TECH Reviews on Earning Season: Earnings Must Deliver REAL Cash, Not Hype

Last week was characterized by a "mixed bag": calm on the surface ( $S&P 500(.SPX)$ down 31bps, $Cboe Volatility Index(VIX)$ touched a 6-month low)Hidden sharp divergences,quality/momentum factors significantly underperform, and market breadth continues to narrow under AI theme dominance.

On the eve of the earnings season, the environment is "okay but not optimistic" - valuation pressures and the lower performance thresholds have formed a tug-of-war, the performance of the TMT sector in the second half of the year will be more dependent on earnings performance (E) rather than valuation expansion (P), especially the need to verify the "cost" of AI investment (P).TMT sector performance in the second half of the year will be more dependent on earnings performance (E) than valuation expansion (P), in particular, the need to verify the "cost-benefit" balance of AI investment (Fortune 500 could unlock $780 billion in NPV if they achieve 14% cost reduction).

The key conflict centers on:

Whether the software sector can take advantage of the September user conference season to turn the tide;

Whether strong stocks (e.g., $Netflix(NFLX)$ $CrowdStrike Holdings, Inc.(CRWD)$ ) can cash in on valuations;

Whether cloud services ( $Amazon.com(AMZN)$ AWS/ $Alphabet(GOOG)$ GCP) can continue Azure/OCI growth;

Big Tech 2026 capex guidance ( $Microsoft(MSFT)$ stance is critical).

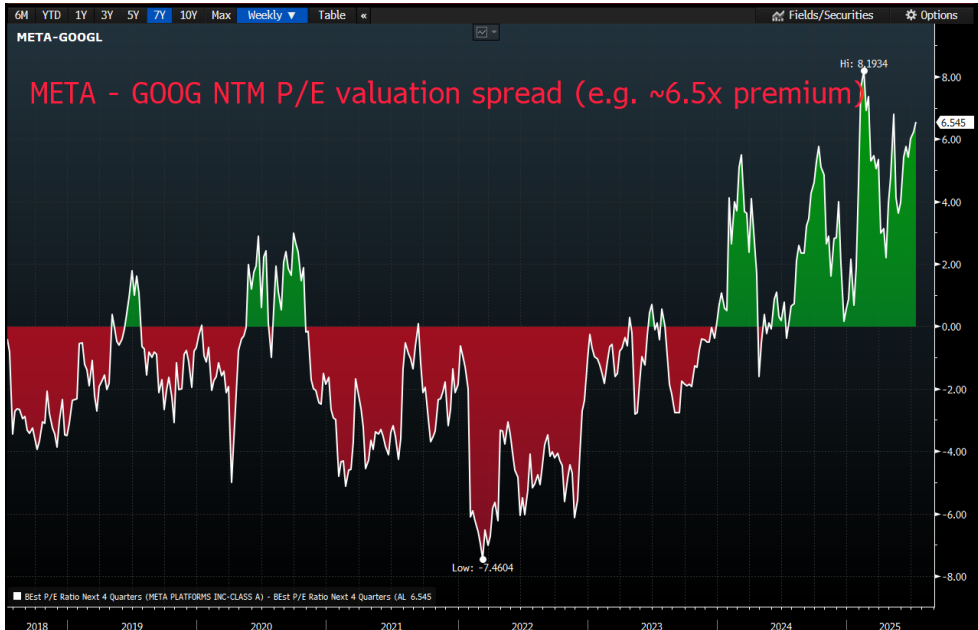

Next week's highlights include ASML/TSM/NFLX earnings, CPI data and the AI Summit, while META's 6.5x PE premium to $Alphabet(GOOGL)$ underscores the market's differentiated pricing for AI real estate.Overall, investors are at a crossroads between "sticking with AI winners" and "tapping valuation depressions," with the IT sector's 33.5% S&P weighting (the highest since the dot-com bubble) highlighting the risky decision.

