Only 8.5x PE, Is Brazilian Fintech STNE on a buying dip?

$StoneCo (STNE)$ Demonstrated strong execution and business model resilience in a complex macro environment, but need to validate growth sustainability in the 2025 interest rate cycle.

Short term focus on software asset disposal progress and Q1 credit asset quality data, long term more on MSME customer growth, and international market expansion.

Performance and market feedback

A quick look at core data

Financial Indicators

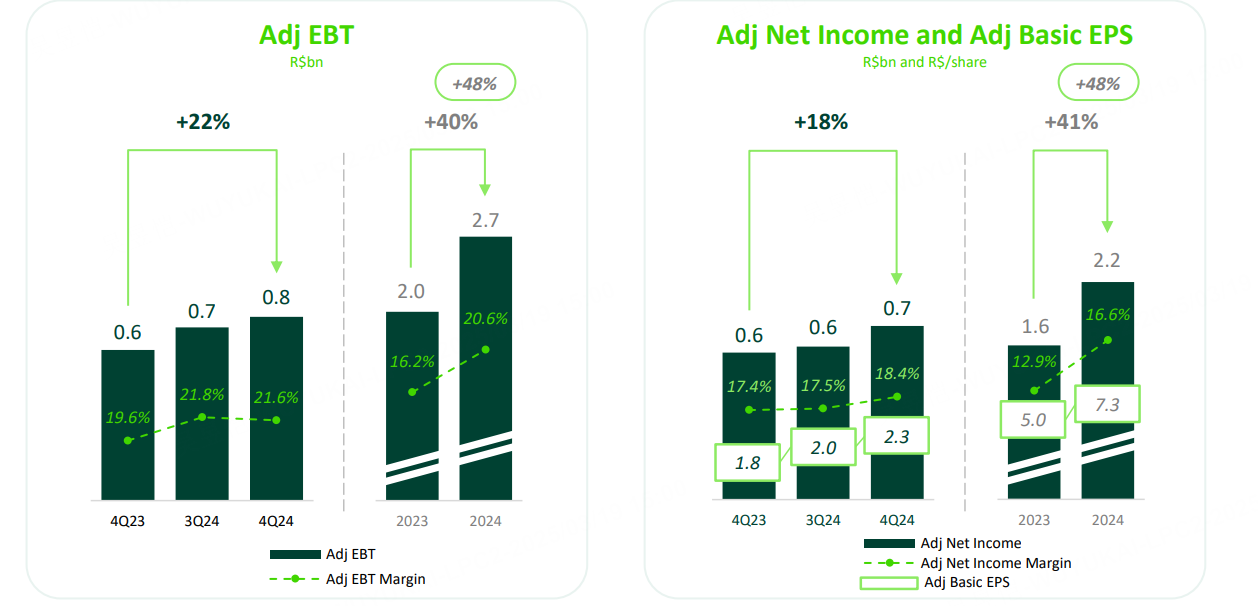

Adjusted Net Profit: R$2.2B (+41.3% yoy, ahead of guidance of R$1.9B)

Adjusted Earnings Per Share (EPS): R$7.27/share (+46.6% yoy)

