US Stock Valuation & Estimates in 2025

Against the backdrop of the current record highs in the market, investors are increasingly concerned about the valuation situation of U.S. stocks.

Multi-dimensional comparative analysis of U.S. stock valuations

Dynamic Valuation

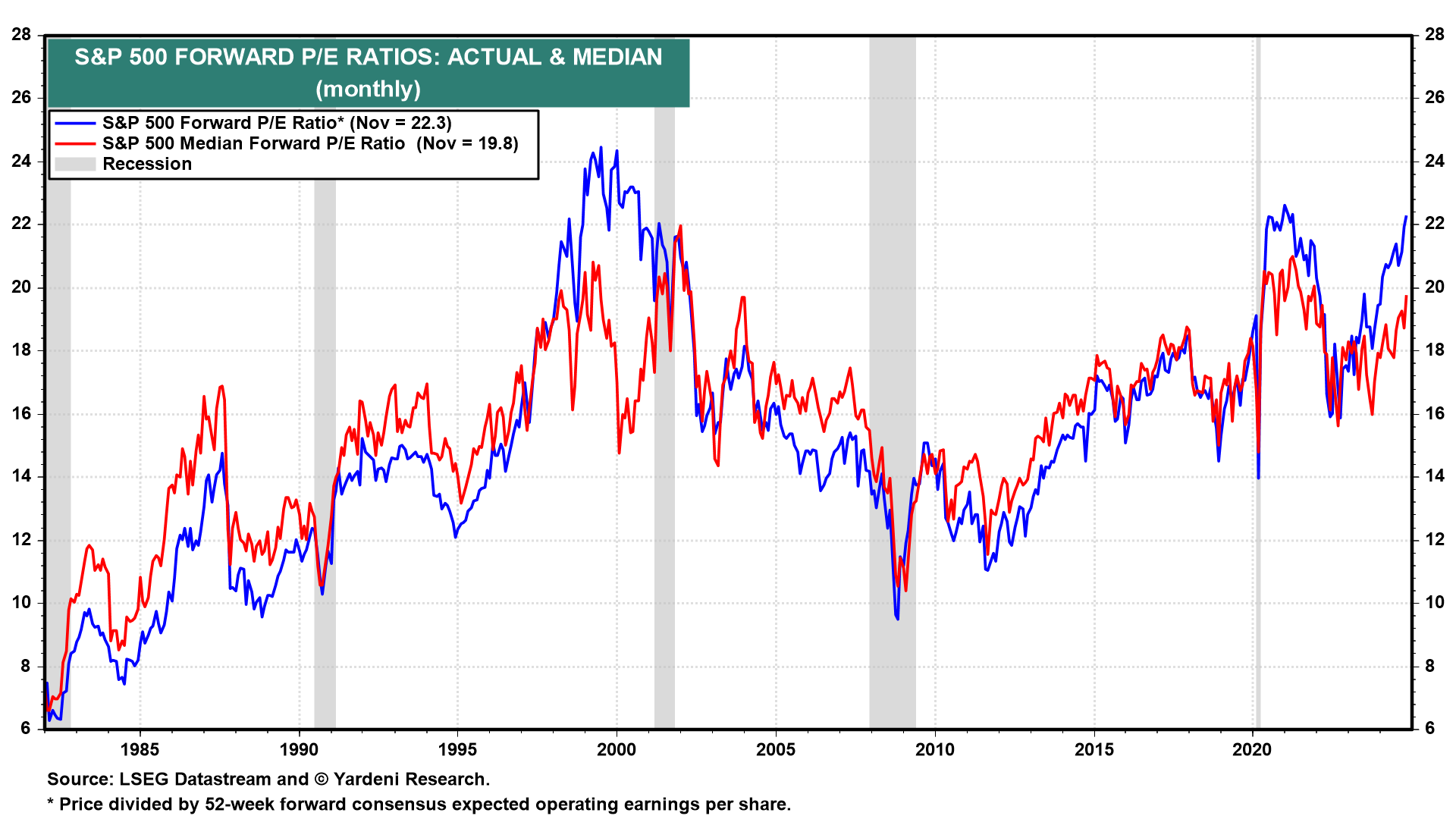

$.SPX(.SPX)$ The current dynamic P/E ratio of 22.7x is not far from the previous high of 23.4x (2020/9/2), is 1.8x standard deviation above the average of 16.6x since 1990, and is in the 94th percentile of its historical score.The static P/E ratio is even at 27.3x.

