How Amazon Improved Q3 Margin?

$Amazon.com(AMZN)$ reported earnings for 2024Q3, jumping more than 6% after hours after investors didn't count too much on higher capital spending amid overall revenue beat expectations, a big jump in profit, further cash flow consolidation and healthy guidance.

As the last of the big tech companies to report this week, Amazon is more of an indicator of the strength of the economy through the activity of retail activity.In the "AI Race" unit, AWS performed moderately well, with neither the growth trends of $Alphabet(GOOG)$ nor the share concessions of $Microsoft(MSFT)$ , while margins improved dramatically (with a change in depreciation life);

In the overall economy "soft landing" or "no landing" expectations, investor expectations for retail spending is also relatively strong.Of course, the impact of Q3's decline in the U.S. dollar also allowed the global retail giant to eat a wave of exchange rate benefits;

Rising margins also further support AMZN's valuation, with forward P/E expected to return to around 28x in 2025.

Investment points

AWS, though not accelerating beyond expectations, has multiple factors for margin lift.

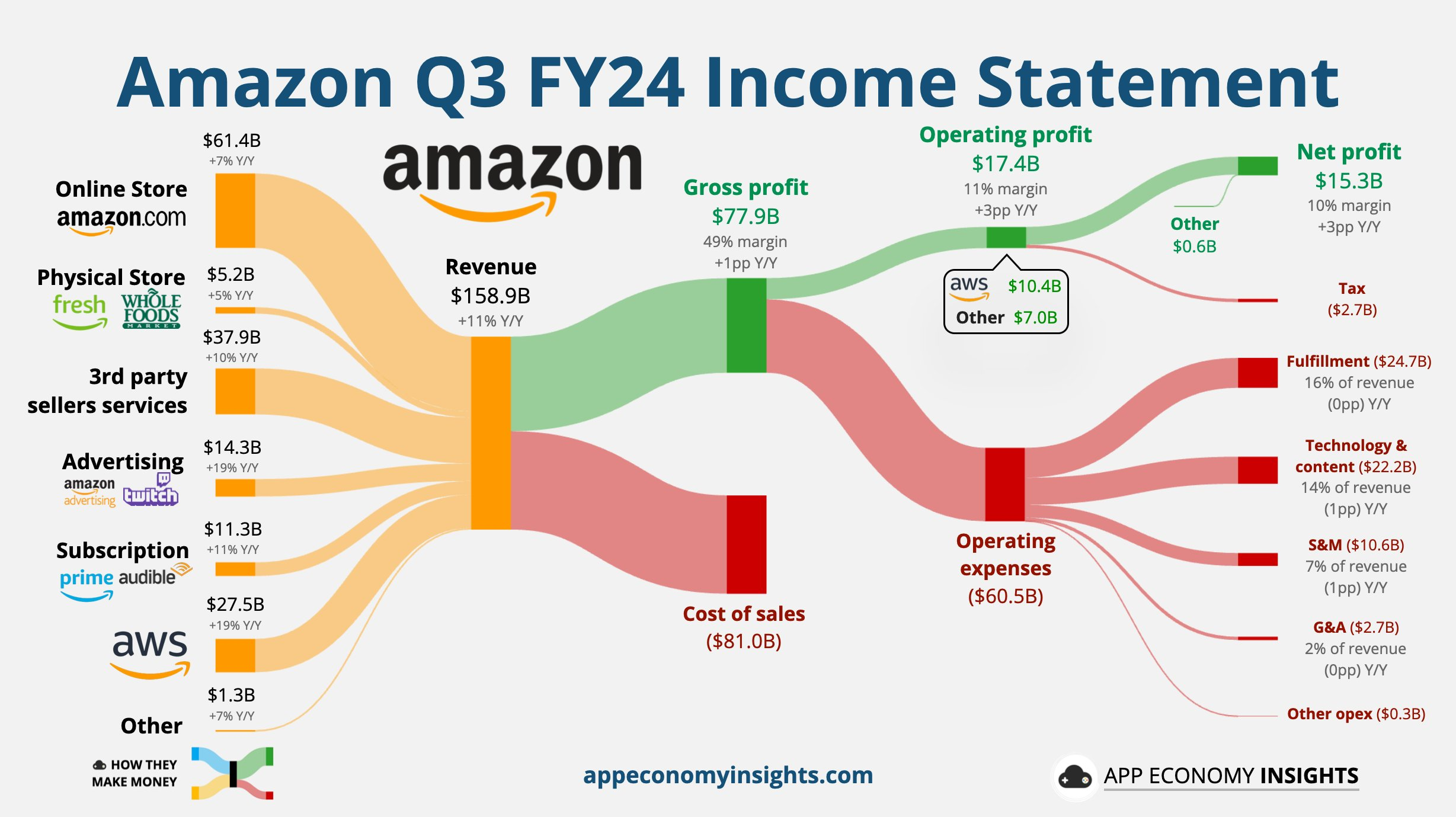

This quarter's AWS year-on-year growth of 19.1% to $ 27.45 billion, slightly weaker than the market's expectations of $ 27.49 billion, compared with last quarter's only a slight acceleration of 0.4%, and did not prove that the demand for AI to drive the cloud business "outbreak".