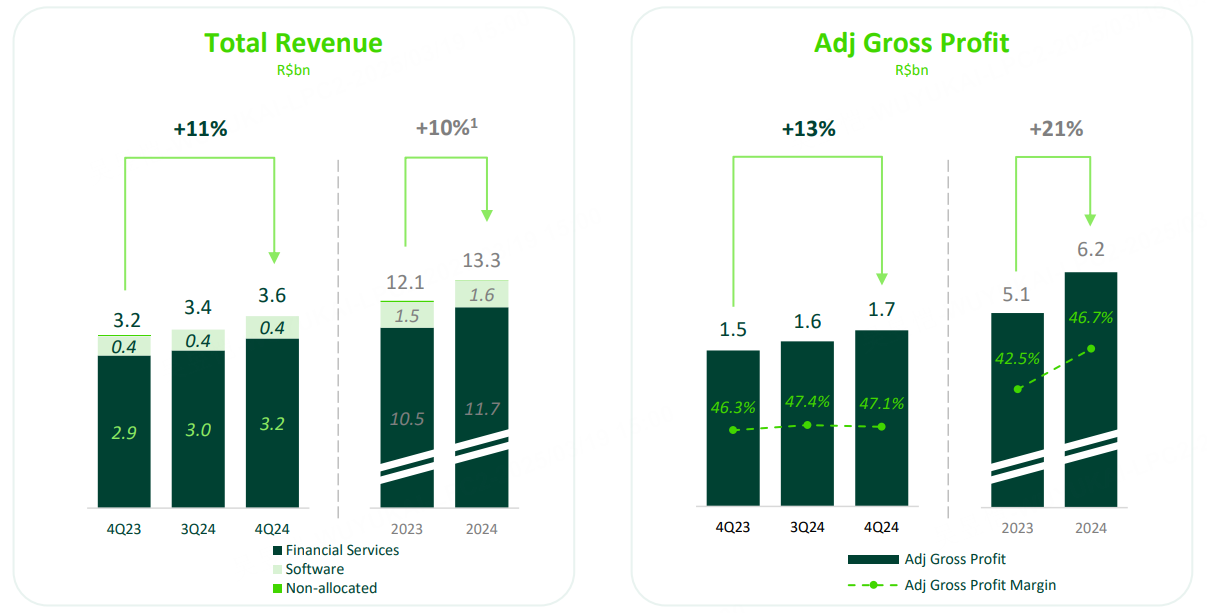

Total revenue: 14% yoy CAGR (2022-2024 CAGR)

Operational Indicators

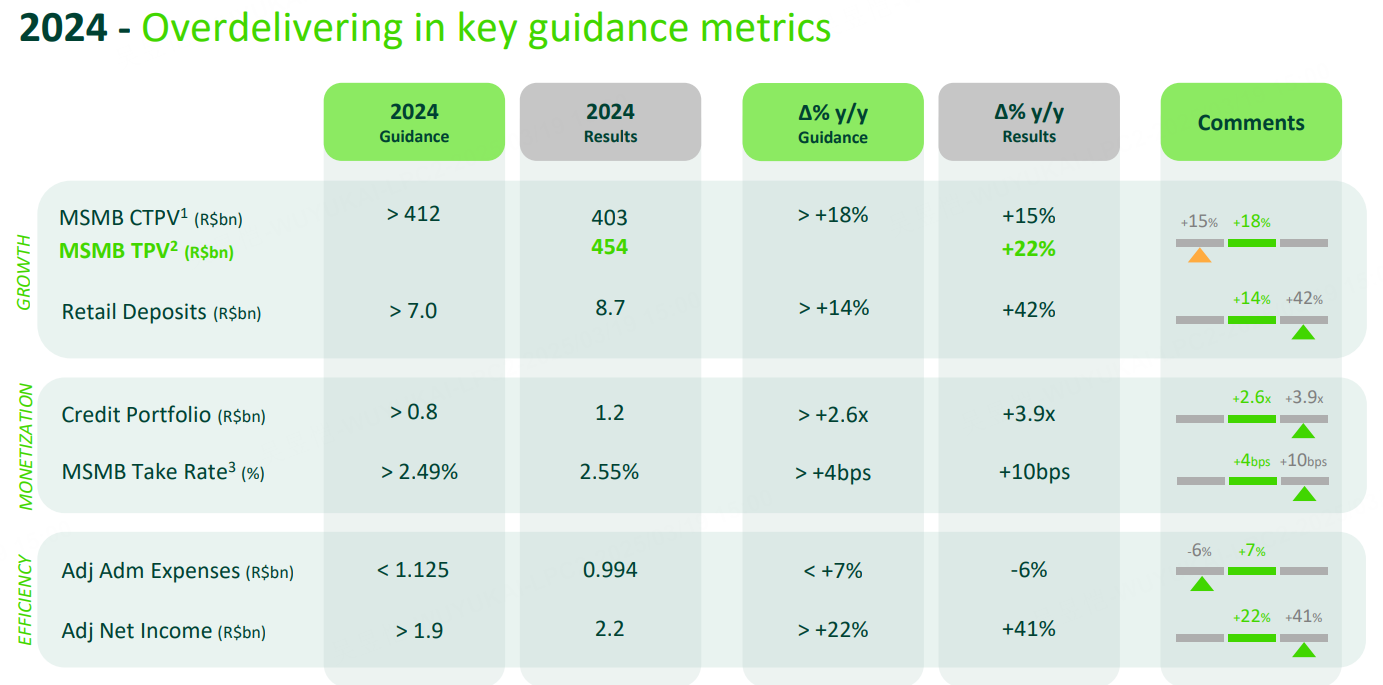

MSMB Payments: TPV of R$454B (+22% yoy), of which R$403B (+15% yoy, 2% below guidance) for card payments

