Will CapEx Expansion Kill META?

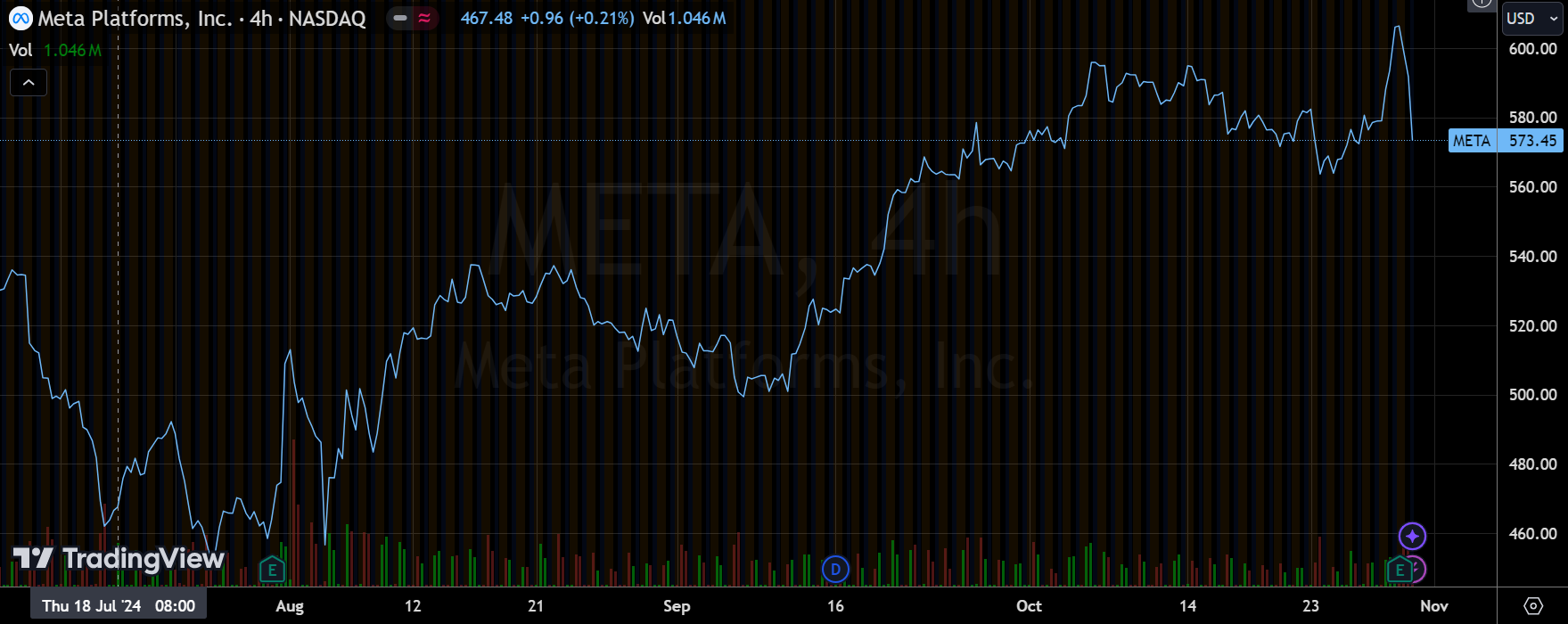

Due to the volatility in the $Meta Platforms, Inc.(META)$ earnings market in previous quarters, META's expected volatility is the largest of the "Mag 6" volatility in the Q3 earnings season, which is usually in the 10% range.A fluctuation of 10% or more is not uncommon.Since META is currently the "Mag 7" company with the highest share price per unit, the relatively light trading on weekdays will emphasize Earnings' amplified sentiment.

However, after reporting 24Q3 earnings after the bell on October 30th, META is down only about 3%, with a high probability of an option double dip.