Overview of Market Dynamics: Bland on the Surface, But Turbulent on the Inside

Overall performance: The market was flat on the surface last week, with the S&P 500 down 31 basis points and the VIX volatility index touching a ~6-month low, indicating relatively stable sentiment.However, the internal structure fluctuated dramatically, with the Quality Factor, Crowdedness Factor, Momentum Factor and Growth Factor all significantly underperforming the broader market, indicating divergent investor behavior.

Drivers: no obvious single trigger, more of a multi-factor pullback:

Mean reversion: AI-related stocks and quarter-end winners pulling back after a run-up.

Macro-expectations digested: tariff policy "clarity" could be pro-cyclical (e.g., Delta comments that it could boost business confidence).

Financial environment eases: GS Retail Favs basket breaks out of consolidation, reflecting improved liquidity.

Market challenge: Investors face a dilemma as market breadth continues to narrow and AI themes (including "Netflix" stocks such as meme stocks) dominate the two-way market:

Choose to stick with existing strategies (despite stretched, expensive valuations and momentum reversals).

Or move into controversial areas (e.g., small- and mid-cap internet, software, services, and value stocks) for fear of further valuation "rubber band" stretching.

Current environment: The environment is "just ok" heading into earnings season.Prices and positions pose mild headwinds, but lower earnings thresholds (e.g., conservative guidance from companies in a period of uncertainty) could lead to superficially strong earnings reports.

Earnings season outlook: the TMT sector relies on earnings rather than valuations

Timing: most of the earnings season in the TMT sector will begin in two weeks (mid-July 2025 at the time of document release).

Core Focus: Upside momentum in TMT stocks in the second half of the year will be more dependent on earnings ("E") than valuation ("P"), especially as 2026 expectations come into view.Reasons include:

Beat-and-reit was sufficient last quarter (due to the complex environment), but this quarter is likely to be more demanding and investors need to focus on earnings sustainability.

Thematic background: the game of AI "costs" vs. "benefits" (revenue growth vs. operating leverage).Investors are looking for more empirical evidence of the benefits of AI (e.g., improved operational efficiency as a result of AI adoption by enterprises) to support confidence in the sustainability of AI spending in 2026 and beyond.

Potential Risks: Sectors such as software may struggle to rebound if AI fever does not cool; meanwhile, high-flying stocks (e.g., RBLX, NFLX, CRWD, $Palantir Technologies Inc.(PLTR)$ ) need to meet high valuation expectations.

Key Outstanding Issues: 10 Focus Points for Earnings Season

The report lists 10 core issues that reflect investors' current concerns:

Next week's earnings preview: watch $ASML Holding NV(ASML)$ (focus on 2026 order trends vs €3.9bn last quarter), TSMC $Taiwan Semiconductor Manufacturing(TSM)$ focus on exchange rates/gross margins vs AI long term strategy), and Nifty (NFLX, how big an earnings beat needs to be).

Software sector recovery: can earnings and September user conference season help software stocks get back on track?Maybe AI fever needs to cool down first.

Rising performance bar: Last quarter's "met" was sufficient, but this quarter will be more demanding (e.g., $ServiceNow(NOW)$ $Atlassian Corporation PLC(TEAM)$ TSM and other early reporting companies).

The Goofy Stock Challenge: Can high valuation stocks (e.g., $Roblox Corporation(RBLX)$ NFLX) meet expectations?Or cyclical optimism triggers capital rotation.

Analog Semiconductor Stock Dynamics: Can Earnings Beat Drive Rally?Or market worries about seasonal demand front-loading risks.

2026 outlook: is it too early to focus on big tech capex/opex? microsoft's (msft) fy26 comments may offer clues (bloomberg consensus forecasts billions of dollars of year-over-year capex growth in 2026 for googl and amzn).

