Weak growth, low confidence, KSS still plunged on beat earnings,

Kohl's (KSS) Q4 2024 (ending February 1, 2025) earnings report presents a two-sided picture of earnings beat but weak growth momentum and dampened market confidence. $Kohl's(KSS)$

Performance and market feedback

Core Financial Performance

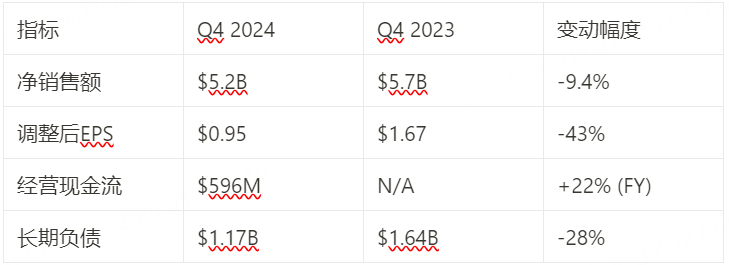

Revenue: Q4 net sales of $5.2B (-9.4% YoY), comparable sales of -6.7%, slightly ahead of market expectations of $5.19B but down significantly YoY

Margin: Gross margin 32.9% (+49bps YoY) thanks to promotion optimization and lower digital penetration; however, SG&A expense ratio rose to 28.5% (+148bps YoY), reflecting faster revenue declines than cost controls

Earnings: Adjusted EPS of $0.95 (-43% YoY) beat estimate of $0.72; however, GAAP net profit of $48M (-74% YoY) showed drag from one-off expenses.

Market reaction and share price volatility

After-hours plunge: Shares fell more than 15% in a single day after the earnings release, with a cumulative decline of 47% for the year, mainly due to sharply weaker-than-expected 2025 earnings guidance:

2025 revenue expectation -5%~-7% (vs market expectation -1.6%);

Comparable sales expected -4%~-6% (vs market expectation -0.9%);

EPS guidance of $0.10~$0.60 (vs $0.23 expected).

Investor sentiment: Concerns about the effectiveness of strategic adjustments, dividend cut (from $0.25/qtr to $0.125) further undermined confidence.

Investment Highlights

Operational Dilemma and Strategic Rethinking

1. Loss of core categories and strategic miscalculation

The CEO admitted that over-expansion of new categories has led to a lack of resources for core businesses such as jewelry and private labels5, and that it is necessary to rebuild competitiveness by upgrading the store experience (e.g., expanding Sephora counters) and optimizing the supply chain.

2. Cost and Cash Flow Leveling

Capital allocation: $400M~425M capex planned for 2025, focusing on omni-channel and inventory turnover optimization.

Debt management: prioritize debt repayment due in July 2025, long-term goal to resume share buybacks

3. Analyst Focus

Comparable sales rebound path: management proposes to optimize promotional strategy, but no clear timeline given

Inventory pressure: Inventory +2% YoY to $2.9B, need to observe spring merchandise turnover efficiency;

Margin defense: full year gross margin target of 37.2% (flat y/y), but SG&A charge control becomes more difficult

Key data comparison (Q4 2024 vs Q4 2023)

Short-term risks

Comparable sales may remain under pressure in a weak consumer demand environment;

Dividend cuts may trigger withdrawal of long-term investors;

Interest expense pressure in 2025 (Q4 interest $74M ) limits earnings resilience.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.