This suggests that U.S. stock valuations are not cheap from a dynamic perspective, even taking into account future earnings expectations.

Side-by-Side Comparisons

Global Market Valuation Deviation: The MSCI U.S. Index's current valuation has a high degree of deviation from its own historical average, at 1x standard deviation above the mean, while European, Hong Kong and other markets are valued below their historical averages.

Versus other markets: The S&P 500 vs. Nikkei 225, European Stoxx 600 and MSCI Emerging Markets are all currently at a premium to their average premiums since 2000;

vs. bonds $US10Y(US10Y.BOND)$ $US30Y(US30Y.BOND)$ : comparing dividend yields to bond yields, the 12-month dynamic dividend yield on the S&P 500 is less than one-third of the yield on the 10-year U.S. Treasury note, a historic low, suggesting that U.S. equities are overvalued relative to bonds

Versus Gold $SPDR Gold Shares(GLD)$ : While gold is also at new highs and in a historically high quartile, the S&P 500/Gold ratio is also above average;

Comparison to Oil Prices $United States Oil Fund LP(USO)$ The S&P 500/crude oil price is at an above-average point, but the oil price relationship is relatively dynamic.

Sector Differences

The dynamic valuations of growth and value styles show significant differences.

Dynamic valuations of the Nasdaq and the Mag7 index of big tech have reached 29.5x and 31.4x, respectively, higher than the Dow Jones and S&P 500, at 21.2x and 22.6x.

Within each sector, with the exception of energy, all other sectors' current 12-month dynamic valuations have exceeded their averages since 2001.The consumer discretionary, financials and IT sectors are in the 95%+ bracket, while the energy and real estate sectors are in the 60%+ bracket, which is relatively low in the historical dimension.

In addition, the headline concentration of large-cap companies is obvious.Of course there is a certain amount of revenue and profitability behind the concentration of market capitalization.

U.S. Stocks 2025 Expected Outlook

(i) Policy implications

Policy adjustments related to the new U.S. administration in 2025 are expected to impact the U.S. stock market in a number of ways.

First, if foreign tariffs are increased, this will raise the price of imported goods, which in turn will push up the level of inflation.Changes in inflation will affect the cost of business and consumer purchasing power, for those who rely on imports of raw materials or for the domestic consumer market, profitability may be compressed, but also may prompt the Federal Reserve to make corresponding adjustments in monetary policy to cope with inflation, which indirectly affects the U.S. stock market capital surface and the overall valuation of the situation.

Secondly, the tightening of immigration policy will make the labor supply shortage, on the one hand, increase the enterprise labor costs, affecting corporate profits; on the other hand, part of the industry may be due to the lack of labor to face a bottleneck in the development of labor-intensive industries, such as construction, catering and other labor-intensive industries.

In addition, the increase in domestic tax cuts is expected to enhance the level of domestic corporate profitability, is expected to affect the profitability of the S&P 500 companies by 2-3%, especially for those industries whose earnings are more sensitive to tax policy, such as the manufacturing industry, is expected to usher in the valuation of the restoration and stock price enhancement.The increase in corporate disposable capital will help to enhance the intrinsic value of the stock and strengthen its attractiveness to investors.

(ii) Fundamental Factors

Different organizations have their own expectations for the performance of the U.S. stock market in 2025.

According to the Bloomberg Consensus Estimate, the Nasdaq Index, which has strong technology growth attributes, is expected to grow at a rate of 25.8% in 2025, which is the leading rate among the major markets in the world, indicating that the technology sector in the U.S. stock market still has strong growth potential.

Although the market for the fourth quarter of 2024 earnings growth is expected to be adjusted downward, reflecting the short-term growth in U.S. stock performance confidence is slightly less, but only a slight change in earnings expectations for the full year of 2025, which means that the overall U.S. stocks next year is not pessimistic, the U.S. stock earnings are still resilient.

Structurally, the technology sector is worth focusing on.

