Tencent Q4 Earning Boosts, Still Cheaper Than AAPL?

After the Hong Kong stock market closed on March 19th, $TENCENT(00700)$ announced its Q4 '24 and full-year financial results. $Tencent Holding Ltd.(TCEHY)$

Looking over the first three quarters of 24 earnings, Tencent complete show the recovery rebound cycle in the new atmosphere of the big technology companies, on the one hand, the revenue side of the open source to further accelerate, at the same time the cost side of the cost side is not restrained, restarted to invest in the cycle, in particular, Q3 mentioned to increase the investment in capital expenditures (AI direction), and on the other hand, the profit side of the run, not only after the first few years of cost-cutting and efficiency gainsrate reductions, profits from associates as well as investment income have also led to accelerated growth in the denominator.

Overlaying the current big rally in Chinese assets led by the tech sector, the market is revaluing and repricing. The short term will require a succession of funds from different types of investors (from HF to LO), and the long term will still depend on the sustainability of the earnings growth and the new incremental growth that can be generated in the age of AI.

Tencent has always been generous in its returns to shareholders, with over $100bn of buybacks in FY24, as well as plans to continue buybacks of $80bn in 2025 (i.e., at the level of $300-400m in a single day), which would not only further strengthen shareholder confidence, but also potentially usher in a long bull run like $Apple(AAPL)$

The key performance of Q4 results are as follows

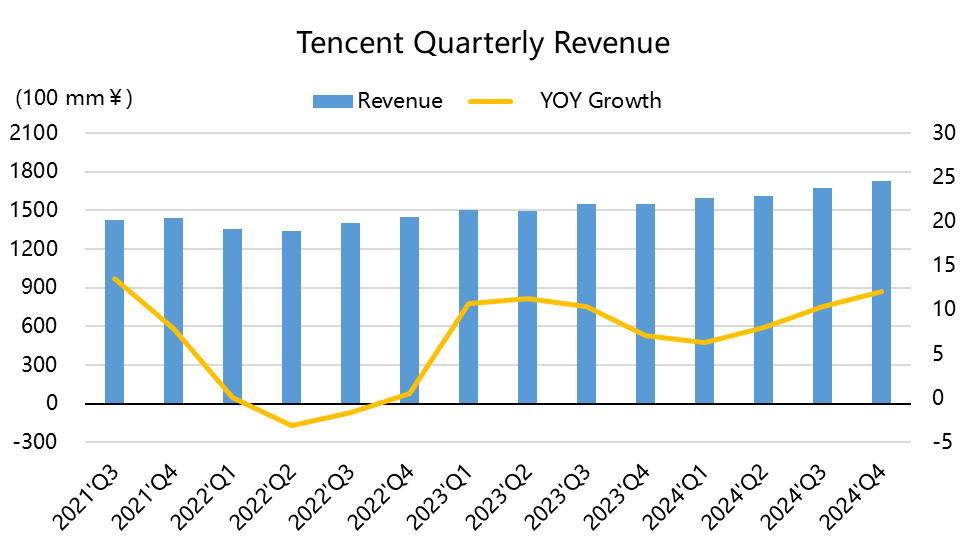

Revenue growth returned to double-digit (+11%), solidly exceeding expectations, and the degree of exceeding expectations (Surprise) was the best in the past two years;

Gaming and advertising were the two main sectors that exceeded expectations, with domestic gaming benefiting from a low base and the release of the gaming up-cycle, and the advertising business from the improved efficiency of WeChat affiliate ads (which caused almost industry-wide growth); while FinTech and social networking were largely flat with market expectations, and better yet, both wealth management and business support saw sales volume rise in Q4.

Cost of revenue growth was mainly in game content as well as server bandwidth, and while overall gross margin growth was as high as 17%, market expectations were not originally low, and actual gross margin was slightly lower than expected (52.6% vs. 53.3%).However, because the three major expense ratios remained at a solid level, marketing expenses stabilized at 6%yoy, and manpower expenses accounted for 17% (with an increase in investment in AI), overall operating profit (EBIT), although growing at a higher rate (+24%yoy), was actually still slightly weaker than expected ($51.48bn vs $52.06bn) but investors shouldn't be overly concerned about that!The real thing that made net profit explode was the investment in the company.

