What's Apple's Surprise in Q4 Earnings?

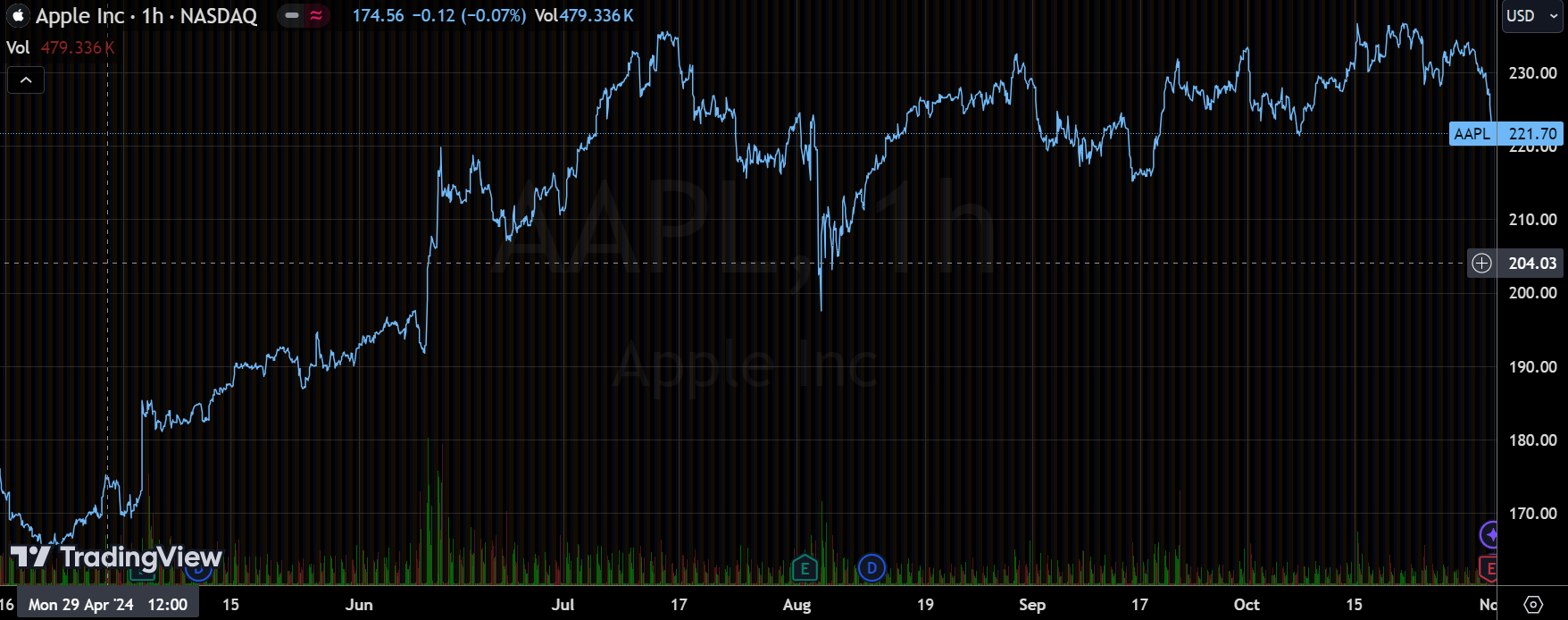

$Apple(AAPL)$ Q3 earnings report, while a small beat, didn't surprise the market too much, dropping 1.8% after hours in a big pullback for the broader market as a whole, back to before last quarter's earnings report, which was almost a full quarter without too much volatility.

