BIG TECH WEEKLY | AI Data Crash Due To Oversupply? NVDA's Strong Support At 110

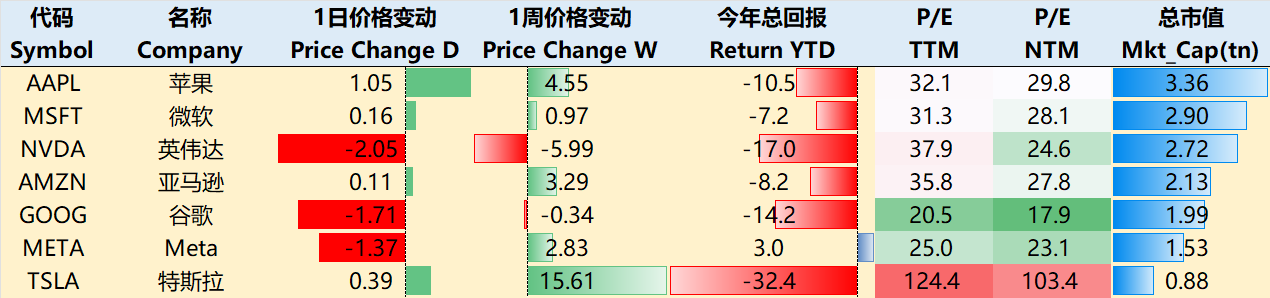

Big-Tech’s Performance

Weekly macro storyline: Divergence on US stock market

Q1 of the US stock market experienced rain, so "whether it is a medium-term intervention point" has become a hot topic of discussion.Policies favor the real economy over capital markets, while "soft data" continues to weaken.

The core differences and market focus on the direction of the market are:

foreign capital flows (Goldman Sachs believes that foreign capital, especially European funds, will continue to inflow, UBS warned that the funds may return to the local market),

sustainability of the rebound (Morgan based on the technical aspects of the short-term bullish, but medium-term by the impact of the policy, the Mo emphasized that the fundamentals of the rebound of the limitation of the space of the weak),

positioning of the economic cycle (Deutsche Bank through the historical data, suggesting that the current in the pullback rather than a bear market precursor, Mo believes that the risk of stagflation more similar to a structural crisis).(Deutsche Bank suggests through historical data that it is currently in a pullback rather than a precursor to a bear market, and Mo believes that the risk of stagflation is more akin to a structural crisis)

Markets are now fixated on two things: whether the government debt ceiling negotiations can loosen fiscal policy, and when the Fed can cut rates.Key variables for market volatility: trump policy, fiscal loosening (debt ceiling progress) and Fed rate cut path.

Additionally, dollar liquidity will be balanced back and forth between foreign exit pressures, and U.S. resident/corporate offtake capacity.

For their part, the big tech companies pulled back this week after a short-term rally, receiving a drop in arithmetic expectations, and are still trading at a high level of concentration.

Through the close of trading on March 27, most of the Big Tech companies rallied over the past week. $Apple(AAPL)$ +4.55%, $NVIDIA(NVDA)$ -5.99%, $Microsoft(MSFT)$ +0.97%, $Amazon.com(AMZN)$ +3.29%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ -0.34%, $Meta Platforms, Inc.(META)$ +2.83%, $Tesla Motors(TSLA)$ +15.61%。

Big-Tech’s Key Strategy

Does Microsoft's withdrawal of data center projects mean arithmetic demand has peaked?

Microsoft has abandoned projects for new (~2 gigawatts of power) data centers in the U.S. and Europe due to an oversupply of AI arithmetic.Let's start with a few conclusions

Microsoft's CapEx contraction this time is the result of short-term supply and demand mismatch, financial optimization and strategic adjustment, and does not change the trend of high investment in AI cloud computing in the long term (at least in the medium term);

Head vendors expansion rhythm is dislocated: Microsoft, Amazon's earliest input, and then adjusted, Meta, Google take over to make up for the rise, but the industry as a whole CapEx will still be climbing

Future competition focuses on efficiency: high-performance data centers, hardware upgrades (e.g., GPU/TPU iterations), and the ability to commercialize AI apps for cash (directly affecting ROIC)

Impact of Changing Relationship with OpenAI

Microsoft's relationship with OpenAI has seen changes over the past year: as OpenAI has gone from working exclusively with Microsoft to allowing the use of competitors' arithmetic, Microsoft is exploring alternatives to OpenAI models, considering Copilot to embed models from other companies.

OpenAI may even start building its own data centers in the mid- to long-term, in addition to acquiring capacity with three-party data centers.

