ORCL Q3: AI-driven RPOs hit record highs, market divided on guidance

$Oracle(ORCL)$ Q3 FY2025C results highlight a strong demand environment, particularly in its cloud and AI segments.

The company achieved record order intake and demonstrated strong financial discipline while improving shareholder returns, but current period results were somewhat short of expectations;

Looking ahead, Oracle's strategic focus on artificial intelligence and multi-cloud partnerships puts it in a position to accelerate growth, with revenues expected to grow by approximately 20% in fiscal 2027.

Performance and Market Feedback

Core Financial Indicators

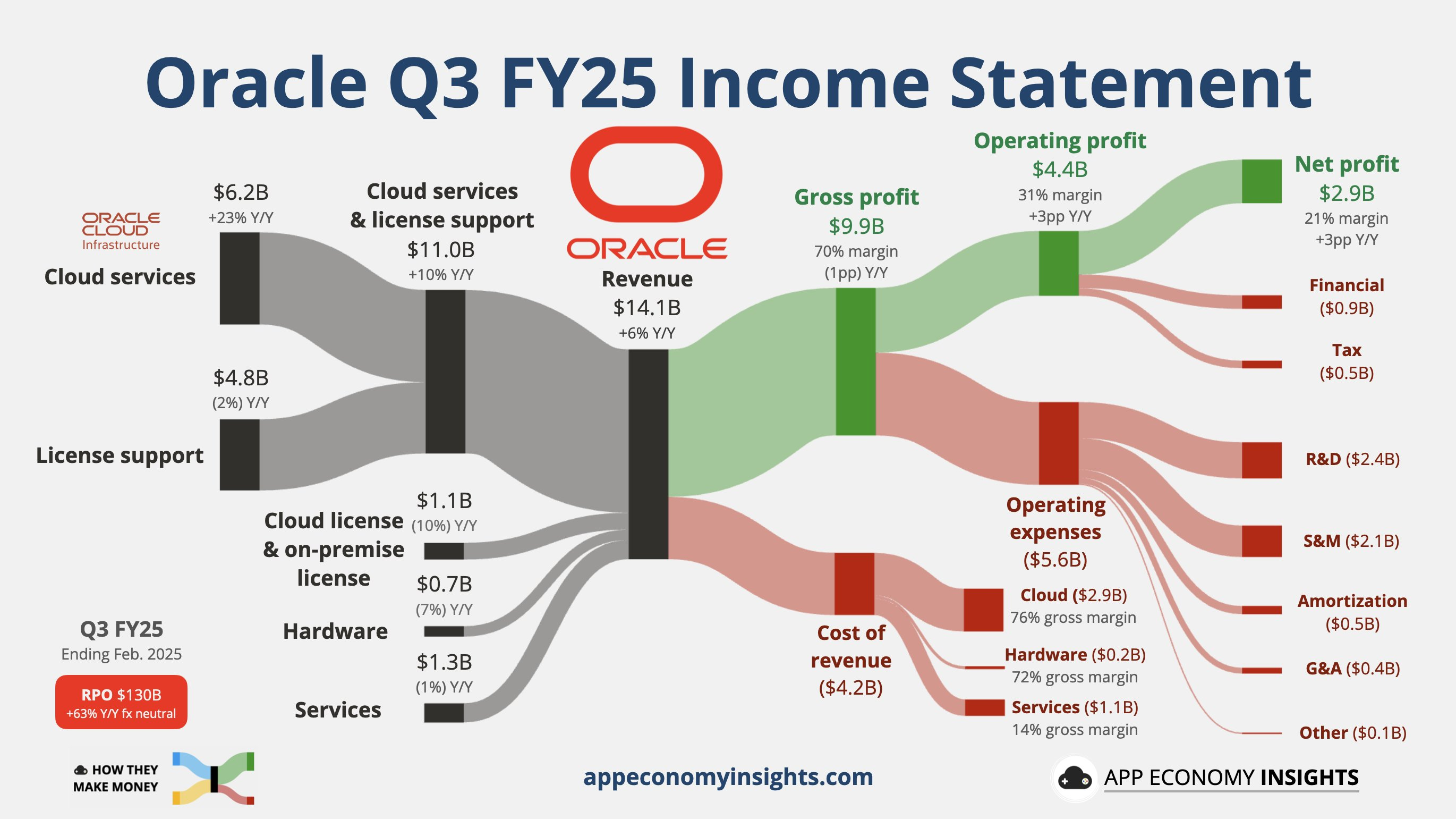

Total Revenue: $14.1B (+6% yoy, +8% FX), below market expectation of $14.39B

Cloud Services & License Support Revenue: $11.0B (+10% yoy, FX +12%), 78% of revenue, but below estimates of $11.21B

Cloud Infrastructure (IaaS) revenue: $2.7B (+49% yoy), a growth highlight

Cloud licensing and local licensing revenue: $1.1B (-10% yoy), hardware revenue $0.7B (-7% yoy)

GAAP EPS: $1.02 (+20% yoy), Non-GAAP EPS $1.47 (+4% yoy), below expectations of $1.49

Remaining Performance Obligation (RPO): $130B (+63% yoy), a record high

Market Reaction

Shares fell 6.9% after hours following the earnings release, mainly due to revenue and earnings misses and market divergence on the 15% revenue growth guidance for the next fiscal year

Investors are concerned about slowing growth in cloud services (especially core SaaS business only +10%) and continued decline in hardware business, but are gaming the explosive growth in AI-related businesses (e.g., IaaS +49%) and the long-term potential of RPO reserves

Investment highlights

Cloud infrastructure becomes a growth engine, but competitive pressures emerge

IaaS revenue +49% yoy to $2.7B, driven by AI training (GPU consumption +244% yoy) and multi-cloud databases (revenue from AWS/Azure/GCP +92%)

However, overall cloud service revenue (including SaaS) growth slowed to 23% from 25% in Q2, reflecting intensified competition in the public cloud market