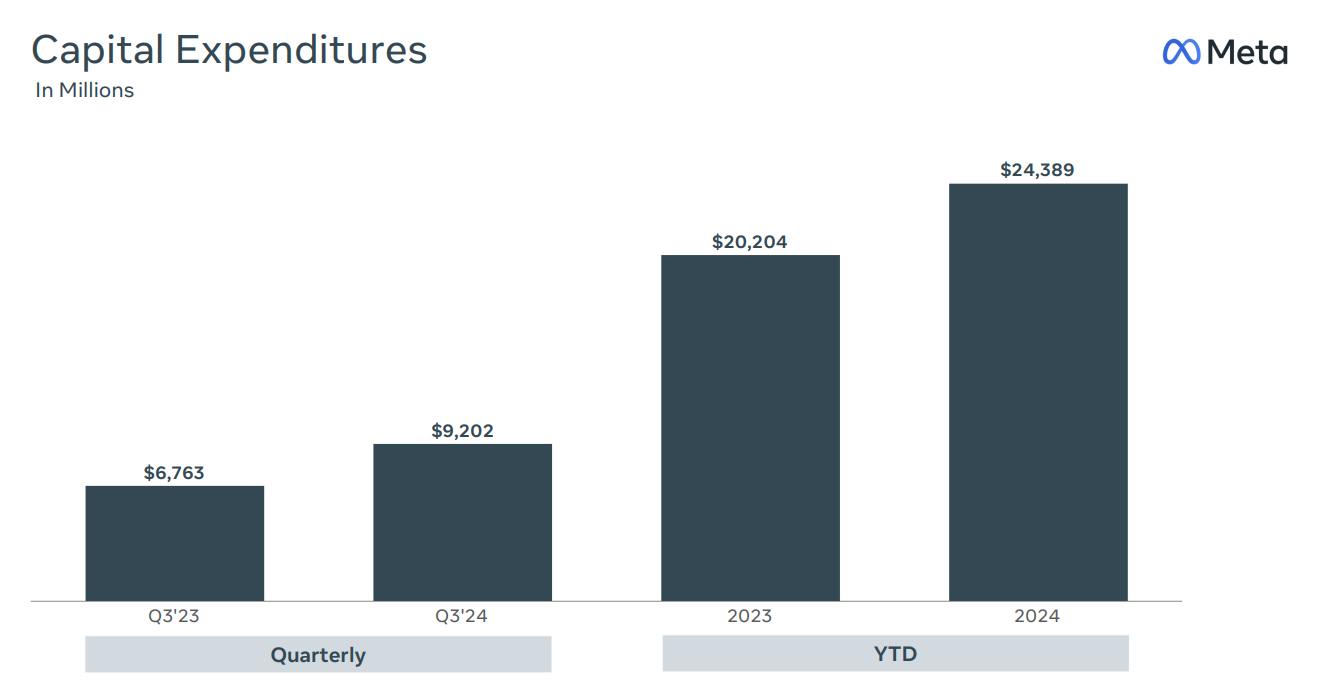

At the same time, guidance has been relatively solid, and while capex continues to be revised upwards and plans for continued upward revisions in FY25 have also been made public, investors seem to have gotten used to META's spending and have come to expect the same from its AI side of the program, so there has not been the same kind of crash crash crash that was seen in Q1.

Investment highlights

Open source end: revenues were solid amidst high expectations, and guidance didn't pull the crotch.