Retail deposits: R$8.7B (+42% yoy, 24% above guidance)

Credit portfolio: R$1.2B (nearly 4x growth, well ahead of R$0.8B target)

Risk Control: 90+ day NPL ratio of 3.6% (manageable level)

MARKET REACTION: Shares are down 55% in 2024, significantly underperforming the Nasdaq (+28%), with a widely divergent market view and price targets spanning $7-$25.Shares are +10%+ after the after-hours earnings release, with greater optimism overall, but there will still be ongoing concerns about Brazilian macroeconomics (high interest rates, inflation).

On the optimistic side, net profit, deposits, credit exceeded guidance, AI application to reduce costs and increase efficiency (customer service efficiency improved by 45%), capital return program (exceeded R$3B excess capital)

Risks, slower growth in payments business (PIX hitting card transactions), pressure on interest rate environment in 2025, uncertainty on strategic realignment in software business

Investment highlights

Strategy execution efficiency exceeded expectations

Payment+Banking+Credit Triple Engine: Credit portfolio R$1.2B (150% of guidance), retail deposits R$8.7B (24% of guidance), validating the closed loop of "Payment channeling→Sedimentary funds→Credit realization".

Rate resilience: MSMB composite rate of 2.55% (6bps above guidance), reflecting optimization of revenue structure by value-added services (e.g. PIX QR code payment).

Moat validation

PIX shock manageable: QR Code payments were successfully monetized, credit card transaction volume remains +15% yoy (management says PIX mainly replaces debit scenarios, not credit)

Cost control: administrative expenses of R$994M (below guidance of R$1.125B), AI applications have automated 100% of customer service (CSAT is higher than manual)

2025 Core Concerns

Interest rate sensitivity: long-term interest rates in Brazil, if they remain high, could suppress demand for credit from small and medium-sized merchants (current credit portfolio is only 0.26% of TPV, room for penetration and risk)

Capital allocation priorities: software divestiture progress (releasing capital for main financial business) vs. shareholder return pace (current dividend yield 0%, buyback plan to be clarified)

Market Focus Recap.

Is PIX disrupting the credit card business model?

PIX mainly replaces cash/debit scenarios, credit card installment payment advantages remain, and PIX NFC will drive innovation in offline scenarios (example: 35% of PIX transactions in 2024 will be B2B scenarios, with higher gross margins than card payments)

How to balance credit expansion and asset quality?

Current R$1.2B credit portfolio is 70% short-term working capital loans (<12 months) with manageable delinquency rate using dual screening model of "customer payment data + AI risk control".

Drivers of slower Total Payment Volume (TPV) growth (Q4 TPV +25% yoy vs Q3 +28%) and lower Take Rate (2.09% vs 2.15% Q3)?

TPV growth slowed due to seasonality (holiday season base effect), but SMB customer contribution continued to grow (75% share); Take Rate declined due to higher share of low-fee solutions (e.g., PIX Instant Payments), but customer stickiness increased (churn declined to an all-time low of 5.2%)

Is SMB customer growth facing a ceiling (Q4 additions +18% yoy vs Q3 +22%)?

Brazilian SMB digital penetration is only 45%, still room to double, with plans to reduce customer acquisition costs through AI customer service tools in 2025 (target CAC reduction of 10%).High-value customers (monthly transactions >R$50k) share increased to 32% (+7pp yoy).

Capex plans for international expansion (Mexico market) vs. competitive risks?

Mexico Q4 TPV +40% YoY, Take Rate stabilized at 2.3% (higher than Brazil), plans to invest $150M in 2025 (25% of full year capex).Competition focused on differentiated services (e.g., cross-border payment solutions), not price wars

Valuation Discussion

Current P/E is only 8.5x (based on 2024 adjusted EPS), significantly lower than Latin American FinTech peers (PagBank 15x, NuBank 22x) Discount reflects: (1) Brazilian sovereign risk premium (2) Concerns about slowing payment growth (3) Uncertainty about software business restructuring.

If R$3B capital return is realized in 2025 (corresponding to 10% market cap), it may constitute a catalyst.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.