AI strategy entered the period of realization

Has signed cloud agreements with OpenAI, xAI, Meta, etc., with plans to double data center capacity within the year

Launched Oracle AI Data Platform to directly connect big models with databases to drive commercialization of AI inference, with current annualized revenues from related databases reaching $2.3B (+28% yoy)

Financial Structure Optimization and Risk

Operating cash flow TTM is $20.7B, but free cash flow TTM is only $5.8B, indicating capex pressure (mainly for AI data center construction).

RPO of $130B, with annualized revenue guarantee of over $26B (~50% of current annual revenue) based on a 5-year performance period, but need to pay attention to performance progress.

Analyst Focus (Earnings Call Highlights)

Growth sustainability: management expects FY2026 revenue to be +15%, but current RPO growth (+63%) is well above that guidance, with the potential for conservatism

Margin paradox: Non-GAAP operating margins are stable at 44%, but IaaS expansion may depress medium-term margins

Stargate project: first AI supercomputer contract to be signed soon, may be a valuation catalyst

Remaining competitive in the cloud services market, Oracle emphasized its strength in the multi-cloud database space, with Database MultiCloud revenues up 92% year-over-year, citing partnerships with $Microsoft(MSFT)$ $Alphabet(GOOG)$ and $Amazon.com(AMZN)$ as helping to drive this growth.Oracle also highlighted its investments in AI infrastructure, including its NVIDIA and AMDpartnerships to enhance its cloud services capabilities

How Oracle's Multi-Cloud Strategy Meets Customer Needs Oracle emphasized the benefits of its multi-cloud database, which enables it to support customers in deploying and managing their databases on multiple cloud platforms, which helps improve customer satisfaction and retention.At the same time, Oracle's multi-cloud capabilities enable it to partner with other cloud service providers to expand its market share

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Twelve_E·03-11$Oracle(ORCL)$ is promising!LikeReport