How about an index push on the main battleground tickets: $IBM(IBM)$ $Arista Networks(ANET)$ $Advanced Micro Devices(AMD)$ $Booking Holdings(BKNG)$ $Uber(UBER)$ $Fortinet(FTNT)$ $ServiceNow(NOW)$ $Oracle(ORCL)$ , etc.performance; whether Mag 7 views change: MSFT/META/ $NVIDIA(NVDA)$ > AMZN > GOOGL/AAPL.

Tariff impact: uncertainty removed (e.g., Delta says it could boost confidence), but potential margin impact needs to be monitored.

AI operational leverage: operational efficiency optimism from AI (e.g., AMZN and $Palo Alto Networks(PANW)$ comments), but macro/micro mechanisms need to be validated (speed of enterprise adoption on market efficiency).

Cloud services growth: after MSFT Azure and ORCL OCI accelerate in 2025H1, can GOOG GCP and AMZN AWS follow in H2 (data center capacity coming online, zero-sum game or rising water)?

Important events preview: key schedule for next week

Policy & Summits: House Financial Services Committee "Crypto Week" + Pittsburgh AI & Energy Summit (Trump with Altman, Zuckerberg, etc.).

MACRO DATA: U.S. CPI (7/15, expect core +2.9% y/y), PPI (7/16), retail sales + Philly Fed data (7/17), new home starts + University of Michigan confidence index (7/18).

Earnings Releases:

7/14: HCL Tech, FAST (pre-market).

7/15: Citi, Ericsson, JPMorgan, Wells Fargo (pre-market); JB Hunt, OMC (after-hours).

7/16: ASML, Bank of America, Johnson & Johnson, Morgan Stanley, PNC (pre-market); United Airlines (after-hours).

7/17: CTAS, LTIMindtree, MAN, Publicis, TSMC, Volvo, Wipro (pre-market); PCCW Securities, Nifty (after-hours).

7/18: 3M, American Express, Autoliv (pre-market).

Other: Sea (SE) Free Fire 8th Anniversary Campaign Kicks Off (7/18); Japan's Senate Elections (7/20).

Insights and Chart Analysis: Expert Insight and Data Support

The report contains in-depth analysis and multiple charts, with images embedded below in the order of their original descriptions (make sure they are immediately adjacent to the relevant text).

SOFTWARE SECTOR WEAKNESS: The Goldman Sachs broad-based software basket (gstmtsft) underperformed the S&P 500 by about 485 basis points over two days (Thursday and Friday), its worst performance since November 2022.The reason for this is unknown and may involve a string of semi-factors (e.g., narrow market breadth due to AI dominance).

NVDA Strong But Weak To Start Year: NVIDIA (NVDA) has outperformed the broader market for seven straight days, with its market capitalization topping $4 trillion (an increase of about $1 trillion over the past two months), but it's up only about 20% for the year, marking one of the worst yearly starts in nearly a decade.(Note: Charts share the same labels as the software section, different src is not specified in the document, so the same embedding is used.)

Big Tech Sentiment Comparison: GOOGL and META diverge (GOOGL outperforms META by ~500 bps for the month) META is up 25% for the year and the market is comfortable with its AI hiring; GOOGL has mixed sentiment and is expected to "pull back" META's NTM P/E is ~6.5x premium to GOOGL.META's NTM P/E is ~6.5x premium to GOOGL.(Ditto for reuse of image tags in documents.)