It currently has $13 billion in backing.They have also modified their agreement to allow OpenAI to use other companies' cloud computing services.

TD Cowen's "bearish computing power" report is not the first time

The AI sector selloff on March 26th came almost exclusively from a TD Cowen report.Their take: Microsoft's abandonment of new data center projects in the U.S. and Europe that consumed a combined 2GW of power is a result of data center supply outstripping demand after current forecasts for its own needs.The part of the lease extension is because Microsoft is stockpiling for mid-term cloud and inference workloads.And for the portion that exceeds the mid-term capacity needs of the update, Microsoft simply canceled the lease.

Not for the first time, TD Cowen has issued back-to-back reports on Microsoft's declining data center demand since January.

January report: plummeting Microsoft data center demand tied to OpenAI business shift, withdrawal from multiple early negotiations (totaling over 1GW of capacity) and abandonment of contracted land; rare absence of hyperscale leasing team from industry conference (PTC); 33% of capacity originally planned to be procured for OpenAI workloads lagging behind schedule; OpenAI turning to Oracle to partner on the "Stargate" project due to lack of speed of construction by Microsoft"Stargate" project.

February report: termination of some leases for "construction delays" or "power issues" and slowing down the process of converting signed Statements of Qualification (SOQs) into full leases (previously SOQ conversions had a success rate of nearly 100%); Earl's international expenditures tilted toward theU.S. (with some geopolitical implications)

Will the US AI major's business model change?

Microsoft is making a big push for what it calls "Copilot Devices," signaling a shift in strategy: away from new construction and toward outfitting existing data centers with servers and other equipment.

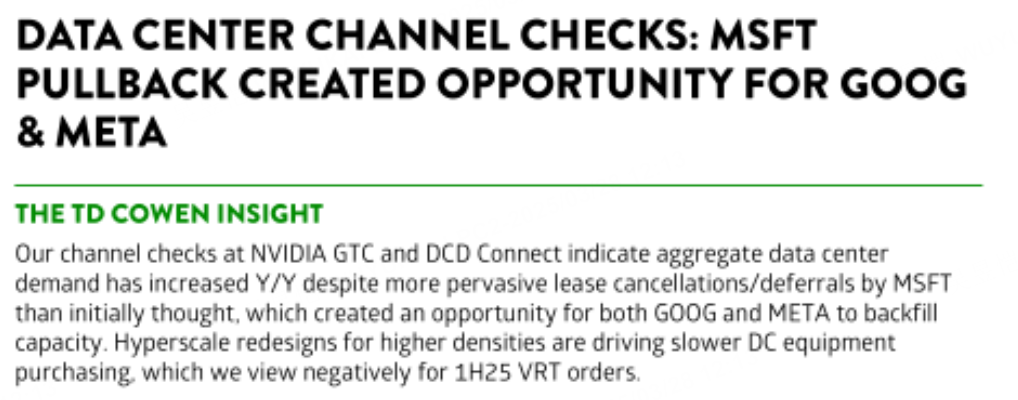

A big reason for the slowdown in orders for data center equipment in January was a redesign by hyperscale data center operators, as some data centers need to support higher rack densities (to accommodate higher-computing GPUs), among other things.At the same time, some of Microsoft's demand exited, allowing Google and Meta to step in to fill it (Google more to fill the international market, Meta more US domestic)

But that doesn't change the business logic of the big AI vendors.

U.S. vendors typically create value through differentiation, investing significant resources in developing proprietary models and innovative algorithms to provide unique services or products.Characterized by high cost and differentiation, the focus is on creating high-end, specialized solutions that can garner higher pricing power in the market.

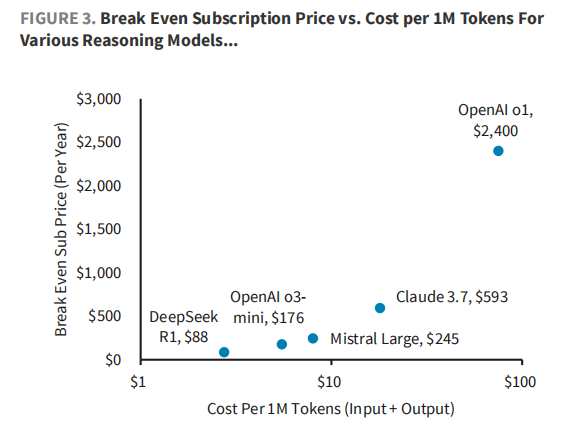

Chinese tech giants like DeepSeek are more inclined to adopt cost-cutting strategies, including API market price wars, where vendors grab market share by drastically reducing prices.Chinese companies prefer to utilize open source models, which not only reduces R&D costs but also operational expenses.

