ratio spread will take advantage of moderate changes in the price of the underlying to profit;

It is suitable for a neutral to slightly bearish view on the underlying;

To be clear, it is not necessary to follow the 2:1 ratio; investors can be more creative in choosing 3:1, 4:3, 5:4, etc., depending on their needs.At the same time, the risk will be characterised differently.

For the most part, this combination of options is a net seller (Credit), that is, it is the same as a naked Sell PUT; of course, those who have a stronger view of the downside and simply wish to reduce the cost of buying the PUT may choose to net less than a buyer with a seller option.Chart below:

Impact of Greek letters on option portfolios

Delta: The Effect of Underlying Price Movements

The impact of the underlying's volatility is dynamic. delta is initially positive in absolute terms, and the stock price may have some degree of unrealised loss if it falls early on, because the value of a long put option grows more slowly than the loss of two short puts.However, if the stock stays near the short strike price at expiration, the strategy will perform best, potentially maximising profits while limiting downside risk.

Theta: the effect of time decay

Time decay works in favour of put rate spreads.As time passes, the time value of an option decreases.This decrease helps to reduce the value of the two short put options.Ideally, there is minimal movement in the underlying stock, allowing for significant erosion in time value near expiration.This decline may allow you to repurchase short puts at a lower price than you initially received, while long puts maintain their intrinsic value.

Vega: The Impact of Implied Volatility

Lower implied volatility is favourable for put rate spreads.Lower volatility reduces option premiums, which is beneficial when spreads are initiated at higher volatility levels.As implied volatility declines, the value of a short put option falls faster.While implied volatility is unpredictable, it is critical to understand its impact on option pricing.

Some personal understandings

In a net seller (Credit) situation, it is appropriate to be mildly bearish while eating volatility losses;

In the case of low risk appetite, choose the right ratio as well as the strike price to leave enough room for downside;

Remain optimistic about the underlying itself and hopefully intend to bottom out at certain extreme declines

Don't use it for underlying stocks or scenarios with particularly high VaR (e.g., risky events such as earnings reports), which may cause unnecessary pressure on margins in an instant.

It is more suitable for individual stocks with volatility but stable fundamentals that have a need for a pullback, or large-cap ETFs, etc. (e.g. $S&P 500 ETF(SPY)$ $Nasdaq 100 ETF(QQQ)$ $Russell 2000 Index ETF(IWM)$</a10> )

Supplementary

Two Direction Put Ratio Spread

I. Forward Put Ratio Spread (Front Put Ratio Spread)

Same as the above strategy, the strategy of choice when the market is stable to slightly bearish.It consists of establishing a put debit spread and adding an additional short put option at the same strike price as the short side of the debit spread.

Structure: Buying a put debit spread and selling an additional put option at the short strike price.

Net Seller: This strategy usually starts with a net credit to the trader.In effect, you can manipulate the option to take a credit or debit position.

No Upside Risk: Assuming you start the trade with net credit, you will not be at risk if the price of the underlying asset rises significantly.

This strategy benefits from small price declines because the additional short puts help offset the cost of the spread.The goal is to capture time decay and premium, maximising profits if the stock closes close to the put's strike price.

II. Reverse Put Ratio Spread Strategy (Back Put Ratio Spread)

The opposite of the Call Put Ratio Spread strategy, where more options are bought than sold, this is a more aggressive stance with increased costs but greater profit potential.

Structure: Sell one put option and buy two further out-of-the-money puts.

Net debit: This setup usually results in a net debit.As in the case we mentioned earlier, you can manipulate the option to create a net debit or net credit position.

Unlimited Profit Potential: Typically, this strategy starts with a net debit because it means that the additional options bought provide the opportunity for unlimited profits when the stock price falls.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- BellaFaraday·2024-10-23Awesome strategies for a slightly declining marketLikeReport