Kroger's Potential Future Without Albertsons Is Improving As It Adapts To Bifurcation

- Given Albertsons' significant discount to Kroger's merger price, it appears highly unlikely that the deal will be completed.

- With the FTC's effort to ensure the merger lacks pricing power advantages, I believe KR is better off without the debt-laden company.

- Kroger may benefit if ACI closes stores or lay-offs employees, as it has suggested as a long-term result of a failed merger.

- Lower agricultural input costs lift the Company's gross margins, but to improve its market position, it needs to vertically integrate and invest in private-label branding.

- In the long run, Kroger will likely need significant investment to adapt to consumer bifurcation trends, which benefit wholesale and premium grocers more than those "stuck in the middle."

jetcityimage/iStock Editorial via Getty Images

Kroger (NYSE:KR) has faced years of stagnation as the FTC hangs its merger deal with Albertsons (ACI) in the air. The deal would sell ACI for around $27 per share, but it is now around $18 after falling 22% this year, implying the merger is unlikely based on its deal spread. Other analysts place the odds below 20%.

As I discussed in May, I view the merger as a lose-lose scenario with little upside for Kroger if it passes, given its immense concession of selling many stores that could exercise market power. The stock is up around 5% since then, signaling continued stagnation, though it is back near its 2022 high. However, without the merger, it faces a hefty $600M breakup fee, and would be even further from gaining an edge in a grocery market increasingly dominated by Costco (COST) and Walmart (WMT).

To me, Kroger and Albertsons are in a fundamentally poor niche in the grocery market, not having the "quality" allure of Whole Foods, Sprouts (SFM), or Trader Joe's, but lacking the low-cost value of Costco and Walmart. As consumers bifurcate with the shift away from the middle class (in both directions), middle-income-focused retailers like KR and ACI are left with a declining market. Indeed, this is not an immediate trend but has existed for at least two decades. It may have initially benefited KR and ACI by pricing out smaller locally owned grocers and giving economic scale benefits to consolidators.

Although the combined company would only have ~ a 13% market share, it owns many brands and may gain a monopoly in certain local markets. The merger is further complicated by the possibility that KR is looking to sell stores to a "liquidator," not a competitor, potentially discouraging the FTC from allowing it to sell stores to offset monopoly concerns.

I see the KR-ACI situation as similar to JetBlue (JBLU) and Spirit (SAVE), as two underdogs needing to team up to survive. The problem facing KR and ACI is not as extreme; their survival is virtually guaranteed for now, but without change, I expect these long-term trends may create significant issues 5-10 years from now. However, now that this deal appears quite unlikely, I think it is best to assess KR's value, assuming it must compete independently.

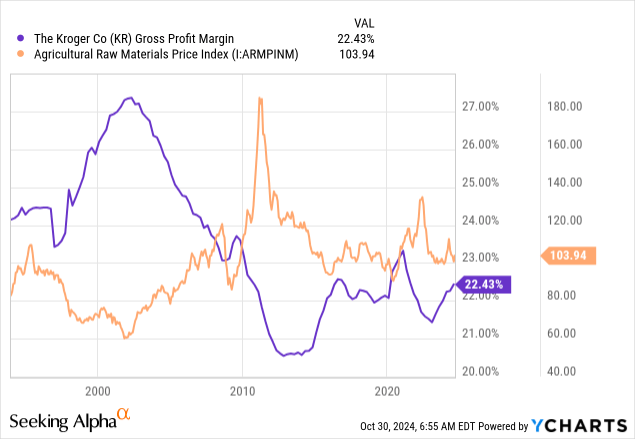

Kroger's Margins Improve On Input Costs

When I covered it last, I saw the spike in agricultural input prices as a potential negative factor for the company's profit margins. That said, a bountiful harvest season and good weather conditions. However, the decline in agricultural crop prices has hurt farms, which still face rising input costs. Over the long run, Kroger's gross margins are inversely correlated to agricultural materials prices. Low prices in 2024 have allowed KR's gross margins to recover from the cost surge in 2020 and 2021:

Data by YCharts

Data by YCharts

In my view, these conditions are unlikely to last. Although overall agricultural input costs are moderate, animal product prices have remained high this year despite a sharp decline in crop prices, led by environmental factors. Although I'd like moderate weather to continue to boost crop yields, that is essentially a random benefit that is unlikely to persist. In the long run, I expect supply side cost issues to slowly push agricultural prices higher, necessitated by falling farm income today.

That said, a slow rise in agricultural commodity prices may not directly harm Kroger's margins as it pushes costs forward, and food processing companies may absorb higher input costs. During 2021, the rise is a large short-term rise in agricultural commodities that cannot quickly be passed forward. Today, KR partially has the opposite benefit, where some input costs are falling, but it can maintain consumer prices.