I. Financial data performance

Revenue and Profit

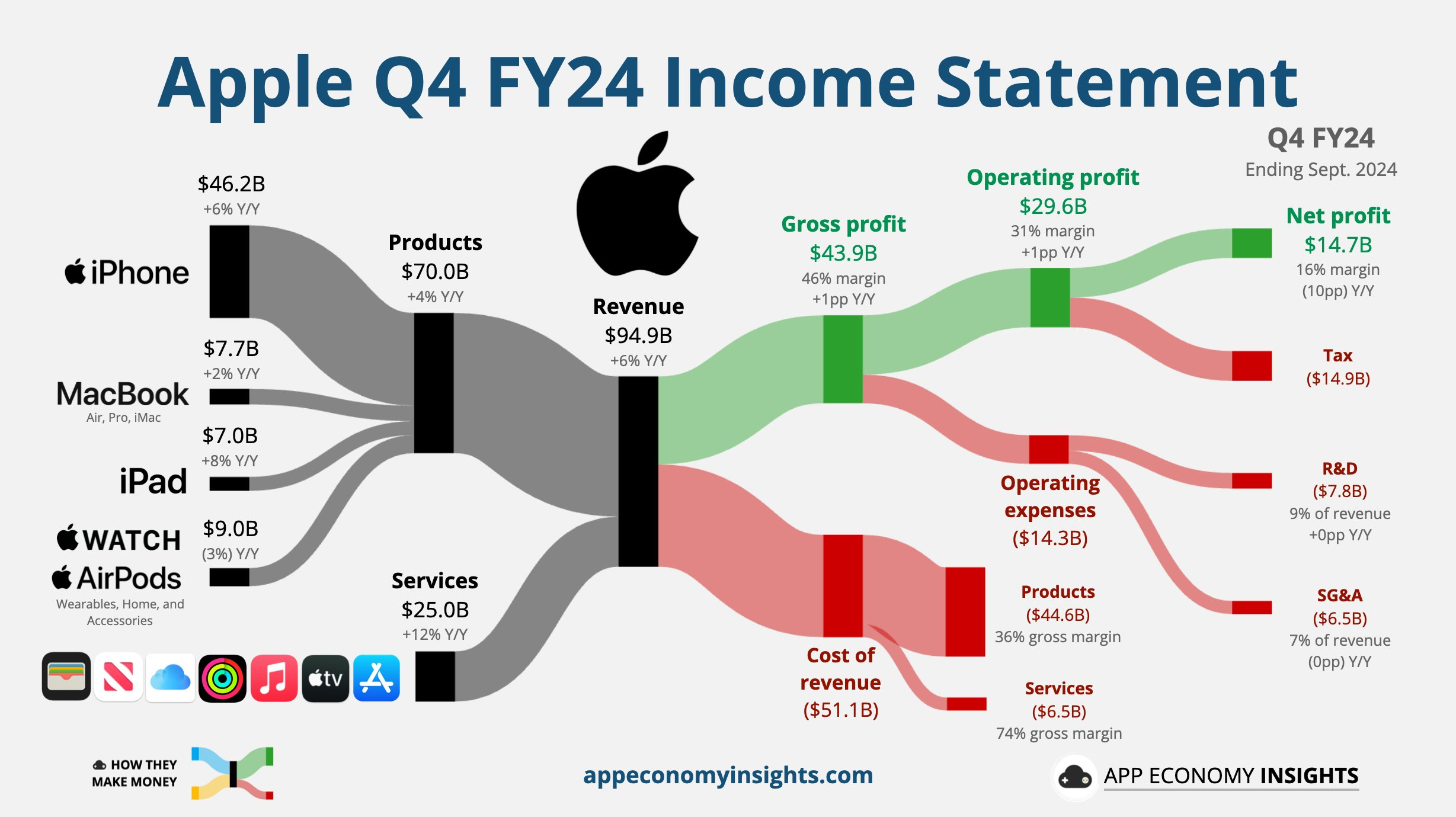

Total Revenue: Revenue for the quarter was $94.9 billion, an increase of 6.1% year-over-year, above market expectations of $94.36 billion.

Gross Profit Margin: Gross profit margin was 46.2%, largely in line with market expectations, and the company had solid cost control.

Net profit: After taking into account the US$10.2 billion EU back tax, net profit was US$14.74 billion, down 35.8% year-on-year; excluding the impact of back tax, adjusted net profit was US$24.9 billion, slightly exceeding the market expectation of US$24.3 billion.

Earnings per share (EPS)

GAAP EPS declined to $0.97 in the third quarter, down 33.6% year-over-year, due to the impact of back taxes; excluding taxes, non-GAAP EPS adjusted to $1.64, up 12.3% year-over-year, and better than analysts' expectations of $1.58.

Operating Expenses

Operating expenses for the quarter were $14.29 billion, up 6.2% year-over-year and slightly below market expectations of $14.35 billion.