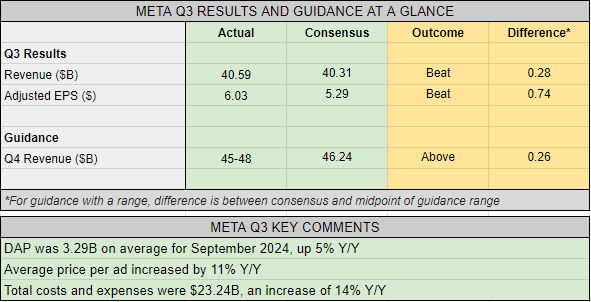

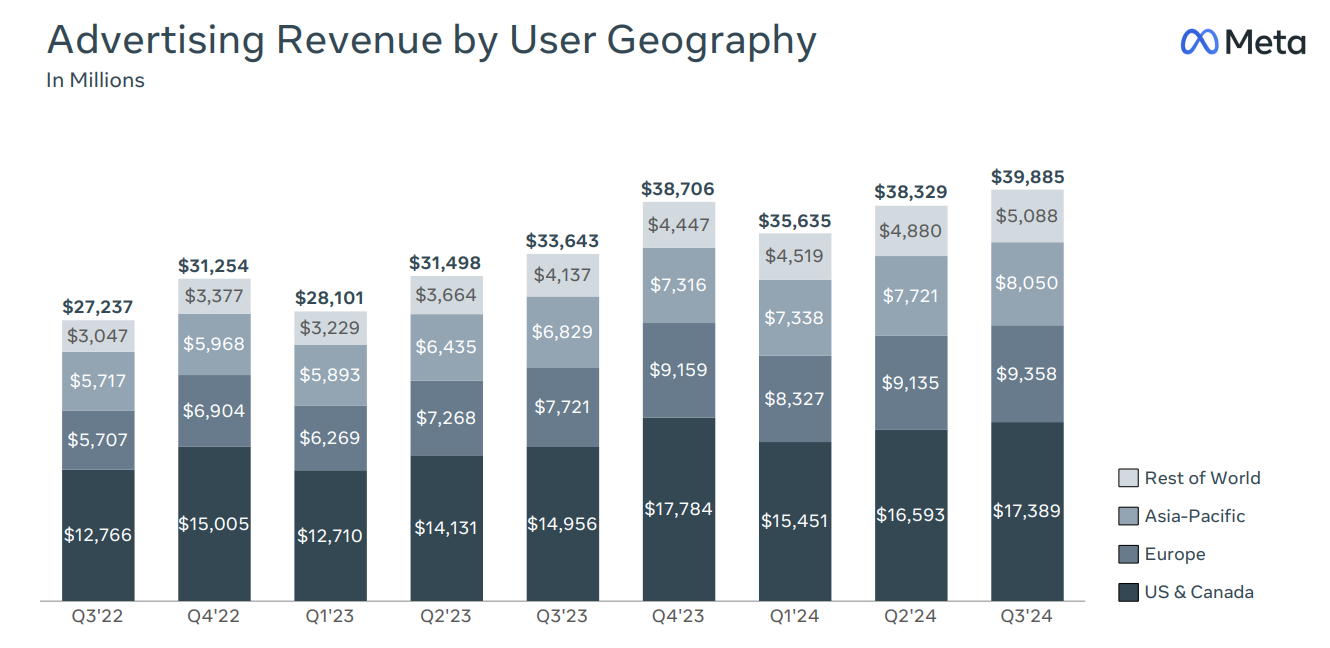

The company's Q3 revenue came in at $40.59 billion, up 18.9% year-over-year and above the market's expectations of $40.25 billion, which was also basically made up of advertising revenue.This growth rate was not easy to achieve as last year's Q3 growth rate was 24%, which is quite a high base.

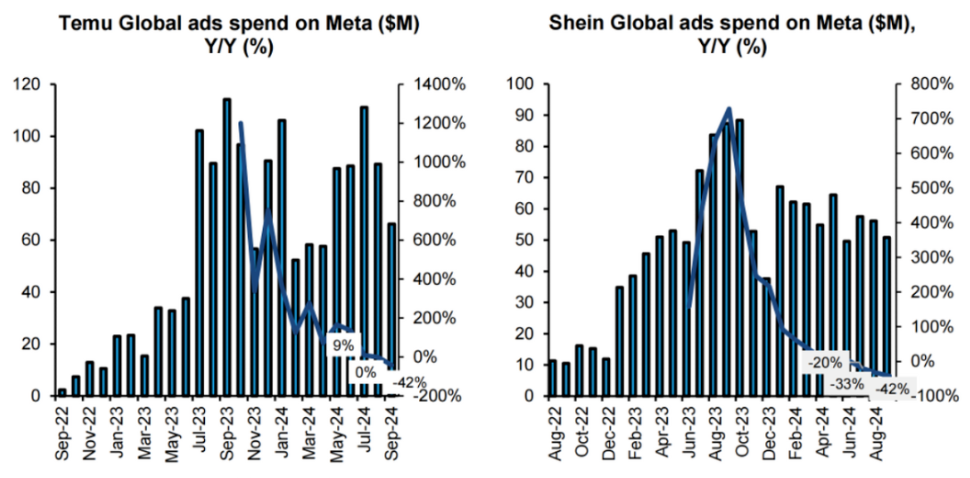

Contributions from overseas e-commerce companies, including Temu, Shein, and other cross-border e-commerce companies that must be invested; META's huge number of active users is the biggest guarantee as brand ads are more focused on scale effects, but relatively speaking, small and medium-sized merchants are more focused on ROI, and therefore the variation will be a bit bigger.Judging from the trend in recent months, Shein has slowed down its spending due to its blocked IPO, and Temu is unlikely to increase its placement budget again.

Efficiency is improved through Meta Advantage+, an AI-integrated advertising algorithm tool.Mainly enough to provide more exposure to newly added or underperforming creatives, thus improving overall ad performance.It's also a hedge against ATT (Apple's App Tracking Transparency Policy) for META

political platform advertising in an election year.Mark Zuckerberg's unsolicited mid-year revelation about Biden's Fake news at the time of the selection also reflected to some extent the market's expectation that Trump would be in charge again, and served to alleviate the pressure for favoritism in political ads.From this perspective, META also left itself a way out, in addition, with X.com's Elon Musk after the clear support of Trump, Harris supporters are likely to switch to Threads more.

On the savings end: depreciation and amortization costs loom larger, and capital expenditures remain unabated.