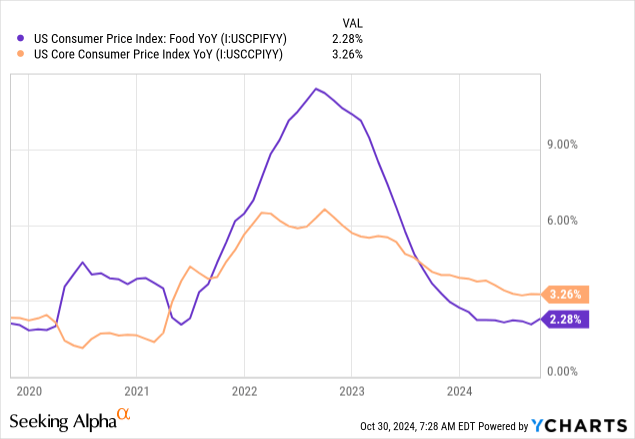

Food prices never decline for consumers, though they're more volatile than the core CPI (excluding food and energy). Today, food prices are still rising annually at ~2.3%, just below the core inflation index. See below:

Data by YCharts

Data by YCharts

Overall, I believe this supply side scenario is favorable for Kroger. Some cost factors are alleviating, while consumer prices are still increasing. I expect we may eventually see some return to 2021-2022 conditions, given that the core issues in the farming industry (as I've discussed in other articles) are not solved and likely will not be for some time.

Kroger should be able to push higher costs forward, but that should only increase the long-term trend of bifurcation toward wholesale grocers and high-end ones. It is worth pointing out that, despite having a better quality perception, Trader Joe's is generally cheaper than Kroger due to having more private-label products. To me, this signals a fundamental issue in Kroger's business model, as it focuses on horizontal integration instead of the more successful vertical integration of many of its competitors. Still, Kroger is now working hard to improve its private label brand to improve its lower-income customer base.

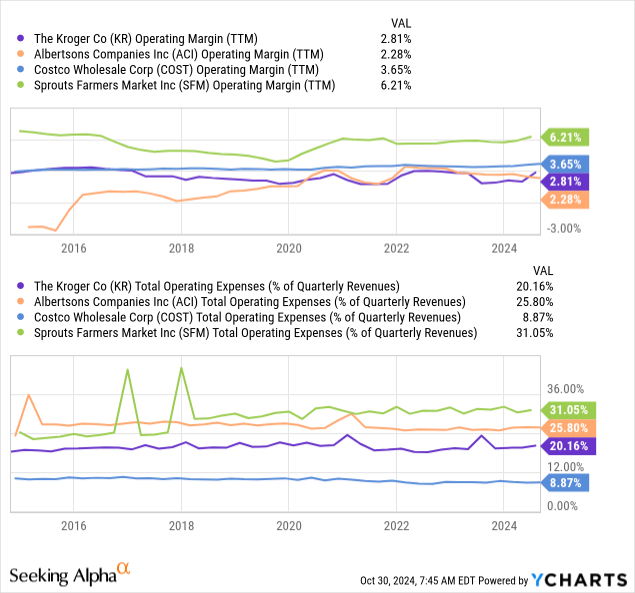

Kroger's Rising OpEx Offsets Gross Margin

Since 2022, Kroger's operating expenses have risen to just over 20% of its sales from around 18%. To be fair, this is around where it was before the cost volatility of 2020-2022. However, it largely offsets the improvement to its gross margins since 2022, keeping its overall operating margins stuck at below 3%. Its struggle is mirrored in Albertsons, but not Sprouts and Costco, which have better margins via higher gross margins (Sprouts - "quality") or lower OpEx-to-sales (Costco - bulk discount). See below:

Data by YCharts

Data by YCharts

In my view, Kroger will ultimately need to decide which market it wants to focus on or use its various brands to bifurcate its business. As with Albertsons, most of its brands are focused squarely on the middle market. However, the economic and business trends clearly show benefits from wholesale (also including Aldi's) or quality. It may be argued that Kroger is betting that the middle-class segment will eventually rebound. Although that may undoubtedly be true, retail profitability seems to always be superior in the companies I've analyzed, focusing specifically on either high-end or low-end.

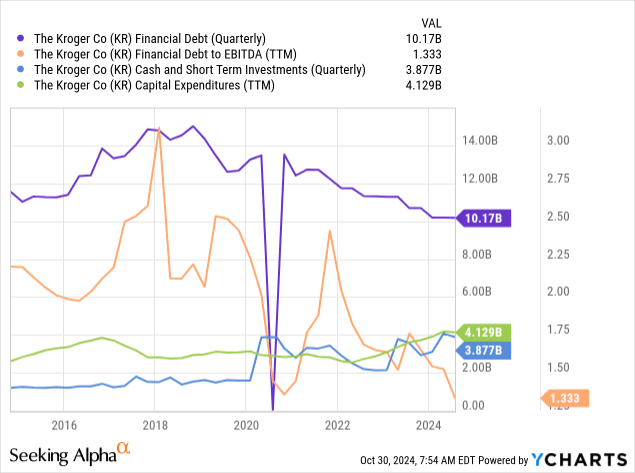

Kroger's Balance Sheet Is Improving

On the positive side, Kroger is more financially sound than it has been over the past decade. The company has dramatically reduced its financial debt while improving its EBITDA. As a result, it now sees a buildup in cash liquidity, allowing it to raise its CapEx spending to strengthen its long-term position. See below:

Data by YCharts

Data by YCharts

In my opinion, Kroger must invest a decent amount of capital to secure a future without Albertsons. Although I am not convinced it has fortified a competitive moat, it is clear that the company is working toward that goal. Slowly, it is working away from the immense debt it had after its acquisition binge in the 2010s. Although it could benefit from ACI, I think Alberstons' debt and the need to sell stores with potential market power make it a net loss for KR, though the deal is a gain for ACI. Still, at this point, I lean toward the view that KR's best path forward is without ACI. The $600M breakup fee is unfortunate, but not so large as to seriously harm the firm.

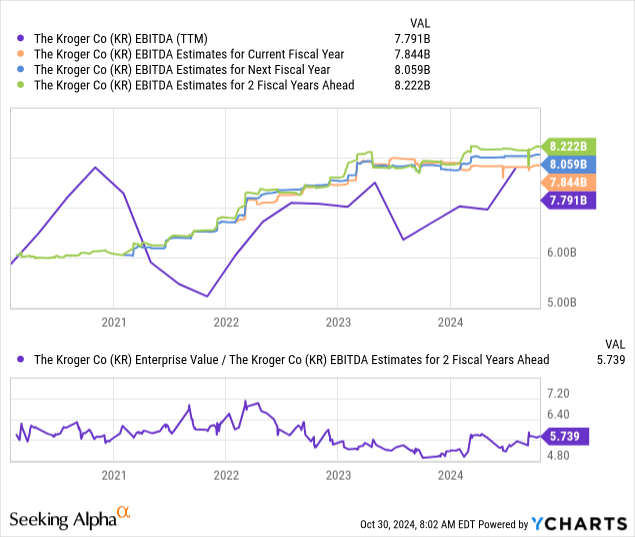

Kroger's sales are also expected to rise at a CAGR of about 2% over the next two years, marking a slight recovery from expected declines this year. See below:

Data by YCharts

Data by YCharts

I think Kroger may manage higher-than-expected sales growth over the next two years. One key factor may be a rebound in food inflation and food input costs, which would improve sales but not necessarily its profits. Still, its EBITDA is expected to increase to $8.22B by the end of 2026. As such, its forward "EV/EBITDA" valuation is below levels seen two years ago. See below:

Data by YCharts

Data by YCharts

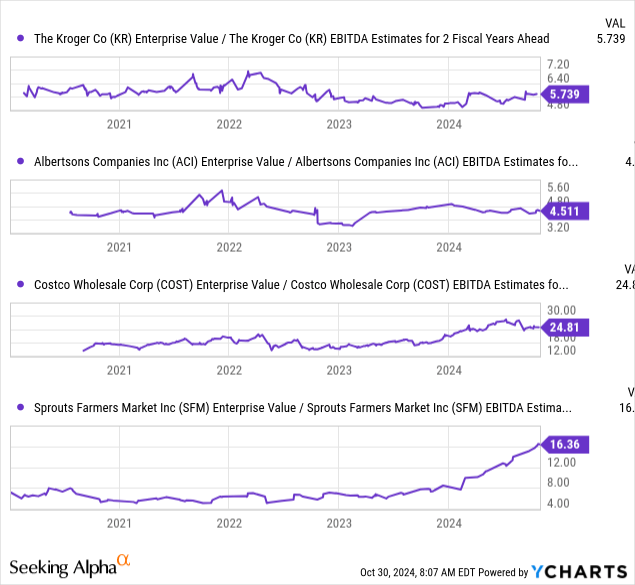

Overall, I think this situation is moderately bullish for KR. Its forward "EV/EBITDA" is only slightly below its 2022 level and is just above ACI's. However, it is far below Costco's and Sprout's at about 24.8X and 16.4X, respectively.

Data by YCharts

Data by YCharts

Costco and Sprouts may have superior market positions and growth, but I believe that still leaves KR at a significant valuation discount. The critical assumption is that Kroger will manage to build a moat. Kroger may also benefit if Albertsons, which is in a worse financial and operational position, loses market share by closing stores in competitive markets.

The Bottom Line

Overall, given Kroger's stability over the past year, its improvement in gross margins and valuation discount, and the likelihood of avoiding a bad merger deal (given the FTC's requirements for the merger), I am no longer bearish on KR.

My outlook on KR is relatively neutral, given its prospects are not secured. That said, I believe it is undervalued compared to other public grocers. Although ACI is cheaper, I have less hope for its recovery than I do Kroger and expect Kroger will gain market share if ACI closes stores if the merger fails, as it has warned. Thus, I may become bullish on KR once we know the deal is off the table.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.