Isn't this similar to a certain industry as well?

Big Tech Options Strategy

This week we focus on: NVDA has its own problems, but plunge orders keep coming?

GB200 has supply chain and technology bottlenecks in the short term or weaken NVIDIA market competitiveness.Mainly include:

High deployment complexity: GB200 takes 5-7 days to deploy in a single run, with frequent system instability and crashes during operation, which affects customer efficiency.

Copper cable engineering bottleneck: The NVL72 system requires the laying of more than 5,000 customized copper cables, which significantly pushes up the deployment cost due to the difficulty in adapting specifications and installation.

Strong technical dependency: The equipment rack configuration is highly dependent on NVIDIA engineers, so the customer's autonomy is insufficient, restricting the flexibility of operation and maintenance.

Cloud service providers (CSPs) turn to mature products such as HGX due to the complexity of GB200, intensifying the pressure on market acceptance of the GB series.In addition, GB300 is likely to be laid out ahead of schedule, with the release of GB300 samples in 2025Q2 (mass production delayed to 2026), or accelerating GB200 demand diversion. incremental sales of B200 AI GPUs may partially hedge the risk.

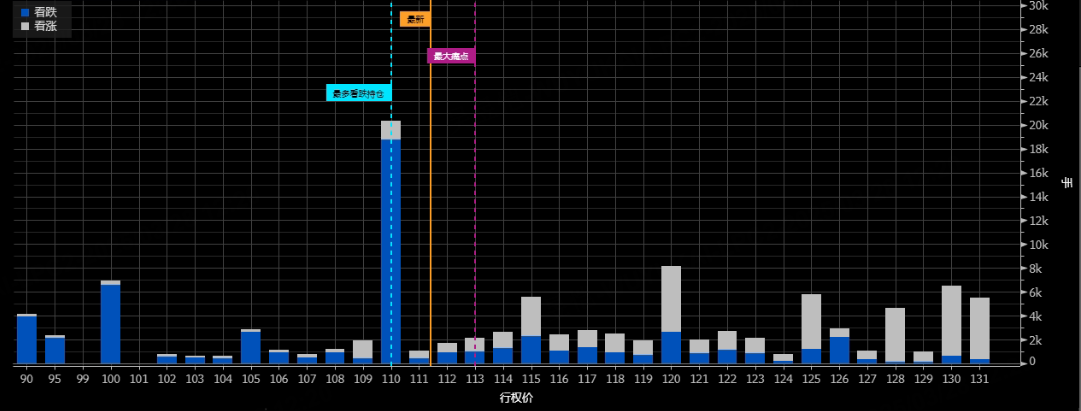

NVDA followed the arithmetic sector this week with a big drop, but from the current to April 21, four weeks of open options, the most for the closed PUT in the position of 110, close to the maximum pain , indicating that this position is willing to take over the bottom of the investor is not a lot.