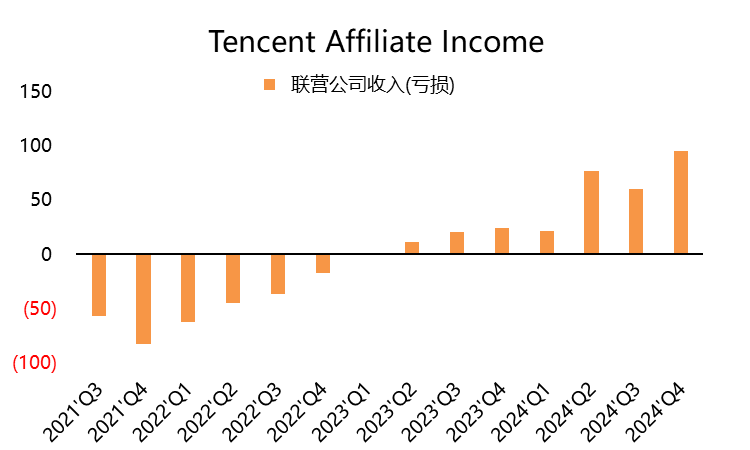

What really makes net profit explode is investment income, earnings from associates (Q4 reached 9.25bn vs Q3's 6.01bn vs Q23Q4's 2.46bn), making the overall net profit margin 29.8% (vs 26.2% expected), and of course, higher profit margins can further support the valuation.

Based on the closing price of HK$540, the current TTM PE (counting Q4) is down to 25.9x, and the Forward PE of 2025 is 23.4x, which is still not too high compared to Mag7 of US stocks.

Investment Highlights

Game business entered the release period, both domestic and overseas game growth rate returned.Q4's VAS overall growth rate of 14% (11% over the overall growth rate), the main contribution is still the game, of which domestic +23%, overseas +15% (climbed up from 9% in the last quarter), Q3 deferred trend has also long illustrated that the Q4 rebound will not be bad, just release how much of the problem;

Domestic games have the advantage of a lower base in 23Q4, so the growth rate jumped up is also relatively well understood, the old game "King's glory" "peace elite" are relatively stable performance, "DNF" hand tour, "Delta action" has also passed the peak of the flow of water, the future probability of conforming to the life cycle of the normal mainstream game; the future focus will remain on the excellent means of operation to continue to promote the living of the old game, for example, the "Golden Shovel Shovel".

Overseas due to last quarter's adjustment of the deferral cycle led to slightly less than expected, this quarter resumed double-digit growth rate (+15%), the key is to look at the level of the future retention rate to mention.

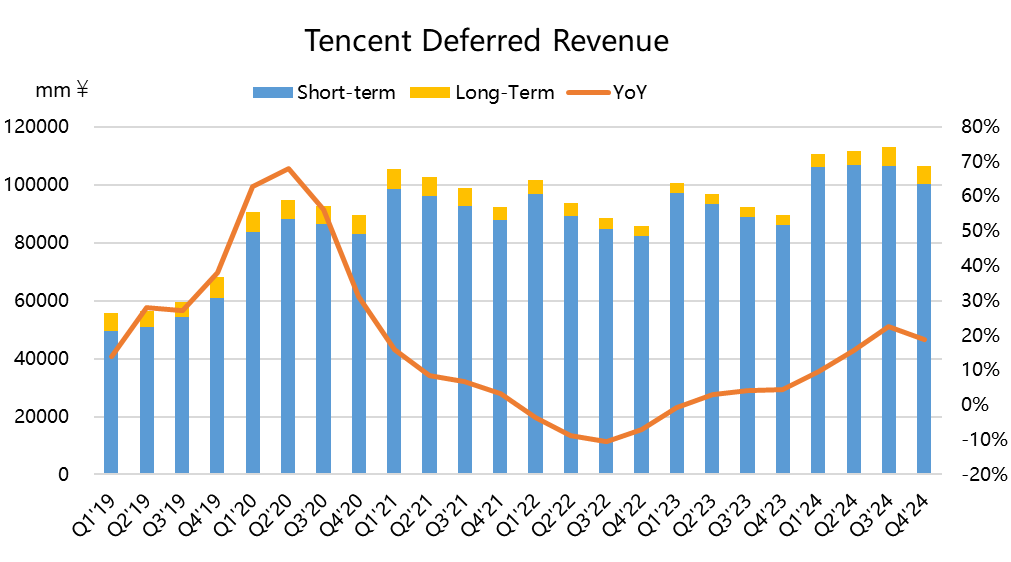

Deferred revenue of 100.1 billion yuan, a year-on-year growth rate of 18%, but the ring showed the first decline in four quarters (-6%), the next 1-2 quarters of game revenue is still guaranteed for now.