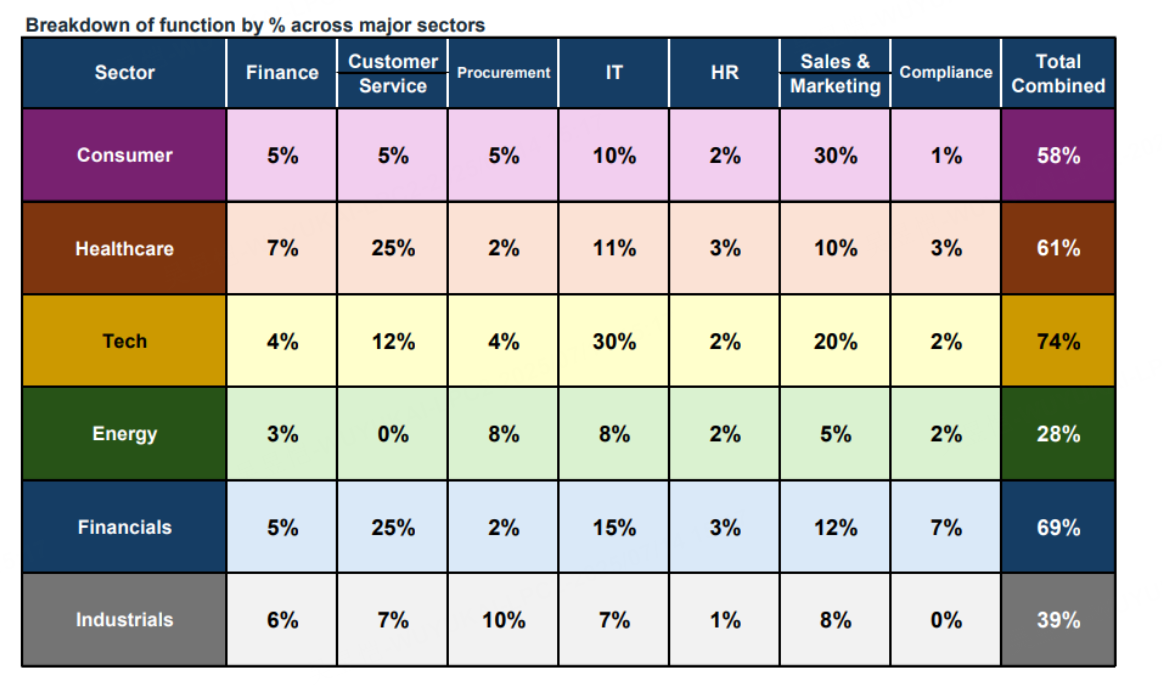

AI return on investment (ROI) analysis: the Goldman Sachs Semiconductor Initiation Study shows that AI could potentially deliver significant cost savings for the Fortune 500.Measured cost reduction scenarios based on different functional departments (e.g., finance, customer service, procurement):

Conservative cuts: 7% total cost reduction (e.g., procurement -20%).

Basic cuts: 14% total cost reduction (target scenario), unlocking ~$780 billion in NPV savings over 2025-2030, corresponding to $350 billion in AI capex realizing triple-digit returns.

Aggressive cuts: 19% total cost reduction.

All-time high IT weighting: IT GICS has a 33.5% weighting in the S&P 500, the highest since the internet bubble (after the 2018 communications services migration).(This section of the document uses a different CAPTION, so it is embedded separately.)

Overall Insights and Conclusions

Core Theme: AI remains a dominant market force, but earnings season will test its sustainability.Investors need to balance AI costs and benefits and focus on earnings realism rather than valuation bubbles.

Risks: Narrow market breadth, high factor volatility, tariffs and macro data (e.g. CPI) could trigger short-term shocks.Software and semiconductor sectors are key bellwethers.

Recommendations for action: Monitor next week's events (e.g., Nifty earnings and the AI Summit) and utilize the GIR portal for additional roadshow summaries (e.g., meetings with Capgemini, Horizon, etc.).

Final Thoughts: The report emphasizes that there are both opportunities and risks in the "okay" environment, and that TMT performance in the second half of the year will depend on the ability of companies to prove the return on their AI investments through earnings, rather than relying solely on market enthusiasm.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Merle Ted·2025-07-15NVDA is going to $200 very soonLikeReport

- Valerie Archibald·2025-07-15Googoo is way way undervalued. They will win the AI race guaranteedLikeReport

- EVBullMusketeer·2025-07-14Do you think META's premium over GOOGL can holdLikeReport

- bubblyo·2025-07-14Amazing insights on the earnings season! [Wow]LikeReport

- JoanneSamson·2025-07-14Smart decisionLikeReport