Big Tech Portfolio

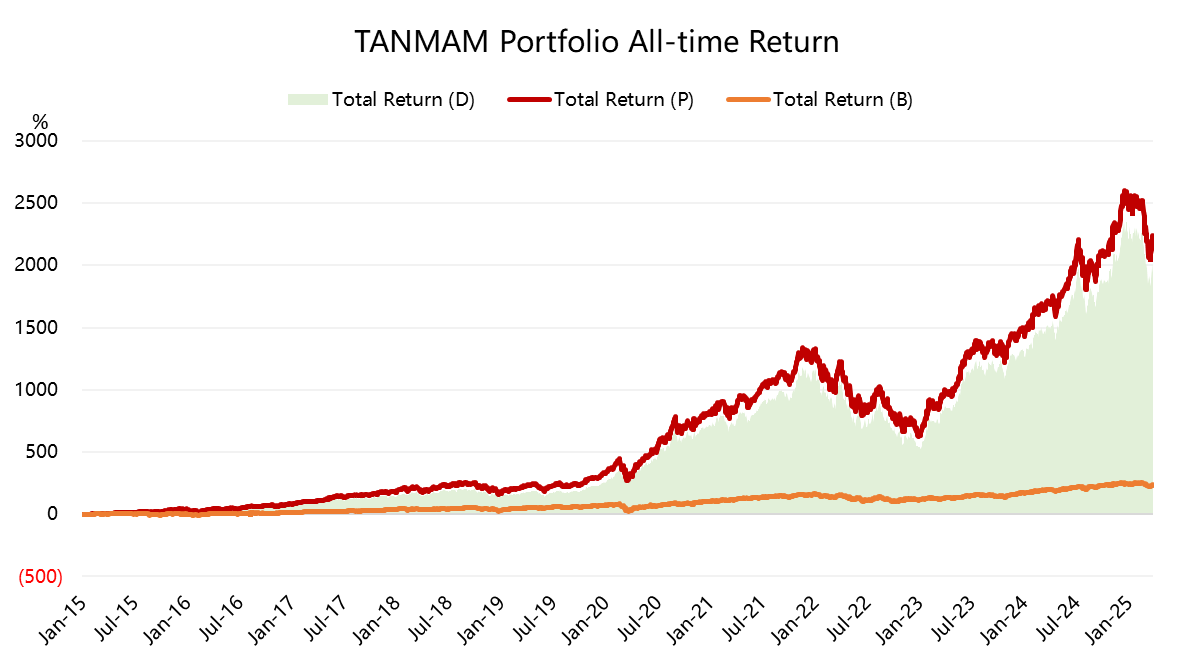

The Magnificent Seven form a portfolio (the "TANMAMG" portfolio) that is equally weighted and reweighted quarterly.The backtesting results are far outperforming the $S&P 500(.SPX)$ since 2015, with a total return of 2,157.49%, while the $SPDR S&P 500 ETF Trust(SPY)$ returned 229.67% over the same period, an excess return of 1,927.82%.

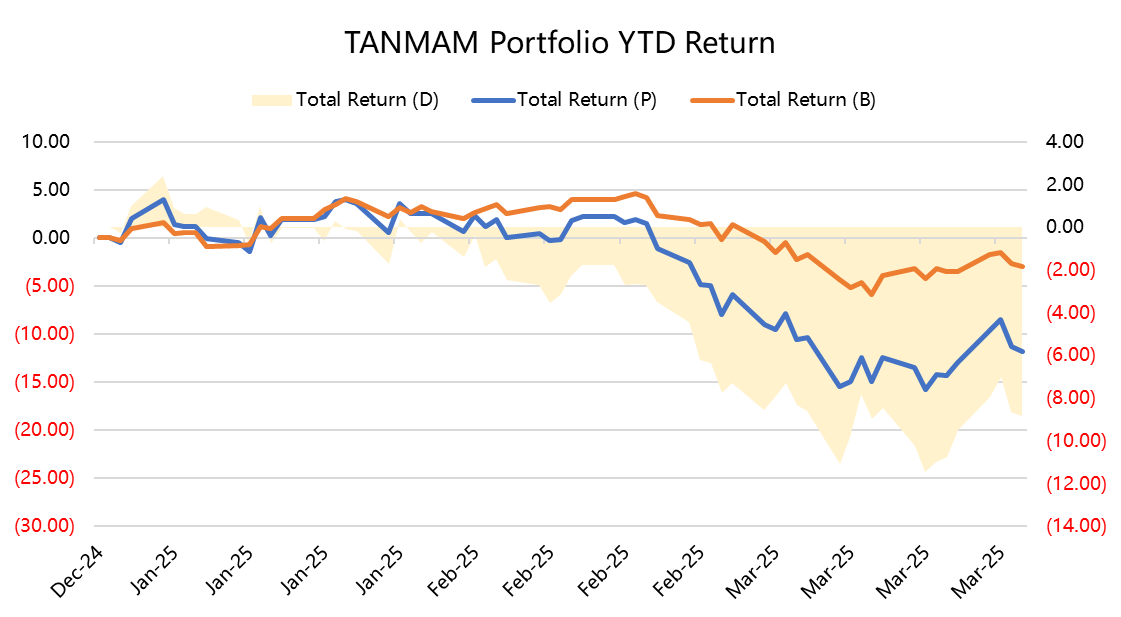

Big tech stocks have pulled back so far this year, returning -11.81%, less than the SPY's -2.95%;

The portfolio's Sharpe Ratio over the past year has retreated to 0.92, the SPY is 0.43 and the portfolio's Information Ratio is 1.04.

$Invesco QQQ(QQQ)$ $NASDAQ(.IXIC)$ $ProShares UltraPro QQQ(TQQQ)$ $ProShares UltraPro Short QQQ(SQQQ)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Valerie Archibald·2025-03-28So is MSFT buying TikTok?1Report

- fuddie·2025-03-28Wow, incredible insights here! [Wow]LikeReport

- jazza·2025-03-29Great article, would you like to share it?LikeReport