The importance of the advertising WeChat ecosystem continues to grow.Advertising revenue of 35 billion yuan, up 17.5% year-on-year, even higher than Q3 0.5 pct, exceeding the expected level of more than 1 billion.

This part of the market is actually relatively insufficient expectations, because they are observing the incremental ceiling of WeChat social advertising. q3 new on WeChat small store, SoYiSuo has become the source of Q4 incremental, WeChat ecosystem of commercialization of the ability to realize has been further proved, the WeChat ecosystem.

Due to the access to DeepSeek in Q1, the activity of WeChat SoYiSuo has also been further improved, and now all of them (Jittery, Quick, Little Red Book, etc.) are strengthening the search function of their internal systems, and will also push the results more in line with the user's habits through algorithms, so

In addition, media advertising may also stop falling and rise in Q4, especially during the shopping season, when competition among merchants and brands will be more prominent, also bringing seasonal increment.

Overall marketing services gross margin rose to 53% from 52% last year.

The FinTech business grew at +4% year-on-year, better than last quarter's 2%, and market expectations for this part of the business have not been put very high. remained stable, but the financial business is still facing a big environment.

The payment business, which accounts for the highest percentage of the total, also stabilized with the performance of offline payment activities, but the overall still does not become a rebound.It is worth mentioning that WeChat Pay did not see significant growth after the announcement of its inclusion in Taobao, and user behavioral habits are a very important moat (the same goes for WeChat).

Pulling growth is already still financial income, which rather suggests that the current environment is already cautious and tends to favor conservative investments.We may need to see further growth once China's assets rebound and consumption starts to be stimulated.

Gross margins remained at new highs, but market expectations were also high and therefore slightly weaker than expected (52.6% vs 53.3%), marketing and administrative expenses remained stable, but the pace of expansion in terms of investment investors were happy to meet.

Revenue costs, mainly content from the gaming business and incremental server bandwidth, were higher than expected, but that doesn't mean the market will "read" it negatively, as investors are now more comfortable with investments in AI services.

Overall operating profit came in at 51.48 billion, also slightly below market expectations of 52.06 billion.

Non-operating income supported a new high in profit, and associates nearly 10 billion in a single quarter, so overall net profit greatly exceeded expectations.

Associates' earnings in Q4 brought Tencent 9.2 billion yuan, nearly four times higher than last year's 2.4 billion yuan.

The current Tencent associates with faster profit growth, or higher profit amounts, and greater impact, are domestic companies such as Fast, Pinduoduo, Tongcheng, China Unicom, Shell, Vipshop, and Futura, and overseas companies such as supercell, Spotify, and Sea, which experienced profit growth in 2024, and therefore provided Tencent with a larger share of associates' profits as well.

Expectation of capex: Q4 AI-related capex reached 39 billion, and it is expected that it may exceed 100 billion in 2025.Depends on the explanation on the call

Valuation

Valuation base further improved.Final Q3 realized Non-IFRS net attributable profit of 55.3 billion yuan, up 30% year-on-year, but because affiliate profits accounted for a relatively large portion.If you look at adjusted EBITDA of 63.9 billion yuan, the year-on-year growth rate was 18%, but also higher than the revenue growth rate.

As the recent wave of Chinese stocks has pushed Tencent's share price to HK$540, with a closing price of HK$540 on March 19th.

If the adjusted EPS, the valuation TTM PE's slipped to 25.9 times from the 27.7 times of the

From the Forward PE (NTM), that is, 2025 EPS expectations, the valuation of 23.4 times, compared to the U.S. stock Mag7 is still not too high

In addition, in terms of shareholder returns, compared with the overall buyback + dividends of more than HK$144 billion in 2024, Tencent's buyback in 2025 is expected to be in the range of $80 billion (that is, about $400 million in a single trading day), while the dividend is increased by $41 billion, so the overall is also $121 billion, suggesting that Tencent itself feels that the stock price is probably unlikely to be deeper than a pullback as well.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Venus Reade·2025-03-20Tencent nearly doubled its profit last quarter and it’s barely moving… this will be in the red soon for no reason.LikeReport

- Merle Ted·2025-03-20Tencent should run the next couple of weeks after great earnings.LikeReport