At the same time, the market's AI expectations may be higher, and in the previous Google Cloud accelerated upward trend, the expectations are more optimistic, but in fact did not show speed.Considering AWS' number one ranked volume, the current growth is not low.

AWS' operating margin improved again, to 38.1%, and was a major contributor to further strengthening the company's finishing margins.

The company said it was "increasing the estimated useful life of servers" that boosted margins by 2%, with a limited timeframe for the impact of the change in depreciation life, and it also said that future margins may fluctuate as well;

Of course, excluding the 200 basis point impact, the actual margin was around 36%, which was also much higher than the market consensus estimate of 33.4%, indicating that the impact of depreciation and amortization was offset;

The company's profit margin improvement through operational efficiency improvements such as layoffs is also more pronounced, and this part of the impact is long-term.

Retail segment growth accelerated and margins to fell back up.

Online retail revenue of $61.4 billion, up 7.2% year-on-year, exceeding market expectations; three-way retail growth was 10.26%

Advertising revenue increased 19% year-over-year to $14.3 billion, which was in line with market expectations, but slightly weaker than last quarter's 24% growth;

Compared to the 8.7% growth within the U.S., the international business growth rate returned to double digits again at 11.67%. Of course the weaker U.S. dollar in Q3 had a 3% impact from the exchange rate factor alone.Meanwhile operating margin reached an all-time high of 3.6%, which could also be attributed to the impact of exchange rates.

Subscription services revenue growth also improved by 1.1%, with Prime Video contributing with relative stability in terms of overall subscriber hours in 2024.

Initiatives such as the Rufus generative AI expert shopping assistant, the Amelia program and AI shopping guides during the quarter helped consumers make better shopping decisions.

Overall margins hit a new high and capital expenditures exceeded expectations and hinted at further increases next year.

Q3's capex increased to $22.6 billion, up over 81% year-over-year, while the full year 2024 cost about $75 billion;

The high investment in capital expenditure is not yet reflected in the financial results through depreciation, so the impact on profits is still limited, but combined with management's "margin fluctuation" rhetoric, the impact may increase in the future.

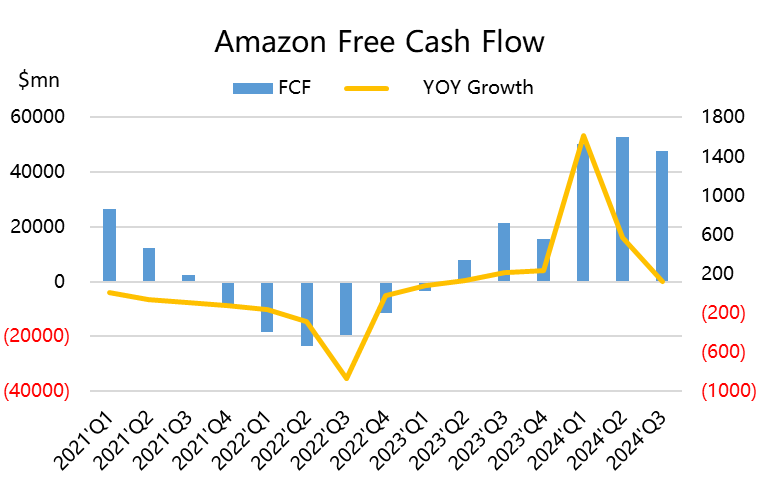

From the point of view of the company's declared free cash flow, Q3 was 47.8 billion U.S. dollars, down from more than 50 billion U.S. dollars in the last two quarters, combined with the company's capital expenditures to increase the point of view, the improvement in profitability did not obviously bring incremental increase in FCF, it seems that AWS "change in depreciation algorithms," as well as international retailing brought about by the exchange rate fluctuations factor influence.More.

In terms of guidance, Q4 revenue is expected to be $181.5~188.5 billion, median slightly lower than the market's expectation of $186.4 billion, but at the profit level operating profit guidance of $16~20 billion is significantly higher than the market's expectation of $17.5 billion.

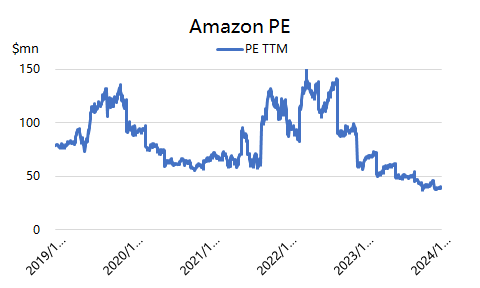

The company's dynamic PE has come back down to 38x due to improved margins , and following this trend, the forward P/E for 2025 is expected to come back down to around 28x, on par with other major big tech companies.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.