II. Core Business Segments

iPhone Business

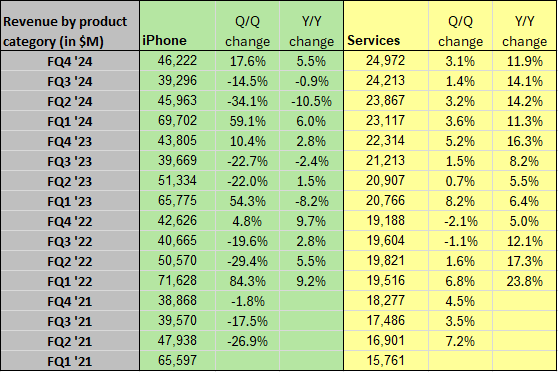

iPhone revenue for the quarter was $46.22 billion, up 5.5% year-over-year, and exceeded market expectations of $45.04 billion. iPhone 16 series launch boosted sales and average shipment price, which increased significantly from the same period last year, leading to a continued rebound on the hardware side.

The launch of the iPhone 16 series, the first to feature a 3nm chip, enhanced the performance of the phone and strengthened its core position.iPhone revenue grew more strongly despite competitive pressure from Huawei and others in China.

Mac and iPad Business

iPad: iPad sales of $6.95 billion, up 7.9 percent year-over-year, were slightly below expectations of $7.07 billion.The release of the new iPad Air and iPad Pro boosted sales growth, reflecting the rebound in demand in the tablet market.

Mac: Revenue from the Mac business was US$7.74 billion, up 1.7% year-on-year, in line with market expectations.However, shipments declined, mainly due to users waiting for new products with the M4 chip.

Wearables, Home & Accessories

The segment reported revenues of $9.04 billion, down 3% year-over-year, a weaker-than-expected performance.Despite the launch of the new AirPods range, it failed to reverse weak demand. the non-market launch of the Vision Pro mixed reality headset also limited revenue growth potential.

Services Business

Service revenue of $24.97 billion increased 11.9% year-on-year, slightly below market expectations of $25.27 billion.Gross margins remained high at 74%, with services revenue having accounted for 26% of the company's total revenue and contributing 44% of gross profit.

Although growth has slowed down, the service segment is still an important source of profit for the company.However, the market's regulatory risk on the App Store still exists, which may put pressure on the growth rate of the service business in the future.

Market Performance

Greater China

Revenue in Greater China for the quarter was $15.03 billion, down 0.3% year-on-year, a markedly narrower decline. Although it fell short of market expectations, the performance improved compared to the 6.5% decline in the previous quarter.

Apple's market share in China was put to the test due to domestic competitive pressures, especially in the high-end market.

Investment highlights

FUTURE OUTLOOK: Apple is guiding more conservatively for fourth-quarter revenue, which is expected to post low-to-mid single-digit year-over-year growth, weaker than the market consensus estimate of 7%.Management said demand could slow during the holiday shopping season.

Profit margins improved steadily, benefiting from the rising share of services.Overall gross profit margin was 46.2%, an increase of 1 percentage point year-on-year, basically in line with the market's consensus expectation of 46%, with the margin of software services rising and maintaining at a high level of 74%, and the hardware portion falling back to 36.3%, while operating profit of $29.6 billion was up 9.7% year-on-year.

Apple's performance in the quarter met the market's basic expectations, with the hardware business performing steadily, supported by growth in the iPhone and iPad.Despite the downturn in wearables, growth in the services business remained solid and was a key pillar of the company's revenue.

Net income for the quarter was impacted by EU back taxes, but excluding that impact, actual earnings were favorable and the company's stock has a high P/E ratio, reflecting the market's expectations for its future AI applications.

Valuation.For the full year, with $103.9 billion in operating net income for fiscal 2024, the current P/E ratio of about 33x and forward P/E ratio also remains above 30x, which is not too low.For companies maintaining single-digit growth, the market's valuation of Apple at more than 30x reflects expected support for the company's AI hardware and future realizability.Future upside potential for the stock also relies on the company delivering more substantial outperformance on key products and innovations, especially service performance revenues that incorporate AI.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- AuntieAaA·2024-11-01GoodLikeReport