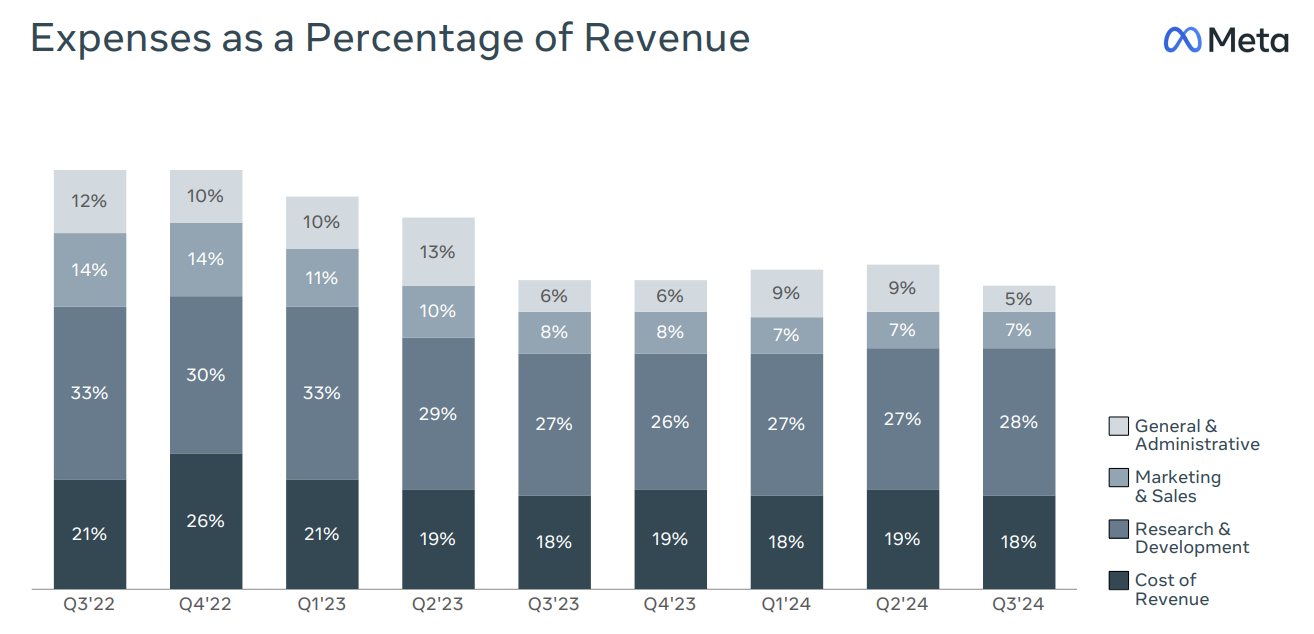

Q3 operating profit reached $17.4 billion, up 26% year-on-year, still higher than the rate of revenue growth, indicating that the current profit margin is still within the acceptable range of the time position.However, at the same time, depreciation and amortization cost pitfalls from excessive capex are gradually escalating.

At the same time, executives said in 2025 back to continue to raise the capital expenditure guidance, although the market on the "high capital expenditure" has been expected, but the current expectations of only $45 billion, if more than, or to reach more than $50 billion, will still be expected to hit the stock price hard.

The depreciation and amortization of capital expenditures increased by 40% in Q3, much higher than the rate of revenue growth.With this trend, next year's margins will be more or less affected.

Meta-universe division Reality Labs continues to lose money, Reality Lab's revenue of $270 million was up 29% year-over-year, but below market expectations of $310 million.Operating losses were $4.4 billion, and cumulative operating losses since 2020 have exceeded $58 billion.

Although the Quest VR headset and Ray-Ban Meta smart glasses are the highlights of Q3, the entire VR industry still needs to wait for more mature products to pave the way for a developer ecosystem, and Apple's Vision Pro has basically flamed out and cut orders.

However, the market's expectations of the VR business is not high, as long as it is not a serious loss affecting profitability, investors will not put this part of the valuation Price-in, the short term to reduce losses as a more practical goal.

Can the existing valuation be maintained?

In terms of profit multiples, META is no longer the lowest in Mag 7 (Google below), The short-term forward P/E on a closing basis is 25x, which should correspond to around 23x in 2025.

But the current market expectations for META is relatively bursting, and the singularity of the business makes its advantages (native Facebook Family user volume) and disadvantages (phasing out of the dividend) are obvious.In particular, META is very much eating changes in macro factors, with incremental new ads being the focus of investor attention and spending on e-commerce on the consumer side decreasing.That's why the company is betting on AI (e.g., the recent AI search engine) as well as lead generation (Threads) at all costs

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.