Q3 earnings show that the performance of the TMT sector as a whole is resilient, the cloud business is strong, and advertising, e-commerce, subscription and other businesses are also in a solid growth state;

Cryptocurrency, AI and other sectors belong to the Trump industrial policy favor plate, is expected to continue to provide support for the earnings growth of technology stocks.For example, Google, Microsoft, Amazon and other technology giants in the AI drive, cloud computing revenue and earnings growth have increased;

At the same time, pro-cyclical sectors should not be ignored.As the Fed's interest rate cut process continues, the market will gradually benefit from only the denominator end (valuation improvement) of the asset to the molecular end (earnings repair) will usher in the improvement of the asset, Trump's policy is more inclined to support the traditional industries, with the relevant policies in 2025 to gradually promote the implementation of the medium-term pro-cyclical plate earnings or will improve, like industrial, energy and other pro-cyclical plate is expected to usher in the valuation and earnings of the dualThe pro-cyclical sectors such as industrials and energy are expected to see both valuation and earnings restoration and play a more important role in the U.S. stock market.

Goldman Sachs, which expects the S&P 500 to rise to 6,500 by the end of 2025, with a total return of up to 10% including dividends, believes that while U.S. stock valuations are at a high level, they are likely to remain high as long as macro conditions are supportive, and that factors such as strong GDP growth, the continued strength of large tech stocks, and the lower corporate tax rate are expected to propel U.S. stocks to a better performance in 2025.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

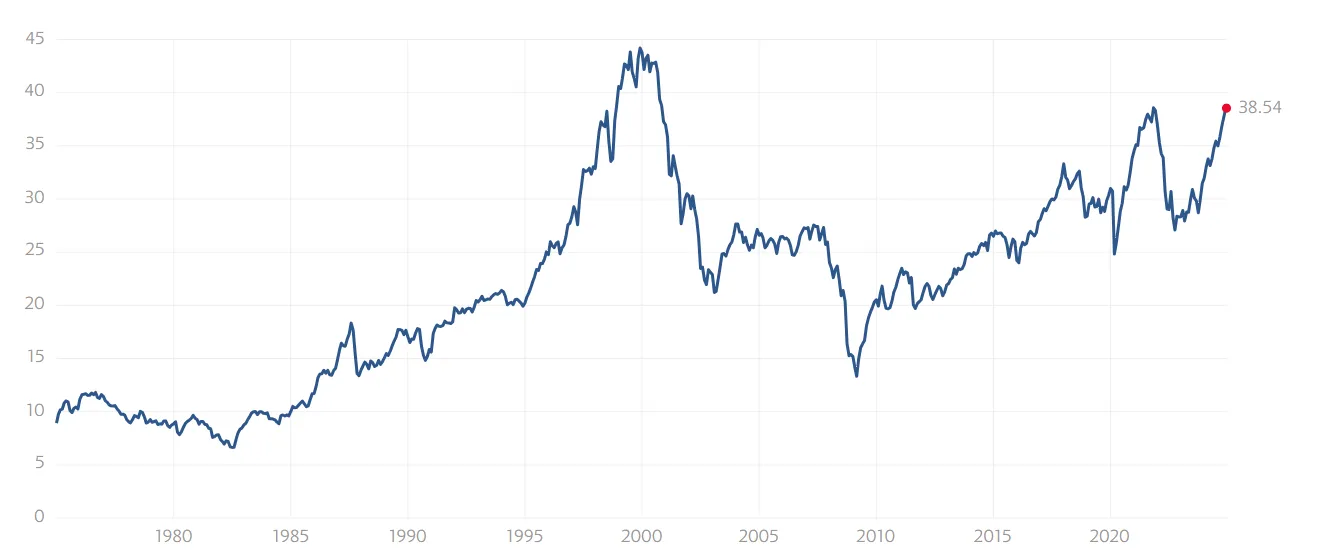

According to the factset: The trailing 12-month P/E ratio for $SPX of 28.7 is above the 5-year average (24.1) and above the 10-year average (21.9).

With tech stocks projected to grow, it seems like a good time to focus on the Nasdaq. Any recommendations on specific stocks?

Does anyone else find the comparison to bond yields alarming? U.S. equities seem overpriced in relation to bonds